The recent passing of former Federal Reserve Chairman Alan Greenspan at the age of 100 has prompted a reevaluation of his legacy. While many are familiar with the so-called “Greenspan put,” there are other, less widely discussed aspects of his tenure that merit examination. Here, we explore some overlooked elements of Greenspan’s career, particularly in light of skepticism from within the financial community during his time in office.

A finance professional who frequently attended Economics Club of New York talks recounted an experience: “On a shuttle flight from Washington DC to New York, Alan Greenspan was on board. I found myself contemplating whether I would be willing to perish in a crash if it meant Greenspan would too. I quickly decided, ‘yes.’”

This anecdote illustrates that even during his peak, many skeptics hesitated to voice dissent against the media’s enthusiastic support for Greenspan.

President Reagan appointed Greenspan to replace Paul Volcker, who had implemented neoliberal monetary policies and aimed to weaken labor’s bargaining power through sky-high interest rates to combat inflation of the 1970s and early 1980s. In his book, The Secrets of the Temple, author Bill Greider noted that Volcker tracked construction wages, hoping to see them decline as proof that his policies were effective. Volcker famously stated, “I want unions to get the message.”

While Volcker had a reputation for being tough on labor, he was also stringent with major financial institutions. He believed that banks should maintain a simple structure, focused on their essential role in processing payments, seeing overly complex financial practices as rent-seeking behavior. He remarked that the only true innovation he observed in banking was the introduction of the ATM.1

Volcker’s tenure ended due to his resistance to bank deregulation. In a 2020 paper by Thomas Ferguson, Paul Jorgensen, and Jie Chen, the authors detail the tension surrounding his ousting:

The announcement on June 2, 1987, that President Reagan would nominate Alan Greenspan to replace Paul Volcker stunned the financial markets, which expected Volcker’s reappointment. Bonds suffered one of their largest losses on record, and the dollar plunged.

Officially, it was reported that Volcker had expressed a desire not to be reappointed after eight years in the position. However, many believed that the truth was more nuanced. Volcker would have likely accepted another term had the President himself encouraged it, but no such effort was made.

Furthermore, many economists anticipated that Greenspan would largely continue Volcker’s policies. Contrary to this belief, insiders revealed a starkly different reality. During a significant meeting among Republican leaders regarding Volcker’s future, Treasury Secretary James Baker and Deputy Richard Darman displayed overt hostility toward the towering, cigar-smoking Fed Chair. Despite attempts by Senate leaders, including Robert Dole and Pete Domenici, to advocate for Volcker’s reappointment based on his expertise, Baker dismissed these concerns, asserting that he and Darman were prepared to address any G7 issues.

Baker openly cited two primary reasons behind his opposition: Volcker’s skepticism toward financial deregulation and his firm stance against repealing the Glass-Steagall Act—the New Deal legislation designed to separate investment banking from commercial banking. Baker chillingly noted that abolishing Glass-Steagall would shift the political power dynamics between the two major parties, depriving Democrats of vital funding sourced primarily from investment bankers, led by Robert Rubin of Goldman Sachs.

While it’s true that Glass-Steagall remained intact until 1999,2 by then the act was already significantly weakened, making its repeal a mere formality. This shift was highlighted by the 1988 merger of Credit Suisse with First Boston, following the 1987 market crash—precisely during Greenspan’s early term. Likewise, during the late 1980s and throughout the 1990s, firms like Citibank and JP Morgan aggressively pursued ambitious strategies in investment banking, with the Fed facilitating various financial affiliations.

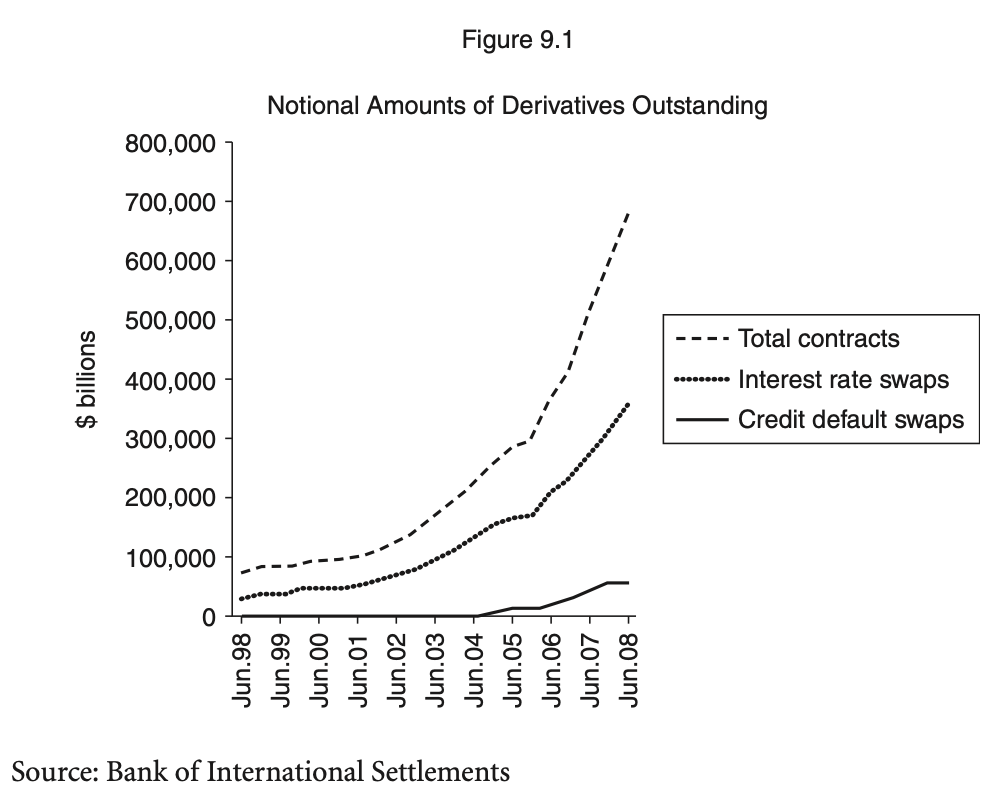

A more insidious aspect of Greenspan’s legacy was his endorsement of unregulated derivatives trading, which contributed majorly to the 2008 financial crisis. Contrary to common perceptions, the crisis wasn’t solely a housing market failure; rather, it stemmed from a derivatives catastrophe linked to risky subprime assets. The market for subprime loans was too small to trigger a systemic crisis independently, but the interplay of credit default swaps (CDS) and collateralized debt obligations (CDOs), heavily reliant on subprime exposures, amplified risks to the global financial system.

Greenspan’s negligence in managing systemic risks long preceded the infamous confrontation between him and Treasury Secretary Bob Rubin against CFTC chair Brooksley Born over the regulation of CDS. He actively promoted the expansion of derivatives, which were primarily used for speculation, diverting both resources and talent into unproductive financial activities. This misguided approach contributed to an insatiable demand for securitized products in the markets.

In the early 1990s, I worked with O’Connor & Associates, a leading derivatives trading firm, and witnessed first-hand the high level of expertise necessary to manage derivatives effectively. I was alarmed when I read in Institutional Investor in 1996 that Greenspan advocated a “Let a thousand flowers bloom” philosophy regarding derivatives regulation, effectively endorsing a hands-off approach.

Regulators, under this framework, operated almost blindly, akin to a doctor relying solely on blood pressure readings to gauge patient health. The failure of Value-at-Risk (VaR) models during the crisis starkly illustrated the dangers of such oversight.

My examination of these issues is not intended to be exhaustive, but rather to highlight how Greenspan’s deregulatory approach to derivatives was a critical factor contributing to the 2008 crisis, leading to the proliferation of rated AAA securities that ultimately caused widespread financial devastation. As illustrated in ECONNED:

Some experts argue that the surge in demand for repos was largely attributed to hedge fund borrowing, while others linked it directly to growth in derivatives. Because hedge funds also serve as major counterparties in derivatives, these two factors are interconnected. Demand for collateral for derivatives often leads brokers and traders to accept lower-quality assets, contributing to further instability in the financial system.

It’s crucial to note that many structured credit products weathered the crisis seemingly unscathed, while subprime mortgage-backed securities had long been troubled. The issues were not with asset-backed securities in general but arose from inappropriate asset selection for securitization and excessive leverage. As the saying goes, leverage upon leverage creates a ticking time bomb—this principle not only applies to modern markets but recalls the catastrophic crash of 1929.

While one could continue delving into this complex narrative, such extensive focus on Greenspan risks granting him more dignity than he deserves. In summary, his legacy is intertwined with critical lessons about the potential pitfalls of deregulated financial markets, the consequences of seeking complexity over simplicity, and the role of regulators in maintaining financial stability.

____

1 After the crisis, Bank of England governor Mervyn King advocated for reforms known as ring-fencing, aimed at reinstituting the separation of investment banking to impose stricter regulations on traditional banks. Ultimately, King and his allies were unable to prevail against Treasury interests.

2 I have unique insight into this matter. During my tenure at McKinsey beginning in 1983, I focused primarily on assisting commercial banks in transitioning into investment banking. I vividly recall an incident when a Citibank manager proudly described how they had maneuvered a commercial company on and off their books, a blatant violation of regulations at the time.

3 It’s essential to highlight how Greenspan downplayed the Federal Reserve’s role as a regulatory supervisor, despite insisting upon maintaining that authority when the Gramm–Leach–Bliley Act was finalized.