Recent global events have created significant ripple effects across various sectors:

- Ukraine seeks increased Western military support post-Russian setbacks.

- The impending US railroad strike is set to begin, presenting additional challenges for the economy.

- The Federal Reserve is expected to implement another 75bps interest rate hike next week, according to a Reuters poll.

- JP Morgan analysts forecast a higher likelihood of a soft landing for the US economy.

- Small business sentiment in the US showed moderate improvement in August.

- US banks experienced a record decline of $370 billion in deposits during Q2.

- The UK jobless rate reduced to its lowest level in 48 years as of July.

- Investor sentiment in Germany has further deteriorated in September.

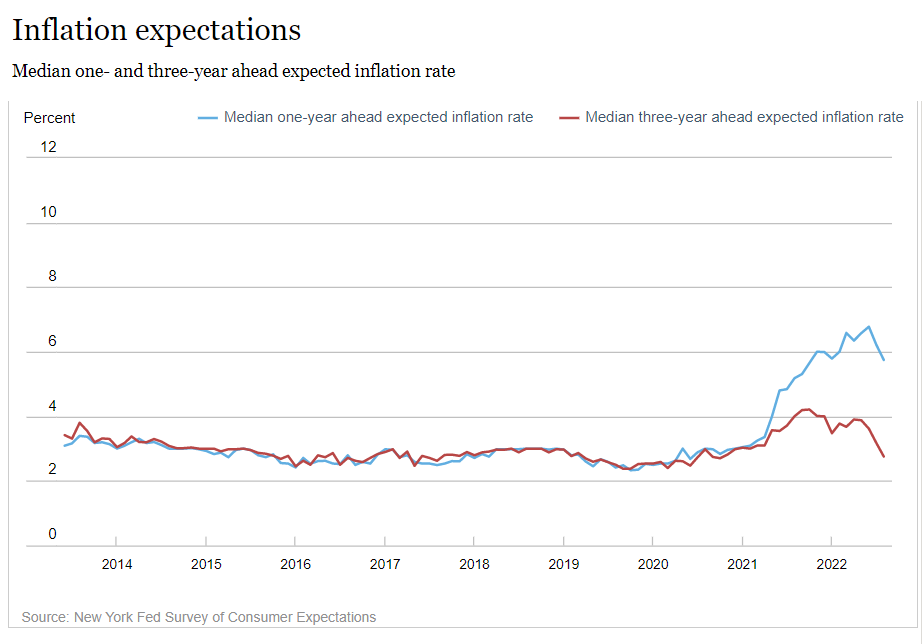

- Inflation expectations dropped once again in August per a survey conducted by the NY Fed.

In the trading week ending September 9, a rally in risk assets was noted, according to various proxy ETFs representing major asset classes. While there is optimism regarding the rally’s sustainability, confidence remains mixed.

Recent developments have shifted the global landscape:

- Ukraine’s counteroffensive has successfully reclaimed significant territory from Russian control.

- Potential railway and port strikes could disrupt supply chain recovery efforts.

- Fed’s Waller has indicated support for a ‘significant increase in the policy rate,’ according to CNBC.

- Concerns arise about whether the Fed’s withdrawal of support could create disturbances in the US Treasury market.

- Treasury Secretary Yellen has warned that oil prices may see a spike this winter due to market dynamics.

- Several industries suggest a potential easing of US inflation indicators in August, as reports indicate.

- The UK recorded growth below expectations for July.

- The passing of the Queen may ignite new movements for self-governance in former British colonies.

- The US 10-year yield is approaching levels seen in June:

In the book, ● Slouching Towards Utopia: An Economic History of the Twentieth Century by J. Bradford DeLong discusses significant economic transformations between 1870 and 2010.

In a recent Q&A with Vox, DeLong argues that these years were “the most consequential in human history,” citing the unprecedented technological advancements during this timeframe. He notes that the progress made reflects more drastic changes than occurred between 6000 BC and 1870 AD.

Before 1870, history primarily documented how elites leveraged power to dominate impoverished populations for survival, contrasting with the developments seen since that have shaped modern society.

In a recent article, I discussed a methodology for estimating the S&P 500’s two-year annualized return one year out. While the approach isn’t foolproof, it provides a useful framework for short-term forecasting. However, I apologize for the lack of clarity in that explanation, as I received numerous inquiries for further details.

Allow me to clarify and expand on the methodology used for predictions.

Recent developments have highlighted high levels of uncertainty in various sectors:

- The passing of the Queen arrives during a period of significant unpredictability for the UK.

- Powell stated that the Fed will increase interest rates as necessary to combat inflation “until the job is done.”

- The European Central Bank has initiated a record rate hike to tackle inflation.

- European energy ministers are contemplating measures to intervene in the energy markets.

- China reported a greater-than-anticipated slowdown in inflation for August amid ongoing COVID-19 restrictions.

- A deadline nears for a US rail strike, potentially costing the economy $2 billion each day.

- The US jobless claims dropped to their lowest levels since May.

- US stocks appear poised for their first weekly gains in a month:

Navigating the market landscape has been challenging, particularly for equities in a year marked by significant downturns across the board. While some sectors of risk factors are performing better than others, market dynamics are heavily influenced by broader trends in 2022, according to a collection of proxy ETFs.

Recent US developments indicate significant financial commitments and ongoing concerns:

- The US has approved $2.7 billion in additional aid for Ukraine.

- Fed Vice Chair Brainard affirmed the central bank’s dedication to curbing inflation.

- According to the Fed’s Beige Book, recent US economic activity remains generally stable since early July.

- China has extended lockdowns in the mega-city of Chengdu.

- Climate change is anticipated to intensify challenges within global supply chains.

- Japan’s economy expanded more than initially predicted in Q2.

- The phenomenon of ‘quiet quitting’ is reportedly prevalent among half of the US workforce.

- A decline in the bond market is impacting Treasuries and corporate bonds.

- Discussion around a potential soft landing for the US economy is ongoing.

- Crude oil prices have reached a seven-month low as of Wednesday:

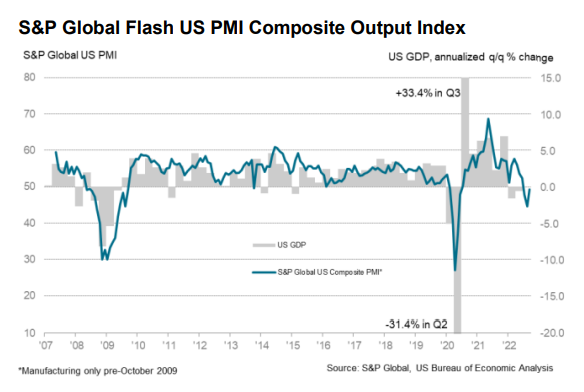

Recent revisions to US economic forecasts for the third quarter indicate a potentially stronger recovery compared to earlier estimates. According to a set of nowcasts compiled by CapitalSpectator.com, growth indicators remain cautiously optimistic, despite the influence of a significant outlier. The general outlook suggests a rebound in the forthcoming Q3 GDP data release from the Bureau of Economic Analysis.

Global developments continue to impact economic stability:

- The melting ‘Doomsday glacier’ in Antarctica could raise sea levels by several feet.

- US tech companies receiving government funding are prohibited from establishing tech factories in China.

- Global manufacturing activity contracted in August, marking the first decline since June 2020.

- China’s export growth slowed in August.

- Putin has called for a review of the UN-brokered grain deal.

- German industrial output continues to decline in July.

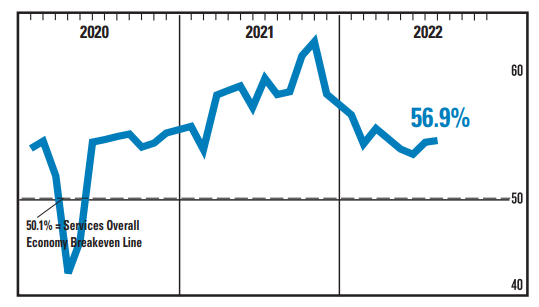

- US Services PMI indicates a deepening sector contraction in August; however…

- the ISM Services Index suggests a more optimistic scenario of moderate, steady growth: