The Capital Spectator is enjoying an early summer break, heading to Hawaii for some well-deserved time off. This temporary shift in focus will allow your editor to explore the local wildlife and flora, resulting in limited updates for a while. Expect to see the usual content resume on Wednesday, June 8. Aloha!

A day to remind us that freedom isn’t free.

● Fossil Future: Why Global Human Flourishing Requires More Oil, Coal, and Natural Gas–Not Less

Alex Epstein

Interview with the author via Reason

Two commonly held beliefs today are that fossil fuels are leading to an impending global disaster and that renewable sources like solar and wind can meet our energy demands either now or soon.

Epstein disputes both claims. He acknowledges that fossil fuels contribute to climate change but argues that they enhance our ability to manage and adapt to our environment. He contends that the potential of renewables is insufficient to meet our growing needs. According to him, humanity is thriving due to the capabilities provided by oil, gas, and coal, which enable us to survive in a world that would otherwise be hostile to our existence. Wind and solar currently account for only 3% of the energy mix; he warns that a rushed transition to renewables could lead billions into poverty or worse, as the impacts of climate change—often overstated—are not beyond our capacity to manage.

* Europe is planning for a possible cessation of Russian gas imports.

* China’s industrial profits declined in April—the first fall in two years.

* US mortgage rates dropped for the second week running, although they remain above 5%.

* Zuckerberg acknowledged that Meta’s metaverse initiative is expected to incur ‘significant’ losses over the next five years.

* Concerns about stagflation are increasing.* The decline in US GDP for the first quarter was worse than previously estimated.

* Last week saw a decrease in US jobless claims, indicating a tightening labor market.

* The policy-sensitive 2-year Treasury yield has slipped to a five-week low:

Despite increasing challenges for the global economy, recent estimates suggest that US economic output remains on track for a rebound in the second quarter.

* The World Bank chief warns that Russia’s invasion of Ukraine could lead to a global recession.

* Minutes from the Fed officials indicate an agreement to accelerate interest rate increases, as shown in the minutes.

* According to the CBO, US inflation and economic growth are expected to cool later this year, forecasts suggest.

* Two investment banks have revised their China GDP forecasts downward for the third time this year.

* The economic downturn in China shows no signs of recovery.

* China’s cabinet convened an emergency meeting to restore economic stability, as reported.

* A negative market reaction, despite solid earnings, may indicate the onset of a bear market.

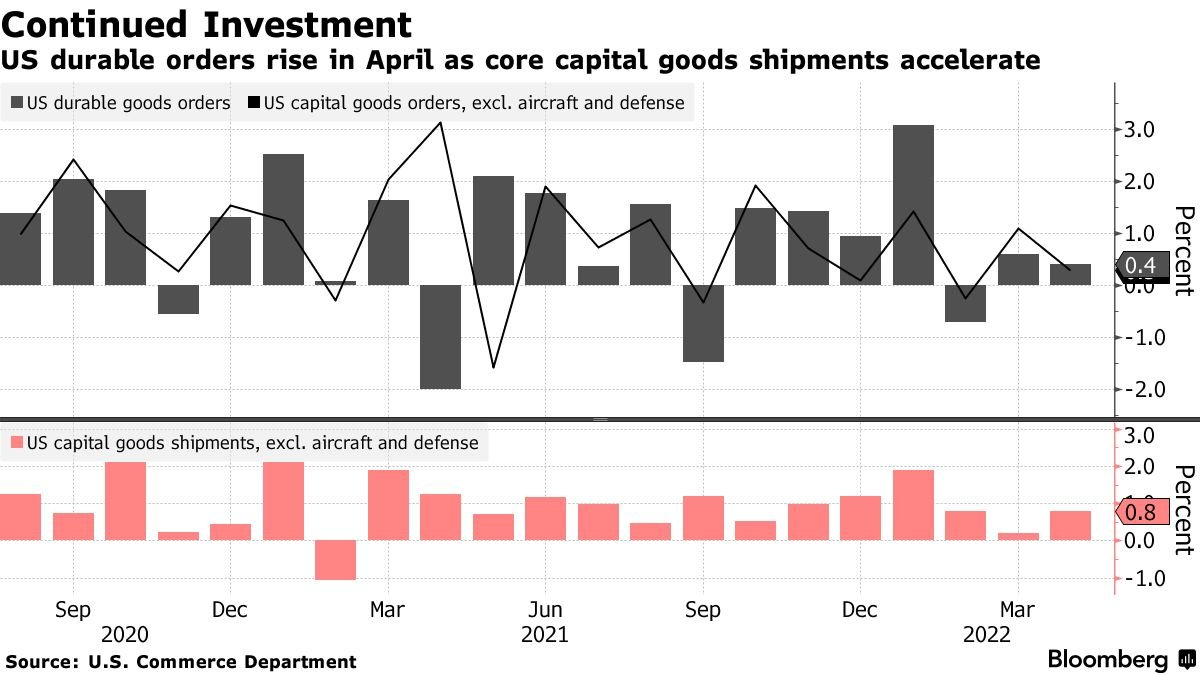

* US durable goods orders rose for the second consecutive month in April:

After months of rising Treasury yields, the current discussion revolves around whether these rates have peaked, spurred by recent declines. With three trading days remaining this week, the widely monitored 2-year and 10-year Treasury yields are poised to record their first series of three-weekly decreases this year.

* Investors are increasingly concerned that recession may overshadow inflation as the primary worry.

* China is pursuing a security deal with ten Pacific island nations.

* The economic forecast for China is weakening due to the impacts of its zero-Covid policy.

* Pfizer’s CEO predicts ‘constant waves’ of Covid will continue, suggesting ongoing challenges.

* A policy shift by the US Treasury Department could trigger a historic default in Russia.

* There’s ongoing debate regarding whether tech is boosting US productivity, with evidence lacking.

* New home sales in the US declined for the fourth consecutive month in April.

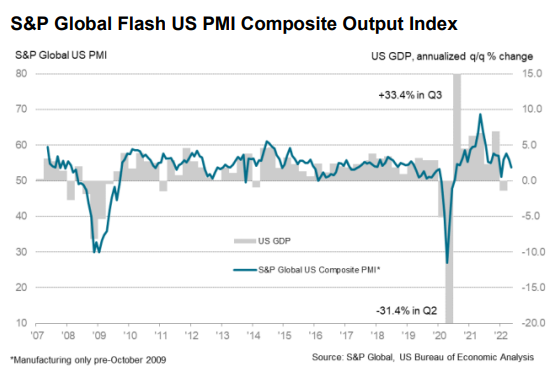

* Growth in the US slowed more than anticipated in May according to PMI survey data.

Various factors contribute to consumer price inflation, but the impact of oil prices often takes center stage. Recent declines in crude oil prices suggest that we may have reached a peak in inflationary pressures at the headline level.

* US-China relations have become strained following Biden’s remarks about defending Taiwan.

* The US’s stance on trade with China remains unclear.

* The European Union’s embargo on Russian oil imports is expected within days.

* Growth in the Eurozone is ‘robust’ in May, according to the PMI Composite Index survey data.

* The chief of the ECB has stated that the central bank is in no hurry to tighten monetary policy.

* The trend of the Great Resignation is set to continue, with one in five people considering a job change, according to a new global survey.

* Is Spain becoming the solution to Europe’s energy issues related to Russia?

* Growth in the UK private sector has slowed to the lowest pace since winter 2021.

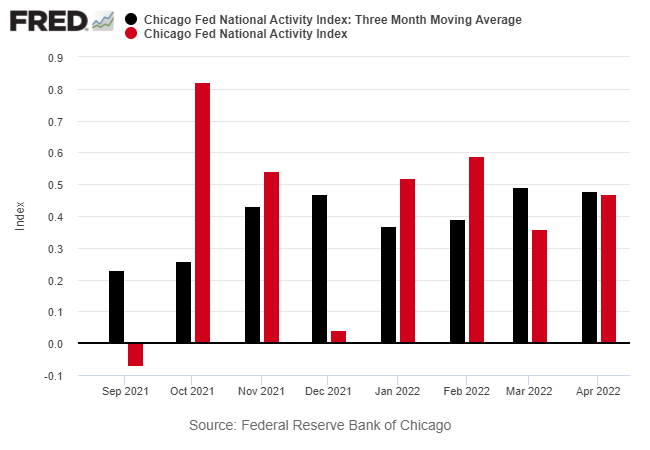

* The US saw a robust economic performance in April, per the Chicago Fed National Activity Index:

This collection of articles highlights a range of significant economic trends and events. As we navigate complex issues such as inflation, energy needs, and global relations, staying informed is essential. Whether it’s a temporary break in publication or crucial warnings about the economy’s direction, each piece serves to enrich our understanding of the world around us.