Following two consecutive months of broad increases in the major asset classes, June saw a return to losses across the board.

* A New York grand jury has indicted the Trump Organization and its CFO.

* The United States and Japan are conducting military exercises amid escalating tensions between China and Taiwan.

* The President of China has promised ‘complete reunification’ with Taiwan.

* The manufacturing PMI in China dropped to a three-month low in June.

* Fed’s Kaplan stated that the central bank should soon begin to reduce bond purchases.

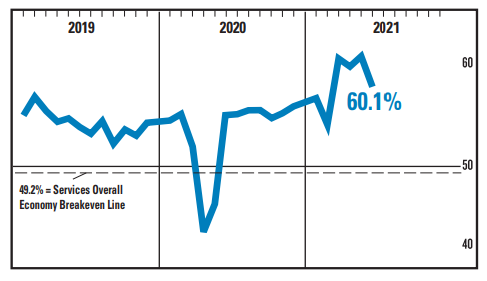

* The Eurozone’s manufacturing PMI rose to a record high in June.

* Pending home sales in the US showed a sharp rebound in May.

* Business activity in the Chicago area was unexpectedly weak in June.

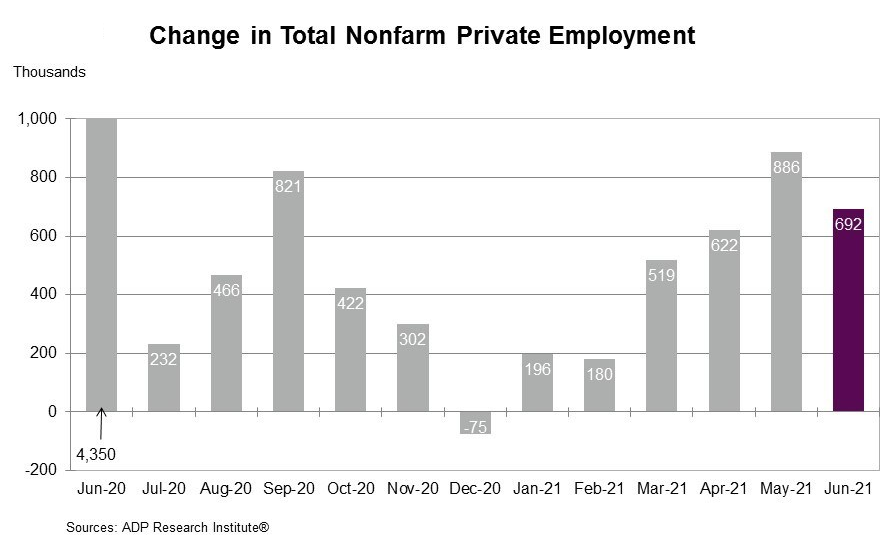

* US private employment increased by 692,000 in June, surpassing economists’ predictions:

The reflation trade appears to be diminishing in momentum, as indicated by the ongoing decline in the 10-year Treasury yield.

Energy stocks are enjoying a robust year, as reflected by traditional companies like Exxon Mobil and Chevron, which have seen significant rebounds after 2020’s downturn. In contrast, the broader alternative energy sector presents a mixed picture in 2021.

* Congress faces renewed calls to reform antitrust laws.

* A US infrastructure plan could stimulate growth and decrease debt, according to a study published recently.

* Economists anticipate multiple rate hikes in the US by 2023, as shown in a recent survey.

* Revised data indicates the UK economy contracted more than expected in Q1, according to reports.

* Eurozone inflation declined in June, preceding an expected rebound in summer.

* China’s manufacturing PMI dropped to 50.9, signaling modest growth in June.

* US Consumer Confidence reached a new high in June following the pandemic.

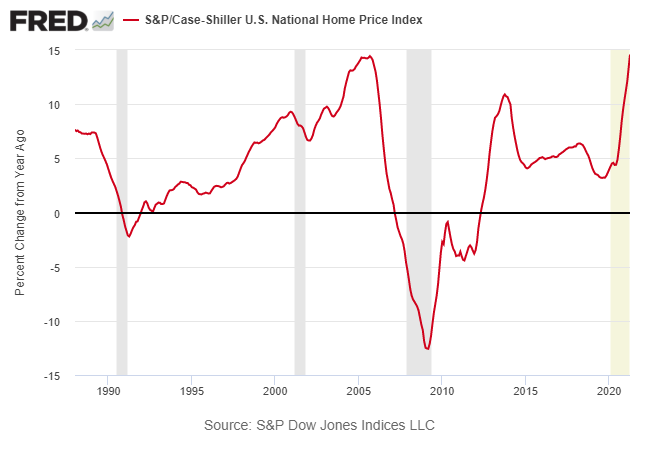

* The annual change in US home prices surged further in April, exceeding the peak levels of 2005:

In recent weeks, I have been developing models to estimate a theoretical “fair value” for the benchmark 10-year Treasury yield (see here and here). The objective is to combine these models to create a more reliable estimate by calculating the average. Consequently, the introduction of additional models strengthens our approach, and today I unveil a third method to econometrically approximate the ‘correct’ level of the 10-year rate.

* Militias have launched rocket attacks on US troops in Syria following airstrikes.

* A federal court dismissed an antitrust case against Facebook.

* The Delta variant is spreading, increasing the risk of potential Covid-19 spikes in the fall.

* A revival in US demand is driving global economic recovery.

* A drought in the US West will add to upward pressure on food prices.

* Discussions are underway about potential risks in the markets and the economy.

* Is fragility becoming the new normal in the US stock market?

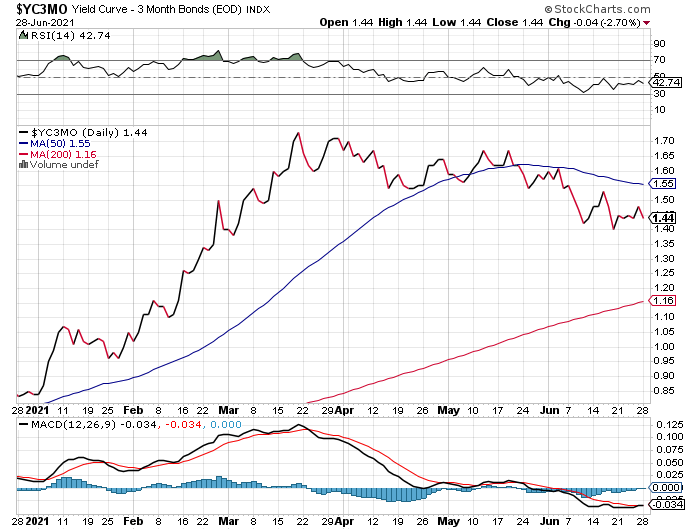

* The 10-year and 3-month Treasury yield curve continues to exhibit a downside trend:

Last week, nearly all segments of the major asset classes bounced back from the prior week’s correction, based on a variety of exchange-traded funds as of Friday’s close (June 25). The lone exception remains US investment-grade bonds.

* The US conducted airstrikes on militia targets in Iraq and Syria.

* White House and Senate negotiators are working to maintain the momentum of the infrastructure deal.

* A Fed official pointed out potential risks of a market decline following the US housing boom.

* Central banks are beginning or planning to withdraw emergency stimulus measures.

* A heatwave is scorching the Northwestern US states.

* President Biden seeks to shift the economic narrative from inflation to recovery, as reported.

* US consumer sentiment was slightly revised down for June, but remains higher than in May.

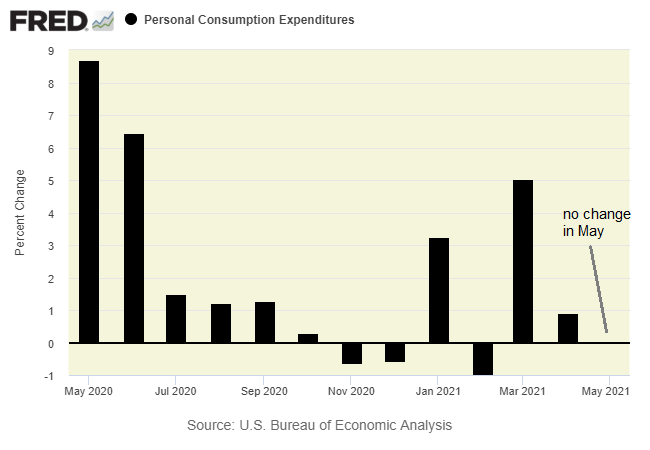

* US consumer spending stayed unchanged in May, while incomes fell for the second consecutive month:

Most international markets rebounded last week, bringing passive beta portfolios back to the forefront in terms of performance.

In summary, recent financial trends reflect a mix of rebounds and concerning indicators across various asset classes and global events. As the landscape continues to evolve, keen observation remains essential for anticipating future market movements.