The current geopolitical landscape continues to evolve, particularly in light of ongoing developments in Ukraine. Here are some key updates regarding international relationships, economic impacts, and military developments:

- Ukraine requests additional support, asserting that Russia’s goal is to fragment the nation.

- Upholding territorial integrity is paramount, as Ukraine insists before negotiations with Russia.

- This week, President Biden’s comments regarding Putin have caused concern among Western allies.

- Defense contractors are evaluating increases in military budgets driven by the conflict in Ukraine.

- Europe’s economy is slowing as the war imposes significant economic strains.

- India is purchasing discounted Russian oil, with China potentially following suit.

- A portion of the Treasury yield curve has inverted for the first time since 2006.

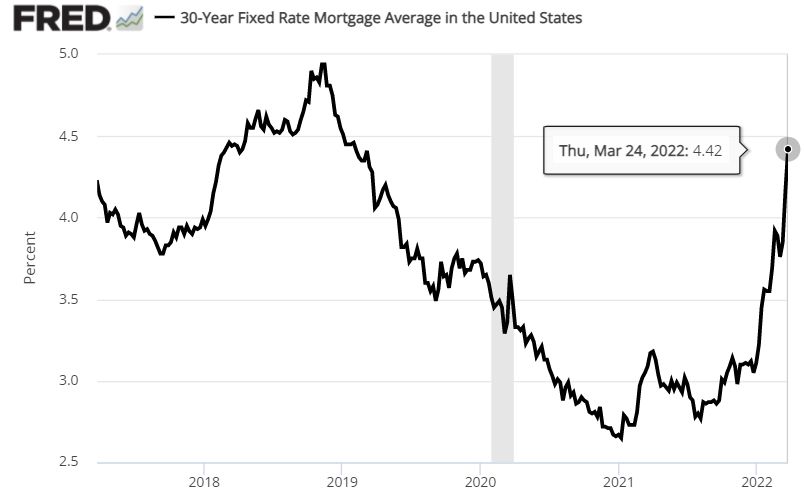

- The average 30-year mortgage rate in the U.S. has risen to a three-year high:

● In Defence of Wealth: A Modest Rebuttal to the Charge the Rich Are Bad for Society

Derek Bullen

Q&A with author via Grit Daily

Q: In your discussion on wealth creators, you refer to “the few who can invest, take risks, innovate, and transform their ideas into successful businesses that generate wealth and employment opportunities.” Do you believe that this would cease if hedge fund managers’ earnings were taxed as income instead of capital gains, or if marginal tax rates were increased by a few percentage points?

A: I indeed believe that excessive taxation can severely hinder the society that imposes it. Historically, taxing the rich has gained popularity but often leads to disastrous outcomes. Wealthy individuals tend to react to overtaxation by relocating or reducing their spending, and this is not merely opinion but a fact evidenced by several recent examples of tax increases in France and the U.S.

As the repercussions of the war in Ukraine begin to impact the global economy, early signs for the U.S. remain positive. While there is a long journey ahead, and it is still premature to make definitive forecasts, initial indicators from March suggest that economic growth is prevailing.

Here are some updates on key geopolitical and economic events:

- President Biden met with NATO allies, who are reinforcing troops in Eastern Europe.

- Poland has become America’s ‘indispensable’ ally during the ongoing Ukraine conflict.

- The EU has signed an agreement with the U.S. to enhance shipments of liquefied natural gas to Europe.

- Concerns mount over whether Putin may escalate his aggression if Russian forces become entrenched in Ukraine.

- Biden warns of impending food shortages stemming from the Ukraine conflict, stating the situation is serious.

- Germany’s leading economic indicator fell significantly in March due to the impacts of the Ukraine war.

- Speculation arises regarding how inflation might stabilize without triggering a recession.

- Durable goods orders in the U.S. declined for the first time in five months in February.

- U.S. business activity showed acceleration in March, according to PMI survey data.

- Weekly U.S. jobless claims dropped to their lowest level since 1969:

As volatility spiked in 2022, the previously stable correlations of returns across markets are starting to shift. This development suggests that our understanding of the relationships between markets—and the potential benefits of diversification—may need revision.

Key updates from global political discussions and market reactions:

- Biden is attending meetings in Brussels with NATO, G-7, and EU leaders.

- North Korea has launched an intercontinental ballistic missile, according to reports from Japan indicating increased tensions.

- Eurozone business activity slowed in March, based on PMI survey data.

- The Federal Reserve’s goal of achieving a soft landing for the economy seems increasingly unlikely.

- Oil prices rose following reports of an extended pipeline outage in Russia.

- Putin has announced that ‘unfriendly’ nations must pay for gas in rubles, creating uncertainty in global markets as a result.

- The invasion of Ukraine is seen as marking the end of globalization, as stated by BlackRock’s Fink in a recent letter.

- New home sales in the U.S. declined for the second consecutive month in February.

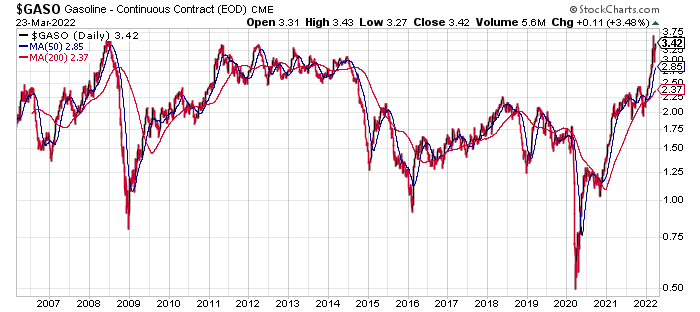

- Gasoline prices in the U.S. remain elevated, nearing the peaks seen in 2008:

Morningstar has recently observed that effectively assessing the U.S. labor market requires a comprehensive examination of various factors. They accurately predicted in December that a weak payroll report from November was “likely just a blip,” given the overall economic strength. This analysis encourages a deeper look into macroeconomic drivers essential for evaluating labor market activity.

Significant developments regarding global geopolitics:

- The U.S. and its allies are poised to announce new sanctions against Russia as President Biden travels to Europe this week.

- Debate continues over whether NATO should initiate a more direct response to the conflict in Ukraine.

- Concerns arise regarding potential disruptions to Europe’s clean energy transition due to the war.

- Global bond markets face their most significant drawdown on record since 1990.

- U.S. gasoline prices are increasing at the fastest rate ever recorded.

- UK inflation has reached a new multi-decade high of 6.2%, primarily driven by surging energy prices recently reported.

- Fed funds futures are indicating a greater than 60% chance of a half-point rate increase in May according to current predictions.

- The yield on U.S. 10-year Treasuries continues to rise, marking the highest level since May 2019:

While the prospect of a recession seems increasingly likely, mounting uncertainties make it difficult to assert high-confidence predictions at this moment. For now, the landscape remains uncertain as experts continue to speculate on potential outcomes.

The European Union is increasingly supporting a ban on Russian oil imports. Awareness of potential Russian cyber threats to the U.S. has also been brought to light, as President Biden cautions against the growing risks.

- Fed Chairman Powell has stated that rates will increase more aggressively if necessary, in response to soaring inflation.

- Comments made by Powell about addressing inflation have served as a wake-up call for Wall Street.

- Powell has also indicated that the short-term yield curve could be a better predictor of recession risks moving forward.

- Economists foresee a “substantial downshift in activity” within the U.S. housing market, and predict drops of around 25% in home sales by the summer.

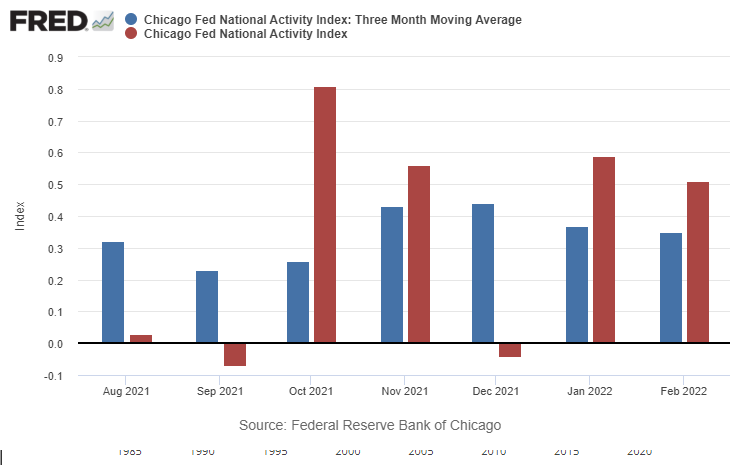

- Despite these concerns, U.S. economic growth remained solid in February according to the Chicago Fed index.

### Conclusion

The ongoing conflict in Ukraine continues to reshape global geopolitics and economic conditions. As countries evaluate their positions and responses, the interconnectedness of international relations becomes increasingly evident. Monitoring these developments is vital as they will likely influence political, economic, and social landscapes worldwide.