The current challenges in the housing market are largely attributed to soaring mortgage rates. For instance, the 30-year fixed mortgage rate is hovering around 7%, the highest it’s been in two decades. The significant question remains whether this crucial sector of the U.S. economy will outweigh the positive effects stemming from a still-strong labor market and robust consumer spending.

* British Prime Minister Liz Truss is under pressure to resign

* The Fed’s Beige Book indicates the U.S. economy expanded modestly since early September, but…

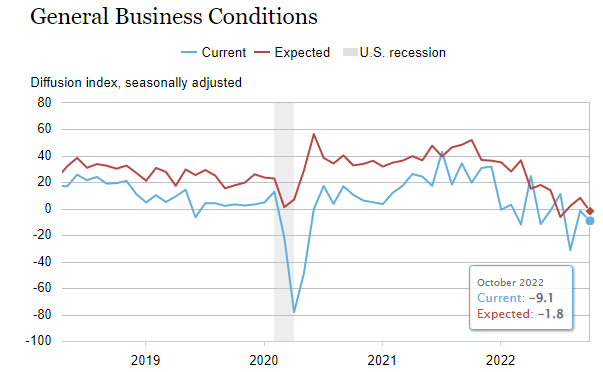

* A Fed survey reveals U.S. firms are increasingly pessimistic about economic conditions.

* The Japanese yen has reached its lowest level against the U.S. dollar since 1990.

* Procter & Gamble has seen earnings boosted by price hikes.

* Amazon’s founder, Jeff Bezos, forecasts troubles for the U.S. economy.

* Home sales dropped sharply in September, according to reports from Redfin.

* Mortgage applications in the U.S. have plummeted to a 25-year low for the week ending October 14.

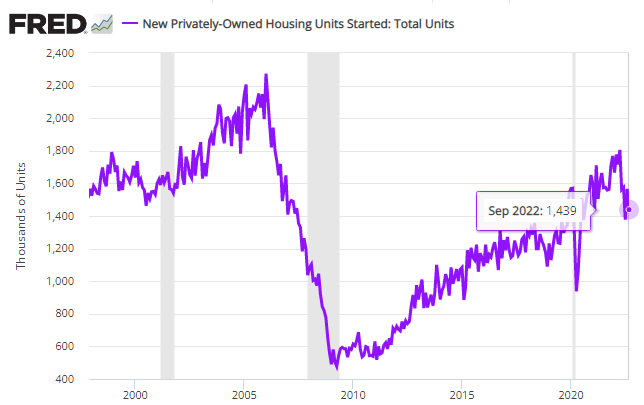

* U.S. housing starts fell more than anticipated in September:

Recent rebounds in the U.S. stock market have sparked speculation that equities may have found their bottom. While this is a possibility, the strength of ongoing downward momentum and various influencing factors could suggest otherwise.

* President Biden is expected to announce additional oil reserve sales to help lower gas prices.

* Central banks are predicted to continue raising interest rates to combat inflation, according to Nordea.

* Inflation in the UK increased by 10.1% in September, marking a 40-year high.

* Builder sentiment in the U.S. drops to a two-and-a-half-year low this October.

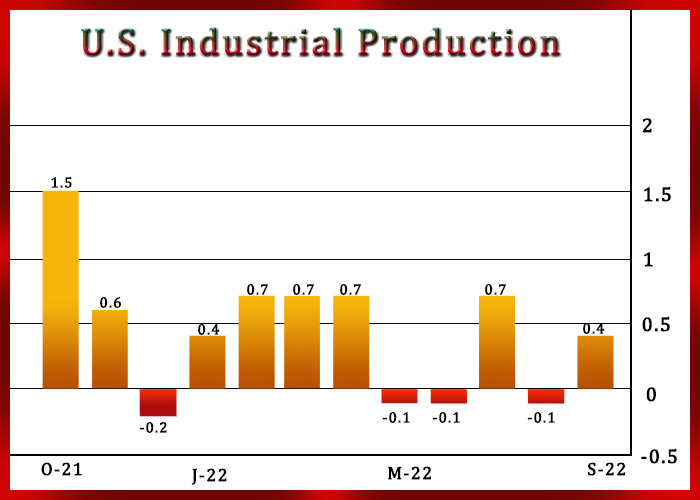

* U.S. industrial production surged beyond expectations in September:

The yield on U.S. 10-year Treasury bonds has experienced a significant surge over the past two months, driven by persistent inflation and consistent rate hikes by the Federal Reserve. However, the fair-value analysis from CapitalSpectator.com suggests that the potential for further increases in the 10-year yield may be limited, despite strong momentum that could push it higher in the near term.

* Russia continues its drone strikes against Ukraine, specifically targeting energy facilities.

* Europe is generating a record amount of wind and solar energy as its reliance on Russian gas diminishes, according to reports.

* China’s economic outlook has been downgraded as a result of Xi Jinping’s political agenda.

* The strong U.S. dollar is inflicting economic hardship globally.

* Bank of America’s strong earnings suggest a healthy U.S. consumer sector.

* Microsoft is implementing job cuts due to slowing revenue and sales growth.

* The oil market is closely monitoring a potential release from the Strategic Petroleum Reserve.

* The New York Fed Manufacturing Index has contracted for the third consecutive month in October:

In last week’s trading, the only major asset class that yielded a positive return through Friday, October 14, was U.S. government bonds designed to hedge against inflation, according to a selection of proxy ETFs.

* Russia has ramped up its drone strikes on Ukraine’s capital.

* China has postponed the release of crucial economic data.

* Expectations are that U.S. assets will lead a rebound once the bear market concludes, as a recent survey reveals.

* A strong U.S. dollar is aiding the recovery of small-cap stocks.

* Positive signs of easing congestion in supply chains have emerged after two years of disturbances.

* The British pound has made a comeback following new UK finance minister announcements regarding policy adjustments.

* The rapid rise in rental prices appears to be cooling in September.

* U.S. retail spending remained flat in September, coinciding with a surge in prices.

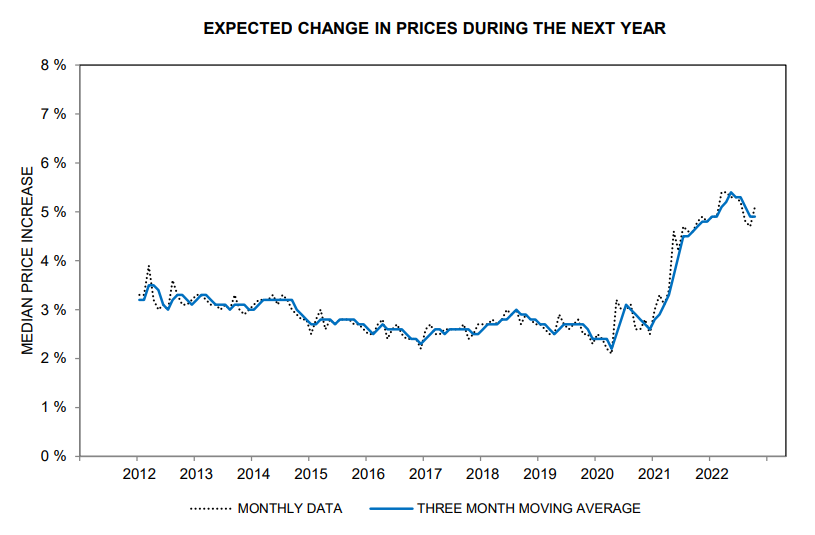

* Year-ahead inflation expectations among U.S. consumers have risen to 5.1% in October:

● Permanent Distortion: How the Financial Markets Abandoned the Real Economy Forever

Nomi Prins

Review via Jacobin.com

Nomi Prins discusses how the pandemic transformed the financial landscape, asserting that “too big to fail” has evolved into a situation where entities are “too big to correct.” As the world faced an unprecedented halt, central banks resorted to printing trillions to stabilize markets, leading to what may be the largest wealth transfer in history. From late 2019 to 2020, the net worth of the world’s billionaires surged by $1.9 trillion, a figure that has continued to grow. In December 2020, amidst around 2,500 daily COVID-related deaths in the U.S., the Dow Jones soared to a record 30,606.48. In contrast, poverty levels escalated from 9.3% in June 2020 to 11.7% by November, resulting in eight million more people falling below the poverty line. The latest report from the Congressional Budget Office reveals that the poorest half of the U.S. population now holds just 2% of the nation’s wealth.

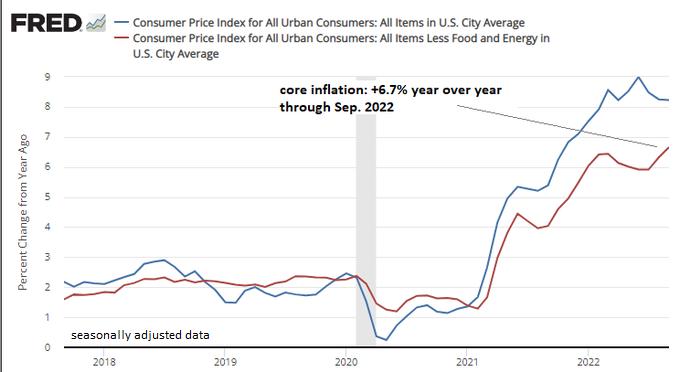

While it’s tempting to argue that inflation may have peaked, the evidence remains mixed. Depending on which indicators are analyzed, there are suggestions indicating that the worst is over, yet recent updates on consumer prices present a counterargument.

This collection of insights reveals the turbulent state of the current economic landscape, marked by fluctuating housing markets, rising interest rates, and varied inflation signals. As we navigate these complex challenges, understanding the nuances of economic indicators becomes crucial for making informed decisions.

Ultimately, the interplay between these factors will shape the future of the economy, emphasizing the importance of continuous monitoring and analysis.