The stock market’s ascent often creates a false sense of security, obscuring the underlying economic challenges. Why worry about stagnant wages when the allure of profits from stocks can outweigh the grind of a traditional paycheck? Many would rather accumulate wealth through the stock market than through labor.

Indeed, the joy of receiving an inflated quarterly brokerage statement can eclipse the disappointment of a mediocre biweekly paycheck. As stock prices climb, so does the perception of intelligence, bolstered by optimistic growth lines on quarterly statements.

Why complain about a labor participation rate at its lowest in 40 years when Netflix shares have soared over 6,000 percent? The ocean of inexpensive, on-demand entertainment more than compensates for a lack of decent-paying jobs. Today’s society has never offered more comfort for inactive lifestyles, especially with large-screen TVs available on credit.

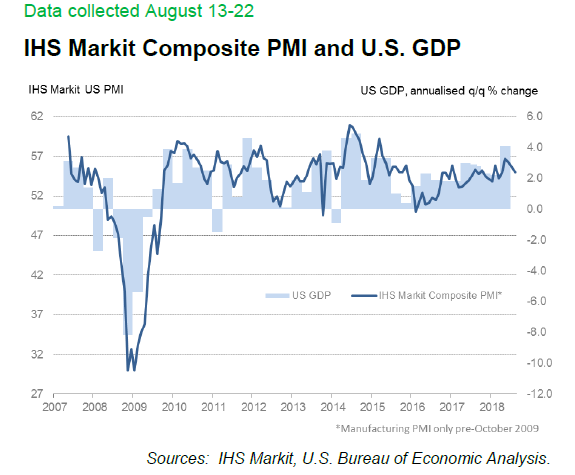

Recently, a largely trivial milestone was celebrated: U.S. stocks, as represented by the S&P 500, notched the longest bull market in history without a 20 percent downturn—3,453 days, despite several near misses along the way.

The greatest beneficiaries of this prolonged bull market were those who disregarded potential pitfalls and continued to invest in S&P 500 Index Funds or stocks from giants like Facebook and Amazon. Strategies like buy and hold, dollar-cost averaging, and buying the dip have proven profitable during this bullish run.

So, what should we conclude from this?

One of life’s profound pursuits is finding meaning in the seemingly meaningless. Let’s take this historic yet superficial milestone of the stock market as a point for contemplation. Where to begin?

“The bigger they come, the harder they fall,” Jimmy Cliff remarked during the bear market of the early 1970s. Using this wisdom, let’s seek insight into one of the fundamental aspects of this bull market.

Promise of the Data

The unwavering faith in statistical data has directed trading choices throughout this bull market. The underlying belief is that by analyzing comprehensive data over time, decisions for future trading can be predetermined. According to these models, tomorrow’s trading forecasts are artifacts of the past.

Modern economists, armed with far more data but considerably less intuition than 19th-century farmers consulting the Old Farmer’s Almanac, operate with a misplaced confidence. They assume to possess the answers to impending questions while remaining rooted in the present and fixated on past data. Vast data sets are extrapolated, promising predictive insights like gospel truths.

So-called statistical prophets utilize cutting-edge technology and automated trading systems, firmly believing these will lead them to wealth. They assert that with sufficient analysis, no market dip is too small to profit from through high-frequency trading. But what could possibly go awry?

Excessive intelligence can lead to reckless decisions. Just ask Nobel laureates Myron Scholes and Robert Merton. In 1998, they, alongside their investors, experienced a costly lesson regarding the limitations of statistical modeling.

Within just four months, their hedge fund, Long Term Capital Management, lost $4.6 billion. The crisis escalated to the point where Federal Reserve intervention became necessary to prevent widespread panic.

Their sophisticated models missed predicting the Asian financial crisis of 1997 and the Russian financial crisis of 1998. Suddenly, the highly leveraged arbitrage trades they depended on diverged in ways deemed statistically impossible—altering the reputations of Scholes and Merton irrevocably.

As the Credit Cycle Turns

Over the past nine years—and even the last 35—the stock market has shown remarkable continuous growth. In contrast, the debt market has witnessed a consistent decline in interest rates.

We suspect that the coming 35 years will starkly contrast the previous ones. Historical market data may no longer serve as a reliable predictor for future trends, potentially complicating quantitative analyses.

Currently, the risks of a financial crisis are escalating. After a decade of low-interest-rate policies flooded emerging market borrowers with cheap credit, the credit cycle has shifted. The Federal Reserve is, albeit gradually, reducing its balance sheet and increasing the federal funds rate.

As the dollar strengthens, emerging market borrowers are increasingly struggling to manage debts in depreciating national currencies. Recently, Turkey has felt this pressure, but soon other nations like South Africa, Brazil, Russia, or Mexico may follow suit.

The effects of a potential debt and currency crisis in these emerging markets could manifest in surprising ways. The 1997 Asian financial crisis and the 1998 Russian crisis contributed to the upheaval of Long Term Capital Management, while the 1994 Mexican peso crisis led to the bankruptcy of Orange County.

Given the extent of credit distributed over the last decade and the ongoing quest for yield, it’s likely we may witness the next crisis infiltrating unsuspecting American investment portfolios.

If you found this article insightful, consider subscribing to the Wealth Prism Letter for our latest market analysis, including The “Economic Collapse Investing” Strategy that Delivered 200% Returns Amidst the Stock Market Crash.

Sincerely,

MN Gordon

for Economic Prism