Global Economic and Political Updates

In recent news, a variety of critical issues are shaping both the global economy and political landscape:

- The US warns Russia of severe repercussions should nuclear weapons be deployed in Ukraine.

- The far-right leader is likely to become Italy’s next prime minister.

- Tropical Storm Ian is forecasted to strengthen into a hurricane as it heads towards Florida.

- The British pound has dropped to a record low against the dollar.

- The ongoing war in Ukraine is projected to cost the global economy $2.8 trillion by the end of 2023, according to the OECD.

- Efforts to profit from “buying the dip” in the stock market aren’t yielding results this time around.

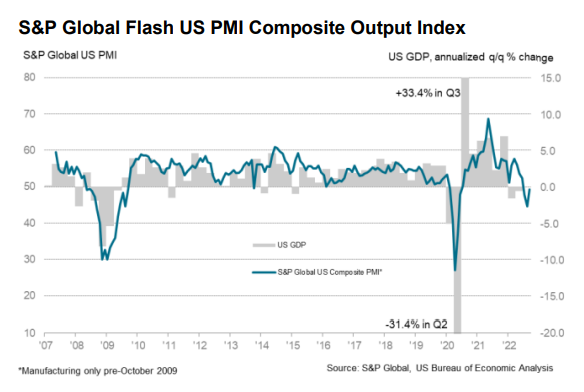

- According to PMI survey data, US business activity continued to contract in September.

● The Invention of Tomorrow: A Natural History of Foresight

Thomas Suddendorf, et al.

Review via Psychology Today

The human capacity for foresight, while imperfect, is a remarkable trait that fuels our ability to envision and plan for the future. In “The Invention of Tomorrow: A Natural History of Foresight,” authors Suddendorf, Redshaw, and Bulley explore the mechanics behind foresight, its development, and its evolutionary background. The book is meticulously researched and offers captivating insights, making it highly recommended for readers interested in this topic.

As more evidence emerges of a bear market in stocks, attention is turning to indicators that could signal when the decline has reached its limits, hinting that the market may have hit a bottom. Multiple methods exist for analyzing this data, each with its own limitations. However, the onset of interest rate cuts could serve as a crucial first indicator of recovery.

Several significant developments in global affairs have taken place recently:

- Kremlin-run voting began in Russian-occupied regions of Ukraine last Friday.

- Central banks worldwide increased interest rates following the Fed’s actions.

- The US Leading Economic Index declined for the sixth consecutive month in August.

- Pessimism among investors has returned to levels reminiscent of 2008, according to a Bank of America survey.

- The Eurozone faced a deepening contraction in September, according to PMI data.

- Business activity in the UK declined at the fastest rate since January 2021, based on PMI figures.

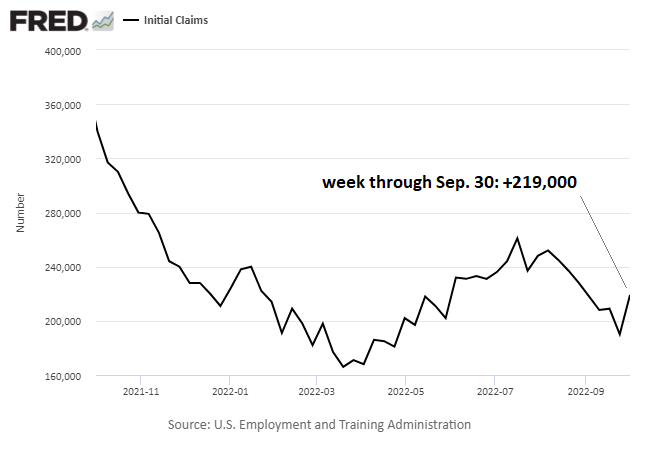

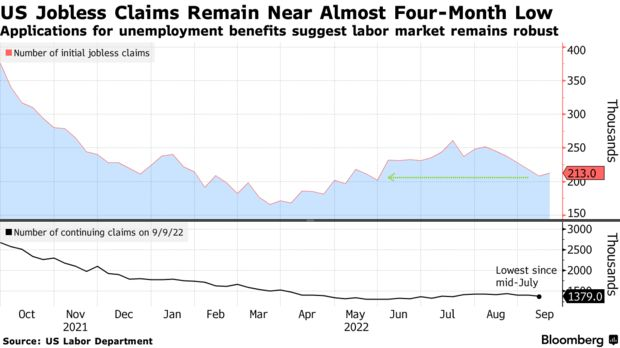

- US jobless claims increased slightly last week, although they remain close to historical lows.

During yesterday’s press conference, remarks from central bank leaders were unusually clear. For those still uncertain about the future trajectory of monetary policy, it appears they were not paying full attention.

Recent geopolitical events have raised concerns and prompted reactions from various leaders:

- NATO’s chief condemned recent nuclear threats from Putin.

- The Federal Reserve raised interest rates again, marking the third consecutive hike of 0.25 percentage points.

- Chairman Powell indicated that a recession might be a necessary consequence of reducing inflation.

- The Fed is expected to raise rates to 4.6% to combat inflation pressures.

- The Bank of England faces increased pressure for a significant rate hike.

- Home sellers are becoming less frequent, as rising rates deter homeowners from moving.

- The Yen has gained value after Japan’s first currency market intervention since 1998.

- With Switzerland’s recent rate hike, Japan remains the last holdout with negative rates.

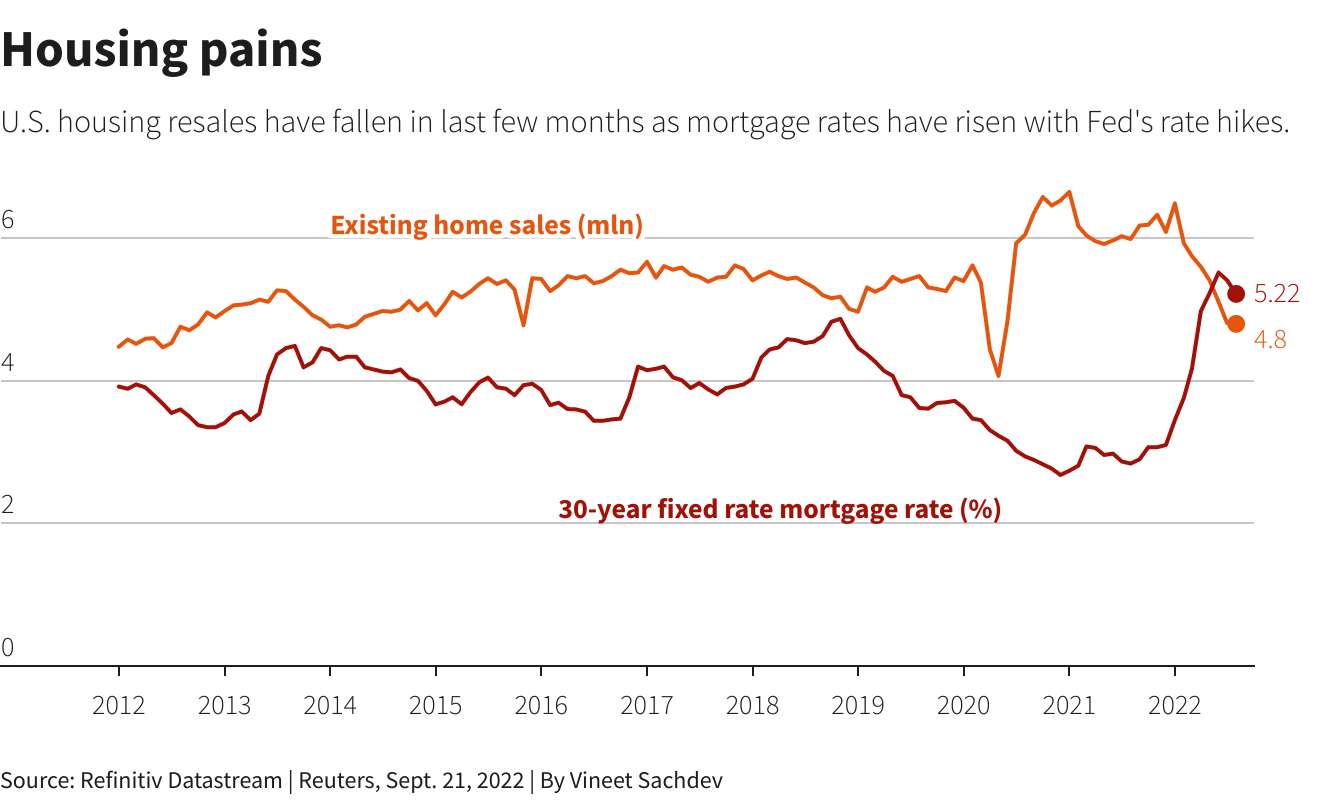

- US existing home sales declined for the seventh consecutive month in August.

The Federal Reserve’s decision to raise interest rates is anticipated to happen today, with a hike of 75 basis points largely expected. However, clarity on the pace and length of tightening monetary policy remains elusive. The lack of definitive answers poses a primary risk for the markets, and investors are keenly focused on discerning where the terminal interest rate might be.

Recent geopolitical developments are altering the landscape:

- Russia has announced a partial mobilization of its citizens amid the escalating conflict in Ukraine.

- The Federal Reserve is expected to raise interest rates by 75 basis points today.

- US and Canadian naval vessels traversed through the Taiwan Strait.

- Germany has nationalized Uniper, an energy giant, amid the ongoing energy crisis.

- Emerging economies in Asia are set to outpace China’s growth.

- European corporations are reassessing their business plans regarding an increasingly isolated China.

- An economist at Capital Economics predicts a return to disinflation.

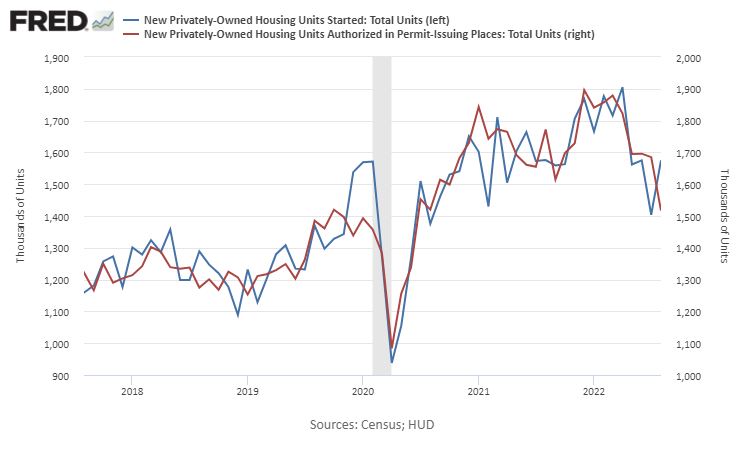

- US housing starts rebounded in August, even as new permits experienced a decline.

The Federal Reserve is widely anticipated to increase its target interest rate by 75 basis points tomorrow (Wednesday, September 21). However, whether the bond market has adequately priced in this change remains uncertain until clearer insights on inflation trends emerge.

Wall Street is feeling a sense of tension ahead of another expected rate hike on Wednesday:

- The policy-sensitive 2-year Treasury yield is approaching 4%.

- Simultaneous rate hikes by central banks may lead to a series of financial crises, warns the World Bank.

- Arrests at the US southwestern border exceeded 2 million for the first time in a year.

- Mortgage rates have climbed to a new 14-year high, as reported here.

- Sweden’s central bank has increased its policy rate by 100 basis points in an effort to tackle surging inflation.

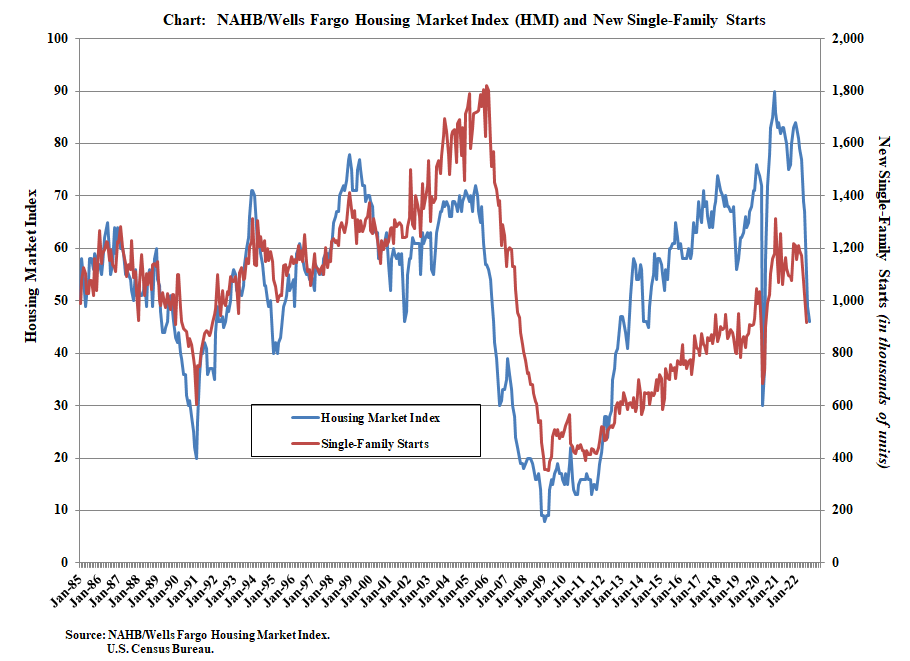

- The US Housing Market Index, which gauges homebuilder sentiment, declined again in September.