Welcome! Today, we delve into a critical examination of the cognitive bias known as the halo effect, particularly concerning discussions about China’s economy. The halo effect refers to the tendency to evaluate individuals or groups as entirely favorable or unfavorable. Enthusiasts of China often encounter criticism from detractors who cling to outdated or distorted views, leading them to overlook genuine issues, such as the unwinding of China’s enormous real estate bubble.

For example, we faced considerable criticism for pointing out China’s overinvestment and overcapacity challenges, which pose risks not just to China but to the global economy. Many argued that this situation was impossible or benign. However, the Chinese government has since acknowledged the substantial overcapacity in several major manufacturing sectors, which they termed “involution,” during a period of deflation—a particularly troubling scenario for a nation burdened with high private debt. The government is now attempting to rationalize these sectors, a process fraught with difficulties.

While the United States finds itself in a considerably weaker position than China, this does not negate the significant challenges and headwinds facing the Chinese economy.

By Kenneth Rogoff, Thomas D. Cabot Professor of Public Policy and Professor of Economics, Harvard University; and Yuanchen Yang, Economist, International Monetary Fund. Originally published at VoxEU.

A significant debate is unfolding over whether China may be on the brink of experiencing a situation akin to Japan’s stagnation following its real estate bubble in the 1990s. This discussion evaluates China’s current adjustments in real estate against Japan’s experiences and reveals notable similarities in investment patterns and responses in consumption. A critical takeaway from both situations is that unwinding overinvestment during a housing boom is not a quick process. Excess supply can linger in the economy, discouraging new investment and depressing activity long after volumes and prices have peaked. While China still possesses the ability to influence the outcomes of its adjustment, the available time is diminishing as overcapacity, sluggish consumption, and negative sentiment mutually reinforce one another.

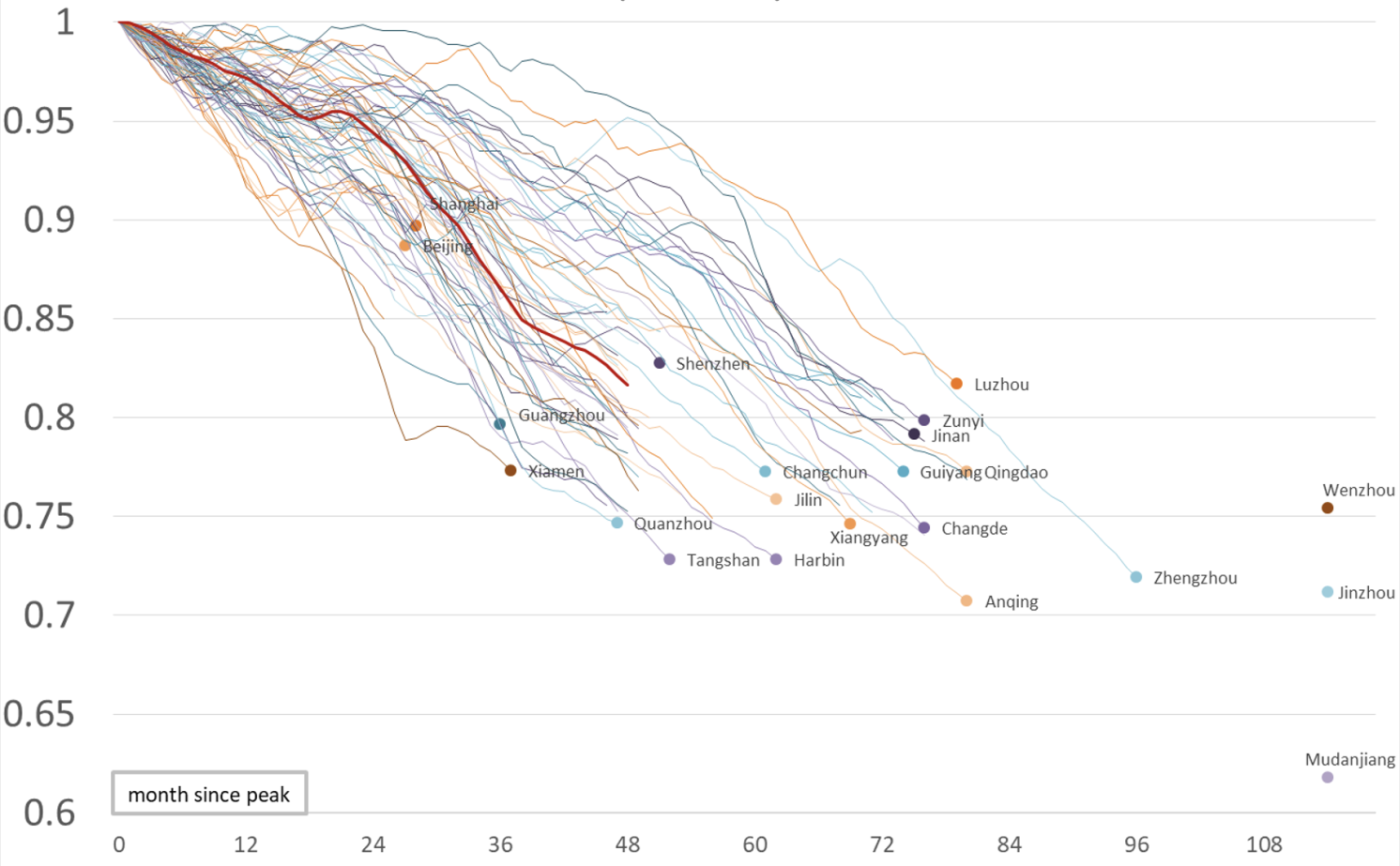

China’s extended real estate decline has emerged as a primary concern in global macroeconomic discussions. With residential investment continuing to slide, house prices steadily decreasing across much of the nation (Figure 1), and consumer confidence remaining low, the discourse around whether China is at risk of mirroring Japan’s post-bubble stagnation of the 1990s is intensifying.

Figure 1 House price decline by city in China

Cumulative monthly decline from peak (peak = 1)

Sources: National Bureau of Statistics of China and authors’ calculations

Notes: The price index is constructed using the National Bureau of Statistics’ monthly residential property resale price index for 70 large and medium-sized Chinese cities. For each city, the index is normalized to its historical peak (the series begins in 2011, with peaks occurring between 2017 and 2023 depending on the city). All other monthly observations are then expressed relative to this benchmark.

This unexpected turn of events has taken many observers by surprise. Although some had cautioned against the sustainability of China’s unprecedented real estate appreciation—predicting major adjustment challenges (see Rogoff 2015 on the inevitable and severe impact of the debt super-cycle)—the prevalent belief had long been that any adjustment in the real estate market was still far on the horizon (e.g., Glaeser et al. 2017) and that, if it occurred, it would be less severe than the crashes seen in Western nations. Chinese homeowners tend to be less leveraged than their American counterparts, and it was thought that China’s strong central government would manage to mitigate any defaults much more efficiently than the prolonged processes seen in Western legal systems, thus reducing the debilitating uncertainty that often accompanies debt crises.

However, as the crisis in China extends into its sixth year, the prevailing view that real estate crises will be mild and fleeting unless exacerbated by a banking crisis (Bernanke 1983, Schularick et al. 2014) appears to be overly optimistic, with various other amplification mechanisms also playing a role. Rognlie et al. (2018) emphasized that excess housing construction can create significant and lingering demand shortfalls, even in the absence of a traditional financial crisis, while Rogoff and Yang (2020) highlighted that China’s overbuilding had reached astounding levels nationwide.

In our newest research (Rogoff and Yang 2026), we explore this issue by comparing China’s current real estate adjustments with the experiences Japan faced in the 1990s. Our analysis considers relative growth across nearly 300 cities in China versus 47 prefectures in Japan. Interestingly, regions that experienced substantial overbuilding tended to endure severe downturns. Though the comparison is not perfect—China today is poorer, less financial liberalized, and operates under a distinct political framework—we still uncover compelling similarities in the investment dynamics and consumption responses between the two nations.

Real Estate as a Growth Engine – and Its Limits

For many years, real estate has been vital to China’s remarkable economic growth. Activity tied to real estate, including upstream and downstream connections and related infrastructure, constituted nearly one-third of total demand at its peak (Rogoff and Yang 2021). This massive investment spurred rapid urbanization and bolstered local government revenues through land sales.

However, the sheer scale of this expansion has become problematic. By the late 2010s, the per capita housing stock in China had reached levels comparable to much wealthier economies. In numerous smaller ‘tier 3’ cities, which are often witnessing population decline, construction persisted even as genuine demand softened. The returns on new investments have continually diminished (Rogoff and Yang 2024a, 2024b).

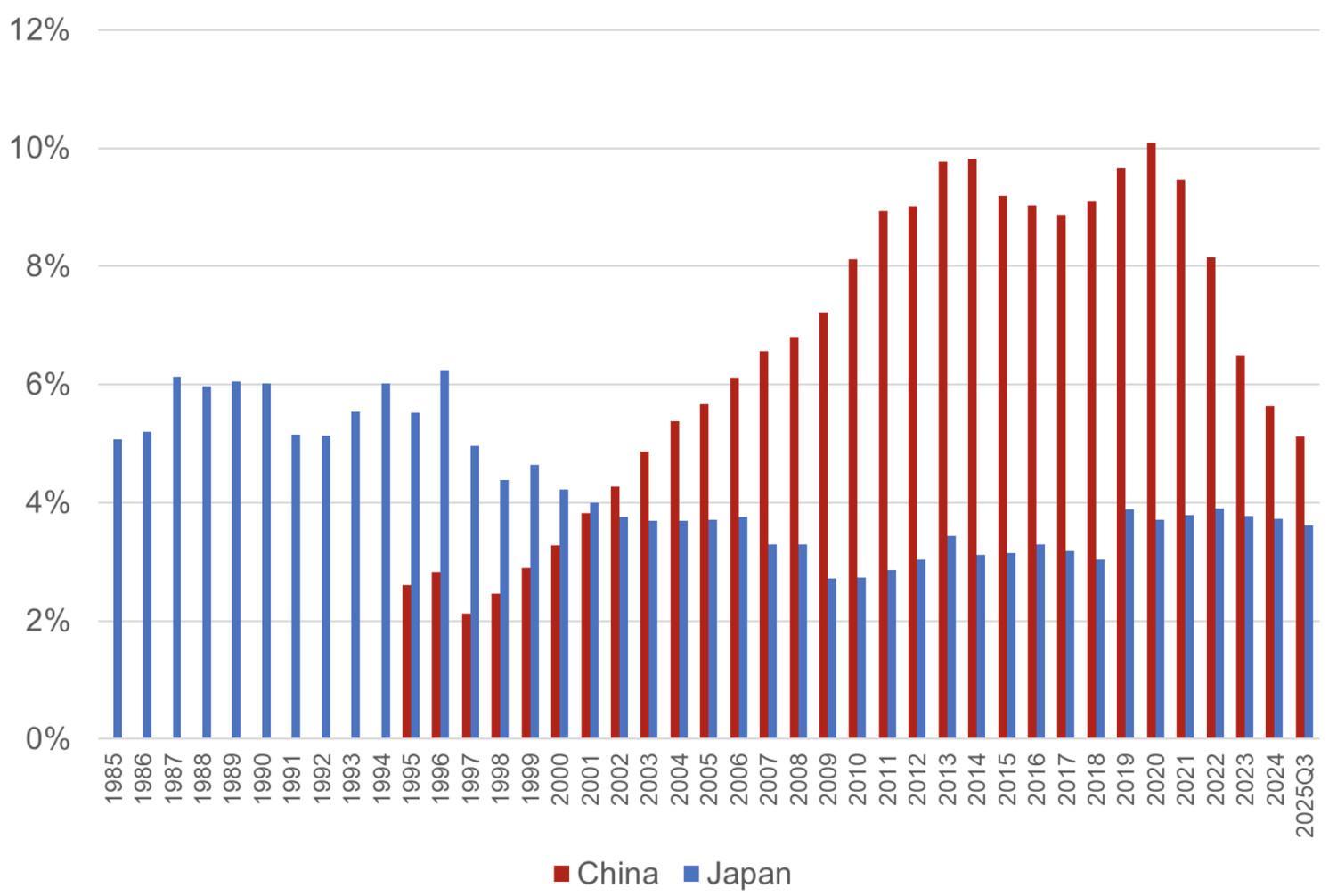

A strikingly similar dynamic occurred in Japan during the 1980s. Real estate and commercial construction boomed alongside infrastructure spending, driving land and housing prices to extraordinary heights. When the bubble burst in the early 1990s, real estate investment remained low for an extended period and never recovered to pre-crisis levels (Figure 2).

Figure 2 Real estate investment as a percentage of GDP

Sources: National Bureau of Statistics of China, Cabinet Office of Japan, and authors’ calculations.

The crucial takeaway from both scenarios is fundamentally structural. Housing possesses a high degree of durability, and unwinding overinvestment during a boom is a slow process. Excess supply looms over the economy, discouraging new investment and weighing heavily on activity long after volumes and prices have peaked.

Declining Returns and the Investment Overhang

By analyzing city-level data for China and prefecture-level data for Japan, we observe a common trend: regions that aggressively built during the boom faced deeper and longer-lasting slowdowns afterward. In both nations, the contribution of real estate investment to growth has deteriorated over time, eventually turning negative.

Importantly, this decline began prior to the headline crises. In China, the returns on real estate investment were already on the downward trend well before the significant 2021 Evergrande default and the tightening measures linked to the ‘three red lines’ aimed at reducing leverage in the sector. This significant downturn reveals that the roots of the issue lay not merely in regulatory missteps but rather in long-standing structural imbalances.

Japan’s experience offers insight into duration. The negative impact of real estate investment on growth persisted for over a decade following the bubble burst. Although GDP stabilized, the real estate sector continued to hinder recovery throughout the late 1990s and early 2000s.

This suggests that simply stabilizing prices or restoring credit opportunities may not quickly revive growth. When the challenge lies in excessive capital rather than a deficit, stimulus measures risk producing diminishing returns.

Wealth Effects: The Underappreciated Channel

Cumulative investment, often surpassing demand, gradually creates excess supply and exerts downward pressure on prices, particularly in cities characterized by significant investment overhang. In both countries, plummeting house prices exert powerful wealth effects. In Japan, decreasing land prices severely impacted household balance sheets, leading to a notable decline in consumption, even in regions where credit remained intact.

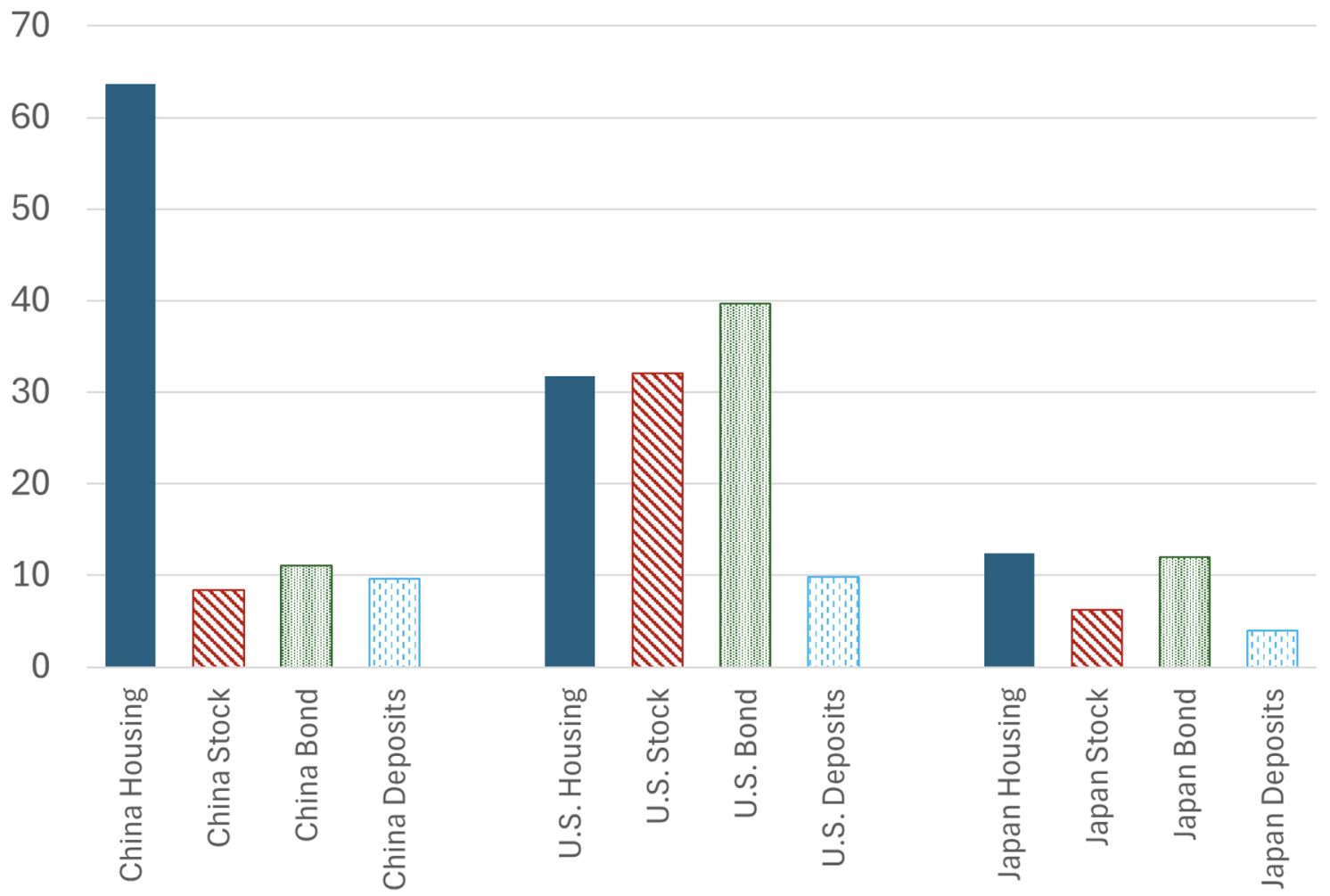

China, interestingly, faces an even more pronounced version of this phenomenon. Approximately 70% of Chinese household wealth is tied to housing, markedly higher than in advanced economies, where consumption accounts for just around 40% of GDP (Figure 3). Consequently, when house prices decline, households tend to reduce spending—feeling poorer and treating housing as a form of precautionary saving in a system lacking comprehensive social insurance.

Figure 3 Valuation of different asset classes, 2017 (trillions of dollars)

Sources: World Bank, BIS, National Bureau of Statistics of China, Bank of Japan, FRED, Zillow, and authors’ calculations

Our estimates suggest that a sizable national correction in house prices could diminish overall consumption by 2-4 percentage points of GDP, substantially exceeding the effects that announced consumption-support policy measures are intended to counteract.

Sentiment: Amplification Beyond Wealth Effects

In addition to wealth effects, we found that sentiment plays a crucial role in amplifying the situation. When households anticipate continued declines in prices, they tend to postpone purchases and increase precautionary savings, intensifying the slowdown. This effect, highlighted in previous work on expectations and ‘animal spirits’ (e.g., Soo 2018), was also observable in Japan, where pessimism about land prices persisted long after the initial crash.

In the case of China, sentiment appears particularly influential. Utilizing news-based metrics to gauge the tone of the housing market, we discover that negative sentiment significantly magnifies the impact of price declines on consumption. Once households internalize the belief that housing is no longer a dependable store of value, a self-reinforcing feedback loop develops.

Why China Is Similar, and Why It Is Different

Despite these similarities, China is distinctly different from Japan. The structure of leverage varies: Japan’s crisis revolved around private banks and corporations, while China’s vulnerabilities are concentrated in local governments and state-affiliated entities. Furthermore, China’s administrative capacity allows for greater deferral of loss recognition, reducing the likelihood of a complete financial sector collapse.

China also possesses advantages that Japan did not have. Productivity growth remains robust, and the country is positioned close to the global frontier in emerging sectors like electric vehicles and renewable energy, which could soften the impact of potential stagnation.

However, these differences carry potential downsides as well. China is aging more rapidly than Japan was in the 1990s, and as a developing nation, it lacks Japan’s extensive social safety net. Moreover, newer growth engines, irrespective of their dynamic nature, are still relatively small compared to the contributions made by real estate and infrastructure. Transitioning swiftly from one export-driven boom to another is unlikely to fully compensate for a declining consumer demand in an economy of China’s magnitude.

Looking Beyond Short-Term Stabilisation

The central takeaway from both Japan’s experience and the current circumstances in China is that dodging a banking crisis is insufficient. When a growth model reliant on investment—whether in real estate, infrastructure, or emerging sectors—encounters diminishing returns, the adjustment process can be prolonged and complex, even in the absence of an outright banking crisis, unless demand can be effectively redirected towards consumption.

Several key dynamics arise from this analysis. Accelerating the reduction of excess housing supply, even at the expense of acknowledging losses, might expedite the adjustment. Prolonged forbearance risks ‘zombifying’ local governments and developers, much like how ‘zombie banks’ constrained Japan (IMF 2026). Restoring household confidence will require more than just stabilizing prices; robust social insurance, clearer income opportunities, and a credible policy commitment to rebalancing could help lessen precautionary savings and revitalize consumer spending (Katz 2026).

Japan’s lost decade(s) serves as a cautionary narrative. While China still has room to influence the outcome of its adjustment, the narrowing window of opportunity, marked by overcapacity, weak consumption, and negative sentiment interplaying, underscores the importance of prudent management. Although the real estate sector may no longer be the main driver of growth, how China chooses to navigate its retreat from this previously dominant sector will significantly influence its macroeconomic direction for the years ahead.

See original post for references.