The latest updates bring a mix of political and economic news from around the globe.

Here’s what you need to know:

- Democrats performed better than expected, but the balance of power in Congress remains uncertain.

- European leaders announced funding aimed at assisting poorer nations facing the challenges of climate change.

- In China, inflation showed signs of easing in October.

- China’s ‘Zero-Covid’ policy has become a game of speculation focused on President Xi.

- Some Wall Street investors are predicting that the Fed funds rate could rise to 6%.

- US inflation is expected to cool only slightly in the October report due this Thursday.

- Binance, the world’s largest cryptocurrency exchange, has agreed to acquire rival FTX.

- Meta is laying off more than 11,000 employees, which amounts to around 13% of its workforce.

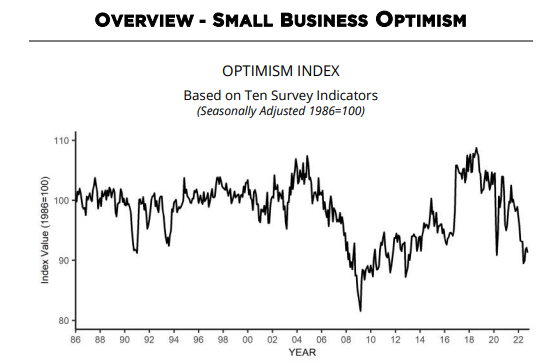

- US small business sentiment remains depressed in October.

Update: The analysis below clarifies that while summing two Treasury yields seems beneficial, it does not reflect an actual compounded yield. The intention is to use the combined yields as a timing indicator to identify favorable payout rates for a strategy involving a 50-50 mix of TIPS and conventional Treasuries. We apologize for any misunderstanding. –JP

The recent uptick in real yields for inflation-indexed Treasuries (TIPS) appears promising for securing attractive payout rates; however, the inherent risks associated with bonds remain significant. This context encourages the exploration of a somewhat unconventional strategy: holding both TIPS and standard Treasuries as a hedging approach.

* Florida’s east coast prepares for Tropical Storm Nicole.

* Republicans anticipate regaining power in Congress following today’s elections.

* At the COP27 climate summit, UN chief issues a stark warning for nations.

* China’s Covid restrictions continue to hamper the economy.

* The Covid pandemic remains a burden on the US workforce.

* Goldman Sachs suggests a soft landing for the US economy is still feasible.

* Consumer confidence in the housing market drops to a new low.

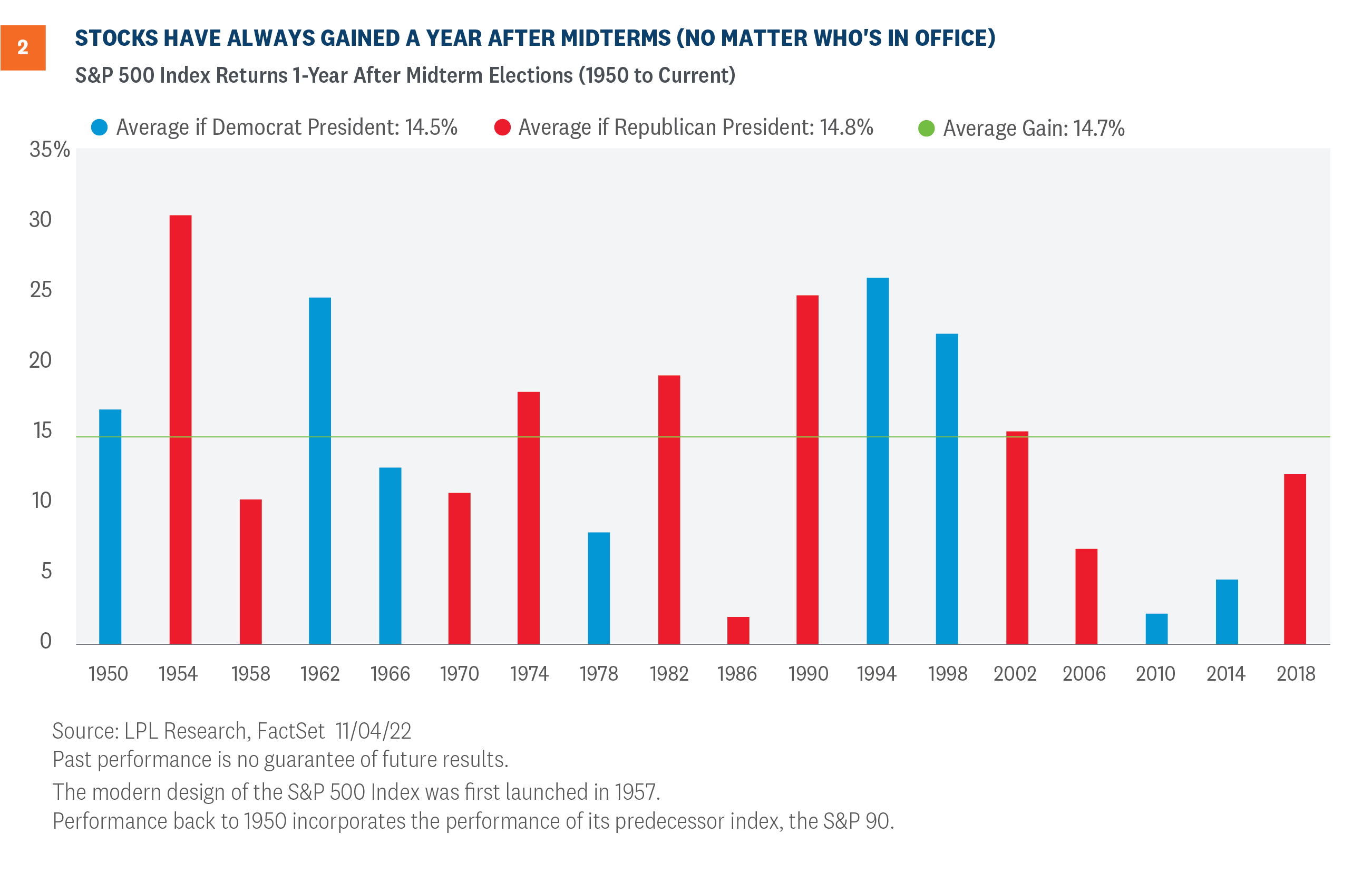

* According to LPL Research, US stocks “have peaked a year after midterms” since 1950:

The recent surge in global markets saw some fading last week, with commodities and foreign stocks showing gains, while US assets experienced a downturn, according to a set of ETF proxies.

The White House’s national security adviser has engaged in talks with senior aides to Russia.

* Republicans seem poised to regain control of the House and possibly the Senate in today’s election.

* Florida is preparing for a potential impact from Tropical Storm Nicole this week.

* China’s exports and imports saw an unexpected decline in October.

* Goldman Sachs forecasts that China is ‘months away’ from reopening.

* US oil production remains roughly stable amidst a slowdown in fracking activity.

* Apple’s iPhone shipments face delays due to lockdowns in China.

* Meta is reportedly preparing for significant layoffs.

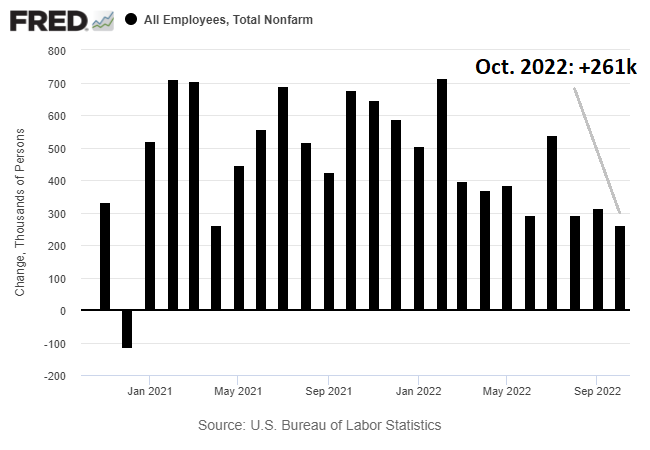

* The US experienced an increase of 261,000 payrolls in October, a solid growth rate but the slowest in 22 months:

● Global Discord: Values and Power in a Fractured World Order

Paul Tucker

Review from The Enlightened Economist

This book seeks to integrate the thoughts of David Hume with Bernard Williams to address the current tumultuous state of geopolitics and global challenges. Tucker uses Hume’s concepts of norms and incentives to reconsider international economic institutions, moving beyond conventional International Relations frameworks (like realism and constructivism). A central question addresses whether a legitimate international order can develop amidst the transition from the European/Atlantic order and the complexities of contemporary existential threats.

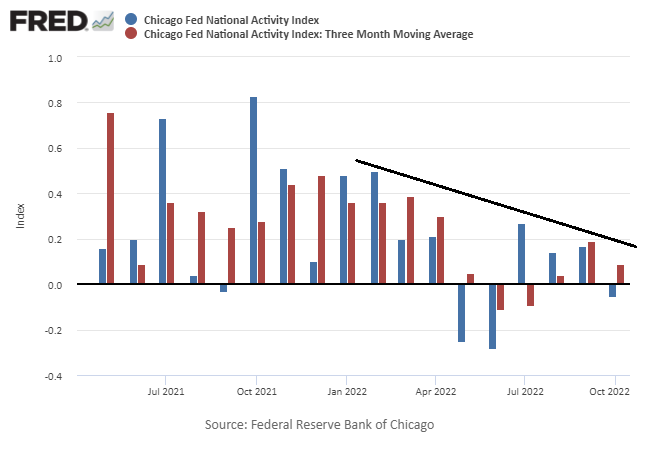

At the beginning of October, the short-term outlook for the US business cycle appeared somewhat dismal, predicting a slight downturn starting in November. However, just four weeks later, that pessimistic forecast has turned around, with economic activity anticipated to remain gently positive for the immediate future. While recession risks still exist, the current macro trend shows signs of strengthening.

* North Korea’s series of missile tests continues.

* Netanyahu is set to return as Israel’s prime minister.

* German Chancellor Olaf Scholz, during his visit to China, advocates for equal economic ties.

* US holiday sales are predicted to increase by 6% to 8%, according to industry forecasts.

* US factory orders registered a moderate increase in September.

* US jobless claims remain low, indicating a tight labor market.

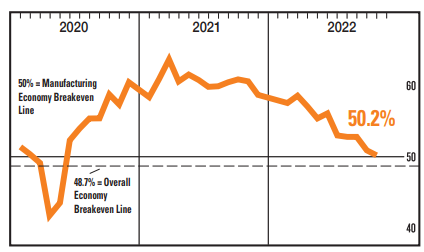

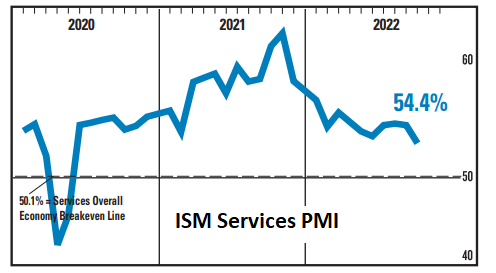

* Contraction in the US services sector deepens in October per PMI survey.

* US services sector growth slowed to its lowest level in 2.5 years in October:

Investors and analysts are concentrating on three crucial questions regarding monetary policy: When will the Federal Reserve slow its rate increases? When will it pause these rate hikes? And when might it begin to cut rates? In his recent press conference, Powell gave somewhat optimistic hints regarding one of these queries.

* North Korea launched an ICBM that allegedly failed mid-flight, according to South Korean military reports.

* The Fed increased the target rate by 75 basis points and indicated that more hikes may be coming.

* Wells Fargo’s mortgage division is bracing for layoffs as lending activities decline.

* Economic activity in China continues to decline, showing signs of widespread slowdown in October.

* Global manufacturing output fell again in October.

* The services sector remains a bright spot within the US labor market as of October.

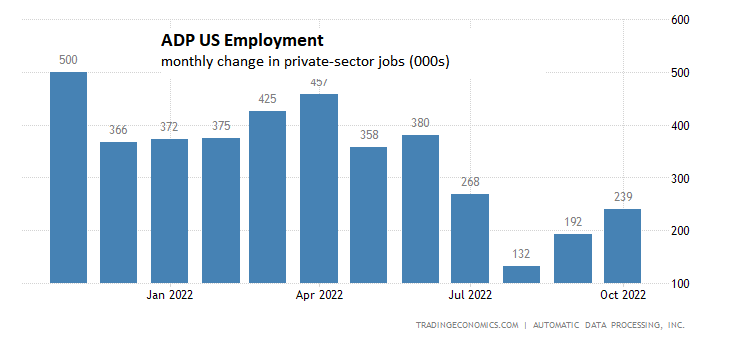

* US companies increased hiring in October, marking a three-month high: