Last week, global markets were impacted by pessimistic views on economic growth, interest rates, and inflation, as demonstrated by a series of proxy ETFs that track major asset classes, concluding with Friday’s close on September 16.

* Biden reiterates US commitment to defend Taiwan against a potential Chinese attack.

* Pandemic officially declared ‘over’ by Biden.

* Markets brace for a significant interest rate hike from the Federal Reserve this week.

* Rising bond yields alter stock market expectations.

* A strong US dollar threatens to worsen a global economic slowdown.

* Some European factories are shutting down due to skyrocketing energy costs.

* Hurricane Fiona ravages the Dominican Republic and Puerto Rico.

* Millions evacuated in Japan as Typhoon Nanmadol strikes.

* US 10-year Treasury yield rises for the seventh consecutive week as of Friday’s close:

● Superabundance: The Story of Population Growth, Innovation, and Human Flourishing on an Infinitely Bountiful Planet

Marian L. Tupy and Gale L. Pooley

Essay by author (Tupy) via The Spectator

According to our analysis, the trend of abundance has been doubling approximately every two decades. This means that a 60-year-old Westerner has witnessed their standard of living increase repeatedly—first from one to two, then from two to four, and from four to eight throughout their life. While this may seem slow, historically, life remained largely unchanged for thousands of years prior to the mid-18th century, and such stagnation was perceived as normal. Generations passed without any noticeable enhancements to their daily lives. Furthermore, the potential for future improvements is vast.

The disadvantages of rising interest rates are evident both locally and globally. However, there are positive aspects as well: higher yields emerge from risk assets that are experiencing price declines, leading to improved trailing payout rates.

* The World Bank forecasts an increased risk of recession in 2023 due to global rate hikes.

* Putin acknowledges that China has ‘questions and concerns’ regarding Russia’s conflict in Ukraine.

* China’s retail sales and industrial output exceed expectations for August.

* US industrial output drops in August, even though manufacturing activity shows improvement.

* US jobless claims decline for the fifth consecutive week.

* Worker strikes increase as demands for wage adjustments rise.

* Gold prices fall to levels seen during the pandemic in 2020 due to the impact of anticipated rate hikes.

* The Philly Fed Manufacturing Index declines in September.

* The New York Fed Manufacturing Index recovers in September.

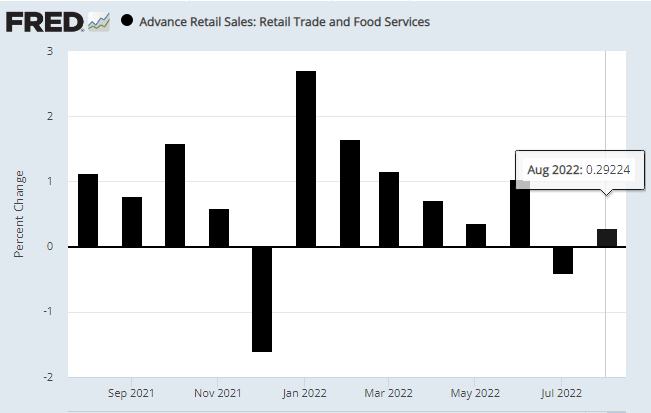

* US retail sales show improvement in August, exceeding expectations:

Recent market trends suggest a return to risk-off sentiment; the environment may have never fully shifted away from it. There are various methods to evaluate this situation. Let’s examine one that leverages market data through ETF pairs to gain real-time insight, as of the close on September 14.

* China’s Xi and Russia’s Putin conduct a summit.

* US rail strike averted following a tentative agreement.

* The policy-sensitive 2-year Treasury yield briefly exceeds 3.8%.

* Mortgage rates surpass 8% for the first time since 2008.

* Demand for mortgages drops significantly as interest rates rise.

* Increased rental prices contribute significantly to inflation.

* Wholesale inflation in the US falls to 8.7% in August.

* California has filed a lawsuit against Amazon, alleging violations of antitrust laws.

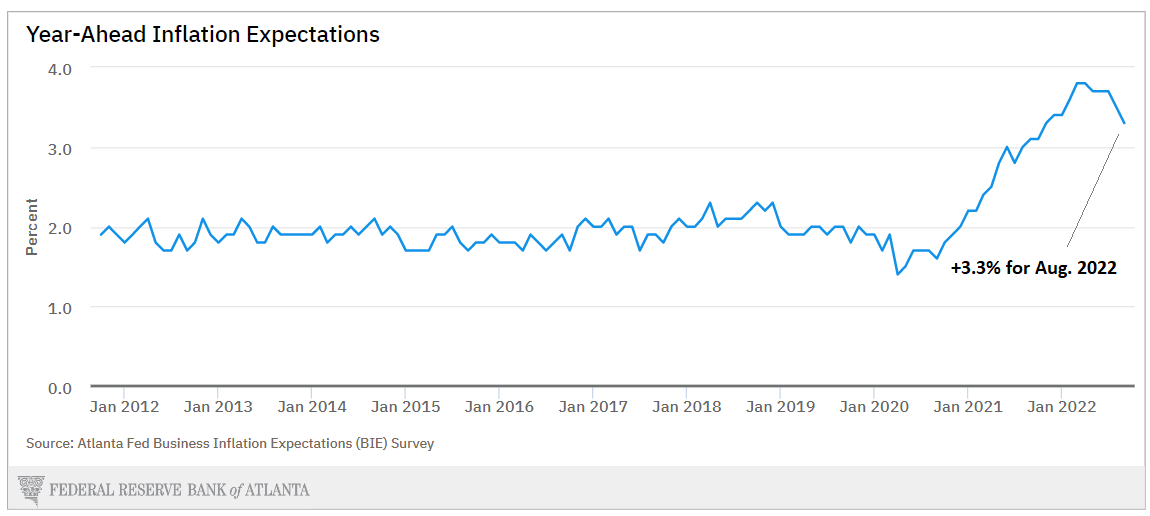

* Business inflation expectations have dropped to a 9-month low according to an Atlanta Fed survey.

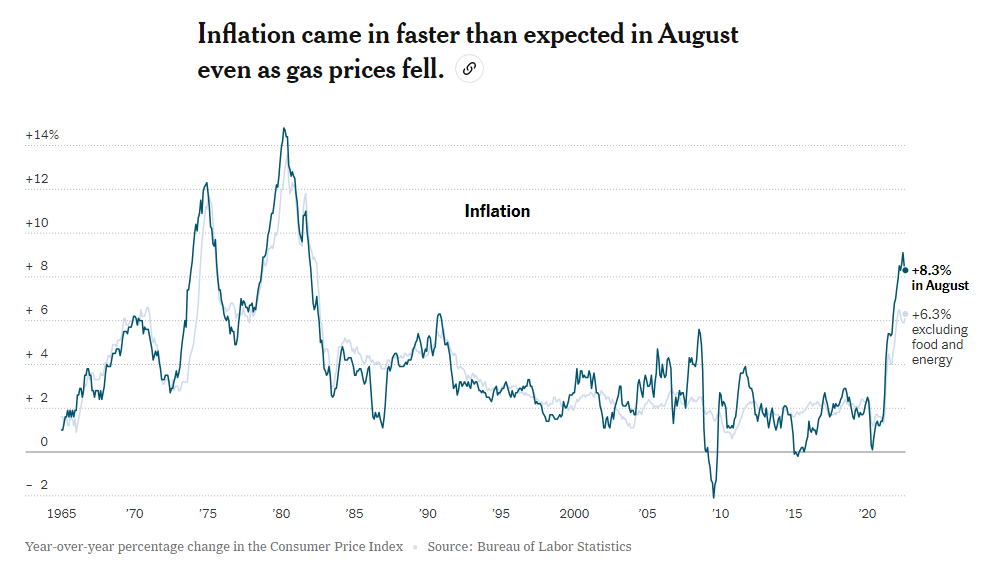

While inflation may have reached its peak, the decline is occurring at a slower pace than anticipated, tapering off gradually depending on the measurement used. The ongoing persistence of inflation has emerged as a new concern.

* Signs of US inflation becoming more persistent emerge.

* The policy-sensitive 2-year Treasury yield rises above 3.79%, the highest level since 2007.

* Xi and Putin are expected to discuss the Ukraine war during an in-person meeting.

* China is benefiting from an energy windfall as the West boycotts Russian supplies.

* US consumer confidence improved in August, marking the largest rise since March 2021.

* Americans experienced two consecutive years of stagnant or declining household income.

* The EU upheld an antitrust ruling against Alphabet, Google’s parent company.

* The UK inflation rate unexpectedly drops to 9.9%, though still remains high.

* Eurozone industrial output falls significantly in July.

* The pace of US consumer inflation slows less than anticipated in August:

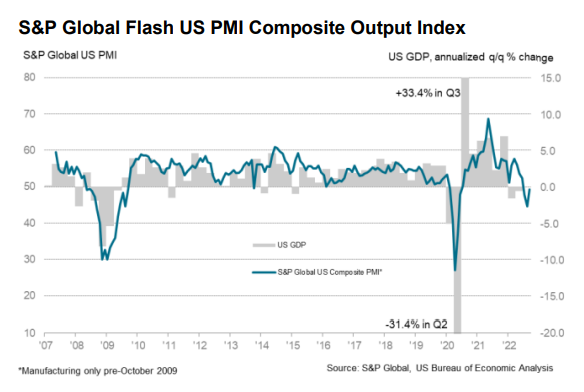

With slow growth, increasing interest rates, persistent inflation, and numerous other risk factors, there are fears that the US economy may slip into a recession soon. Analysts and economists deliver these warnings consistently. While it can be tempting to overlook these predictions, available data suggests that US economic activity continues to defy the pessimistic outlook, at least for the moment.

In a world marked by economic uncertainty, the information provided highlights critical trends and events that shape market dynamics. Analysts caution about rising interest rates, potential recession risks, and global developments that affect economic stability.

Overall, as we monitor these events, it becomes increasingly essential to remain informed and adaptable in response to an ever-evolving financial landscape. Keeping an eye on these trends can aid in understanding the broader economic implications for both markets and individuals.