Understanding the inverse relationship between prices and yields can prove to be beneficial, even if it’s not necessarily a stroke of luck. This dynamic has played a significant role since our last update on trailing yields for the major asset classes represented by ETF proxies. As prices have dropped, the discomfort has been somewhat alleviated by an increase in trailing yields.

* Leaders of Russia and China met at the Olympics in Beijing, denouncing US pressure.

* Global growth in January eased to its slowest pace in a year and a half, according to PMI survey data.

* US business activity slowed “notably” in January as per PMI reports.

* The Bank of England raised interest rates again to combat inflation.

* ECB President Lagarde hinted at a potential acceleration in policy tightening due to high inflation.

* Meta (Facebook) suffered a $250 billion loss in market value following disappointing earnings results.

* Amazon shares jumped due to a strong revenue increase in Q4.

* Eurozone retail sales declined more than anticipated in December.

* US jobless claims dropped for a second consecutive week, indicating a softer impact from Omicron.

* Factory orders in the US fell by 0.4% in December, aligning with expectations.

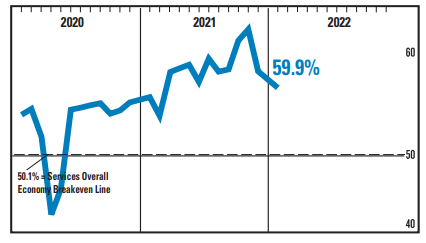

* The US ISM Services Index continued to decline in January, reflecting slower growth:

Following an extraordinary rise, the Global Market Index’s risk-adjusted performance experienced a downturn in January, as indicated by the trailing 3-year Sharpe ratio—a measure that assesses return relative to volatility. The decline was significant but not surprising, considering the considerable growth in preceding months. As previously highlighted, “History shows that sharp increases in GMI’s Sharpe ratio are typically followed by quick reversals, suggesting turbulent market conditions ahead.”

* NATO states that Russia increased military deployments to Belarus, Ukraine’s northern neighbor.

* Russia denounced the US decision to send additional troops to Europe.

* The Russian economy is prepared to face more sanctions.

* US special forces conducted a large-scale counterterrorism operation in northwestern Syria.

* Eurozone economic growth continued to slow in January, as indicated by PMI survey data.

* Persistently high Eurozone inflation is expected, according to the CEO of Nordea, a bank based in Denmark.

* Oil company Shell reported a significant increase in profit for the full year.

* Technology stocks may encounter renewed selling pressure following Facebook’s disappointing profit report.

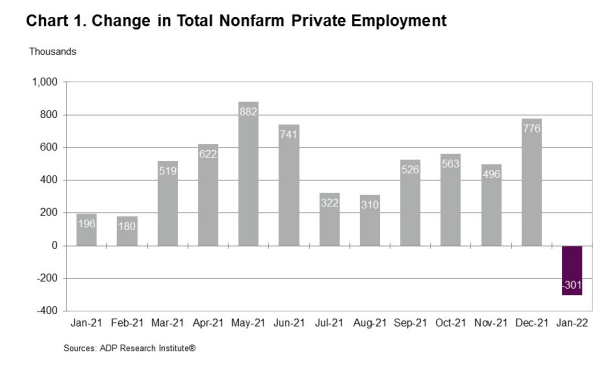

* US companies unexpectedly cut jobs in January, according to ADP estimates:

The anticipated risk premium for the Global Market Index (GMI) declined in January, falling below the 6.0% level for the first time since October. The revised forecast now stands at 5.9% annualized, reflecting a notable shift from the previous month’s estimate.

* Putin claims that the West has ‘ignored’ Russia’s essential concerns regarding Ukraine.

* While blaming the US for Ukraine tensions, Putin remains open to diplomacy.

* US consumer spending is shifting from goods to services.

* The US national debt has exceeded $30 trillion for the first time.

* Eurozone annual inflation rose to 5.1% in January—a record high.

* Global manufacturing output and new order growth slowed in January.

* Google parent company Alphabet reported strong revenue growth of 32% in Q4.

* Job openings in the US remained elevated, nearing 11 million in December.

* US construction spending continued to increase in December.

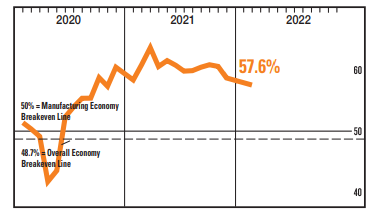

* The US ISM Manufacturing Index declined again in January but still indicates growth:

January saw a significant outflow of capital across most major asset classes, with some notable exceptions as evidenced by a range of ETFs.

* The Kremlin claims that the US is fueling ‘hysteria’ over Ukraine during a UN Security Council meeting.

* Richmond Fed President Barkin suggests that businesses are in favor of higher interest rates.

* The Eurozone jobless rate decreased to a record low in December.

* Eurozone manufacturing activity in January rose to a five-month high.

* German retail sales fell significantly more than expected in December.

* The New York Times acquired Wordle, the popular word game that became a hit.

* Growth in Texas manufacturing activity slowed in January, but outlooks remain positive.

* Economic activity in the Chicago area improved in January according to PMI sentiment data.

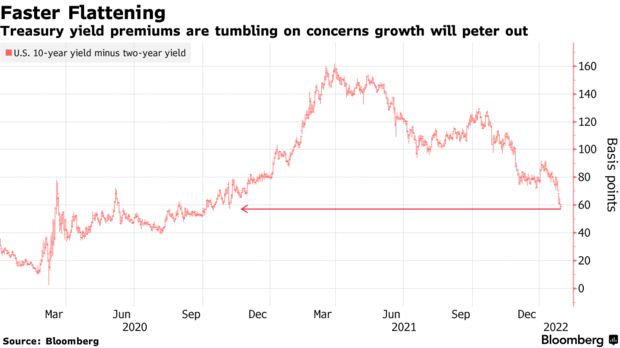

* The US 10-year to 2-year yield spread continues to decrease, reaching its lowest point since October 2020:

Despite a broader market downturn, US company shares and inflation-protected Treasuries managed to experience gains last week, according to a range of ETFs by the close on January 28.

* The White House cautions that the Omicron spike could impact this week’s job data update.

* The Atlanta Fed’s Bostic indicated the central bank may raise rates by a half-point if necessary.

* China’s manufacturing sector contracted in January, marking the weakest reading in 23 months.

* The Bank of England may be approaching its first consecutive rate hikes in 17 years.

* Eurozone growth slowed in Q4.

* Soaring prices for construction materials are likely to mitigate the risk of a housing bubble.

* US consumer spending dipped in December as inflation hit a 40-year high.

* The US 10-year to 2-year Treasury yield spread is at its lowest level since October 2020: