This year, energy remains the standout performer in the US equity market, showcasing remarkable upward momentum. To illustrate the current situation in 2022, a significant divergence continues to favor energy shares, as indicated by sector ETFs through the close of trading on May 3.

* The European Union proposes a gradual ban on Russian oil as part of new sanctions.

* The second-largest fertilizer producer globally may face sanctions from the European Union.

* Tensions in Asia escalate as another North Korean missile launch occurs.

* The Federal Reserve is expected to raise its policy rate by 50 basis points today.

* Can the Fed control inflation without triggering a recession?

* The Bank of England faces what some describe as an inflationary spiral.

* Guggenheim Partners’ CIO predicts that interest rates could rise continuously for a generation.

* Beijing restricts public transportation as COVID-19 cases increase.

* March saw a sharp decline in German exports, marking the first significant data reflecting the impact of the Ukraine conflict.

* US factory orders increased significantly in March, exceeding estimates.

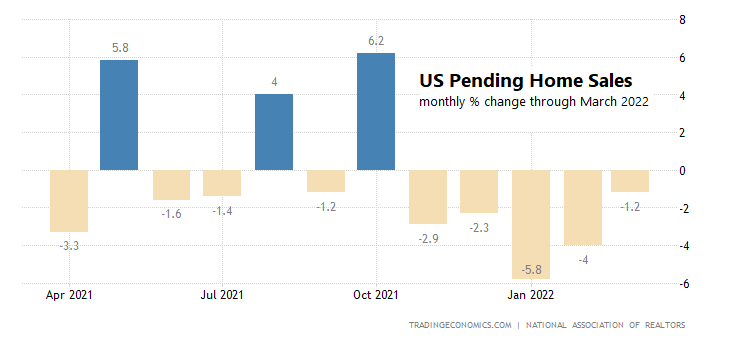

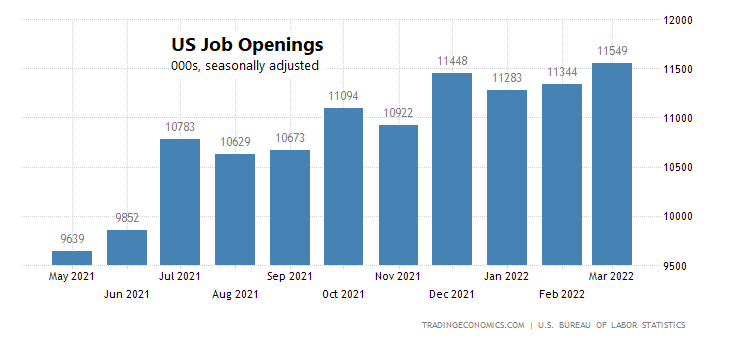

* The number of job openings in the US in March reached a series high:

The anticipated risk premium for the Global Markets Index (GMI) continued to decline in April. The latest revision shows a drop to a 5.4% annualized increase for the long term, a substantial adjustment of 40 basis points from last month’s forecast. This newly adjusted estimate reinforces the discussion about managing expectations for globally diversified multi-asset portfolios in light of actual returns over recent years.

* A leaked document indicates the Supreme Court is poised to overturn abortion-rights precedent, suggesting a significant change.

* The European Union is preparing to propose a phased ban on Russian oil.

* Concerns arise about a potential Federal Reserve error as Wednesday’s policy decision approaches.

* Is the era of plentiful, low-cost supply coming to an end?

* The Bank of England is expected to raise interest rates to a 13-year peak.

* Australia has also raised interest rates for the first time in over ten years.

* China’s manufacturing is slowing further as indicated by the April PMI survey.

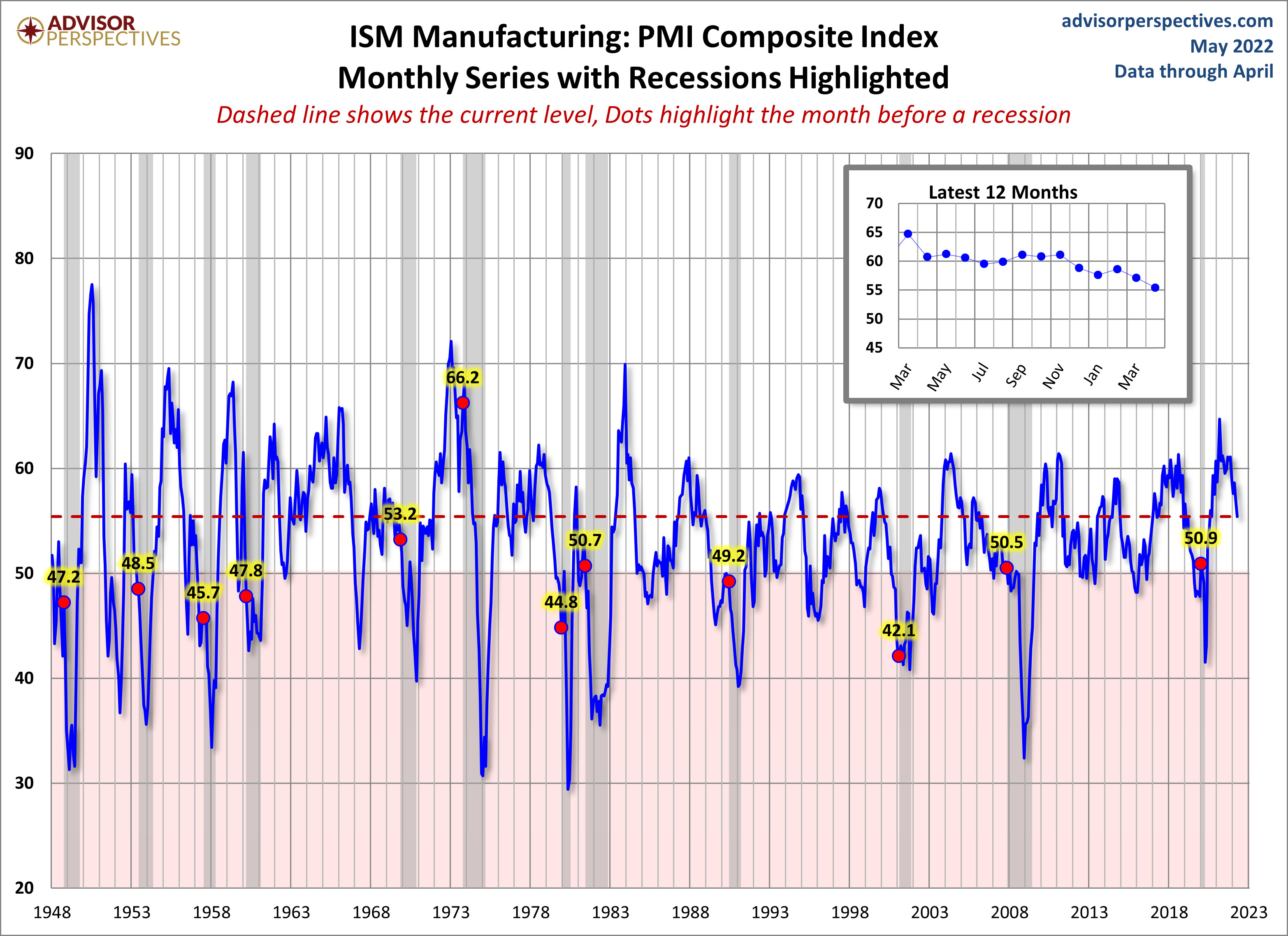

* The US ISM Manufacturing Index fell again in April, yet still points to moderate growth:

April turned out to be a difficult month, with losses seen across nearly all major asset classes, with commodities being the only notable exception that managed to post gains. For the rest, declines dominated, based on a collection of ETF proxies.

* EU energy ministers are in crisis talks regarding Russia’s energy supplies.

* Unconfirmed reports about Putin’s health have surfaced.

* Fed funds futures anticipate a 0.5% rate hike at the Fed meeting this week.

* Three indicators suggest inflation may be peaking.

* Despite surging inflation and slowing growth, experts do not foresee stagflation.

* Consumer staples stocks are gaining attention among cautious investors.

* The looming threat of recession is a primary concern for institutional investors.

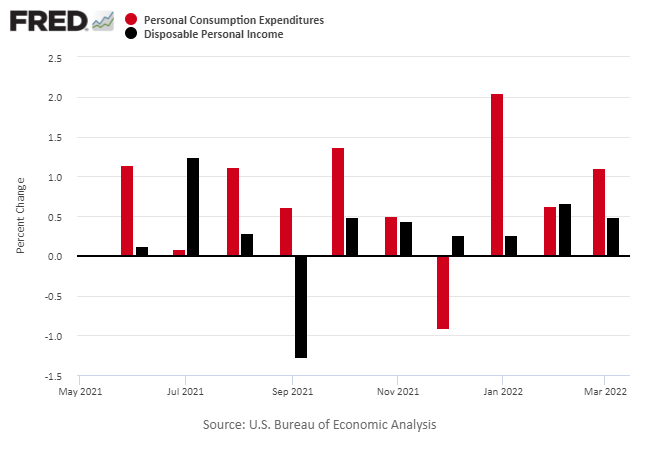

* US consumer spending increased for the third consecutive month in March:

Gary Gerstle

Review via Financial Times

In what is truly a rare occurrence, the term “instant classic” fits perfectly for Gary Gerstle’s latest work, The Rise and Fall of the Neoliberal Order.

This book contextualizes neoliberalism—defined by free trade and the unimpeded flow of capital, goods, and people as well as deregulation and cosmopolitanism—within a century’s historical narrative, essential for comprehending the current political climate in both the US and worldwide. It intricately weaves together complex economic, political, and social developments over the last 100 years, creating a compelling narrative about America’s past and potential future.

Modeling the returns of financial assets remains an intricate task, as no single model can fully encapsulate the complexities of asset performance. Consequently, analysts often find themselves choosing a method that they consider the least inaccurate among the available options.

* NATO has announced its readiness to support Ukraine for an extended period.

* UBS asserts that now is not the time to prepare portfolios for a recession or Fed failure.

* The Eurozone inflation has achieved a new record high in April, continuing to escalate.

* The risk of stagflation is increasing for Europe amid slowing growth.

* Jobless claims in the US remain near a 50-year low, as reported last week.

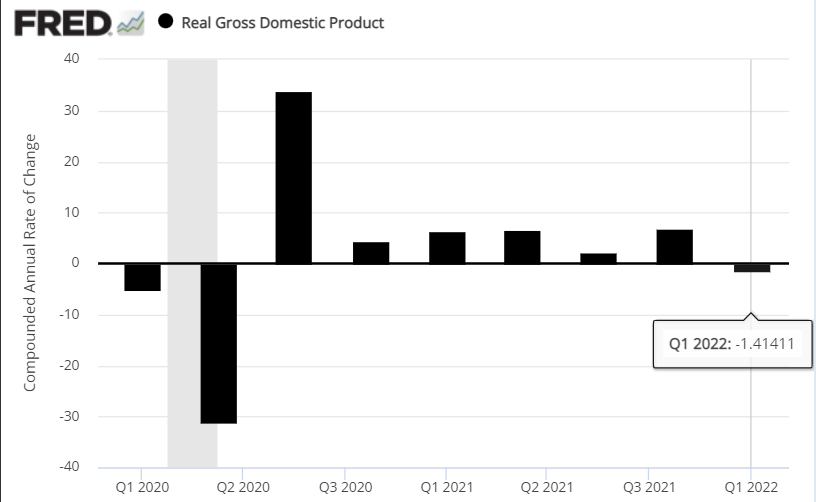

* Despite a decline in Q1 GDP, economists foresee a rebound in growth for the remainder of 2022 according to expectations.

* The US economy contracted by 1.4% in the first quarter, which fell short of projections:

The US stock market is currently leaning towards a bearish trend as the S&P 500 Index tests the lows of 2022. Ongoing challenges stem from a multifaceted blend of factors, including the fallout from the Ukraine war, persistently high inflation, increasing interest rates, and decelerating economic growth. The prevailing risk elements are likely to endure in the near future, suggesting that the market will remain cautious.