* President Biden promises retaliation following a deadly attack on US forces in Jordan

* Iran denies involvement in the assault that resulted in the deaths of 3 US soldiers in Jordan

* This week’s Federal Reserve policy meeting might offer hints regarding a potential rate cut in March

* Increasing real interest rates amidst a decline in inflation present a fresh challenge for the Fed

* Decreasing inflation and steady growth provide the US economy with an advantage over the global market

* Corporate and consumer borrowing in the US is on the rise

* Evergrande, China’s major property developer, has been ordered to liquidate its assets

* China has approved more than 40 AI models for public use over the last six months

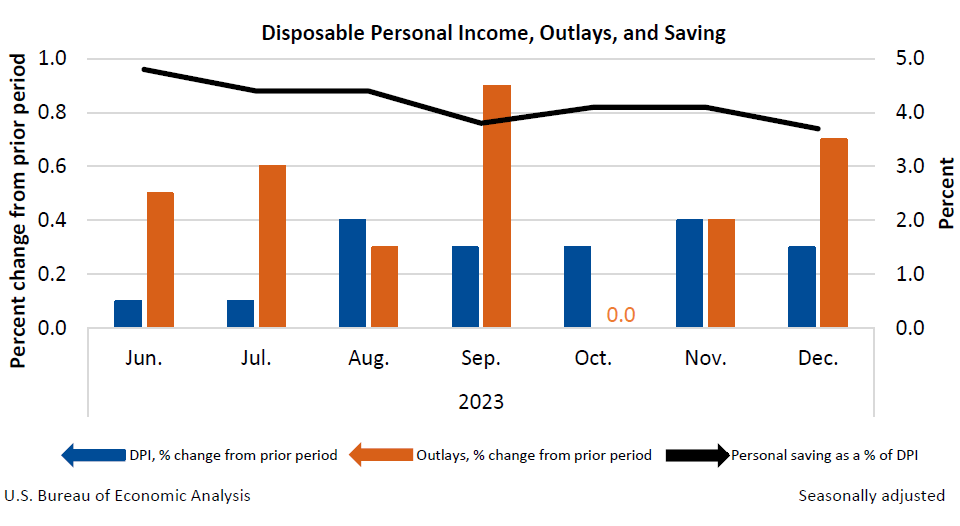

* US consumer spending surged in December:

● Busting the Bankers’ Club: Finance for the Rest of Us

● Busting the Bankers’ Club: Finance for the Rest of Us

Gerald Epstein

Review via Kirkus Reviews

This book by an economics professor examines the many failures of the financial system that adversely affect average consumers while benefiting the wealthy. Epstein emphasizes that while “Finance is a vital and productive component of our economic system, it can also lead to stagnation, instability, inequality, and crises.” The inequities within the system became glaring during the 2007-2008 financial crisis, which burdened taxpayers with costs between $50,000 and $120,000 per household—not counting the impact on the wealthiest households.

The most unexpected aspect of yesterday’s fourth-quarter economic report was the robust level of growth observed. In contrast, positive trends had been apparent for weeks, if not longer, assuming a comprehensive analysis of various indicators while steering clear of common pitfalls in recession probability assessments.

* US jobless claims increased last week but still remain low. However…

* Jobless claims may be an unreliable measure of labor market conditions

* New home sales in the US rose more than anticipated in December

* The Chicago Fed National Activity Index indicates softer growth in December

* The Japanese stock market is approaching record highs last seen in 1989

* US durable goods orders were steady in December after a surge in November

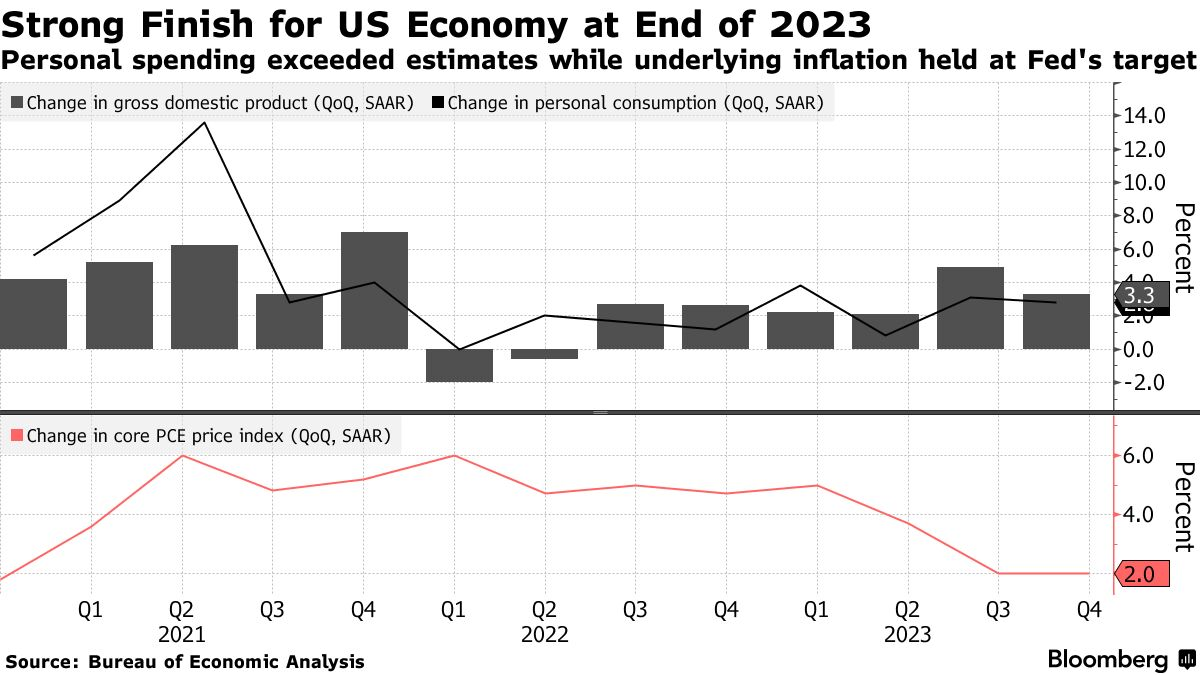

* US GDP growth in Q4 exceeded expectations by a significant margin:

Could 2024 signal the resurgence of the momentum factor in investment performance? After a dwindling impact in 2023, signs suggest a potential rebound for this segment of equity risk premium, as indicated by a collection of proxy ETFs through the closing on January 24.

* The Fed faces potential political backlash in relation to its 2024 policy decisions

* The ongoing Middle East crisis is having an economic impact on Europe

* Eurozone business activity continues to contract for the eighth consecutive month in January according to PMI data

* Revenue is surging for the vital semiconductor company ASML

* Tesla is projecting a significant sales decline this year

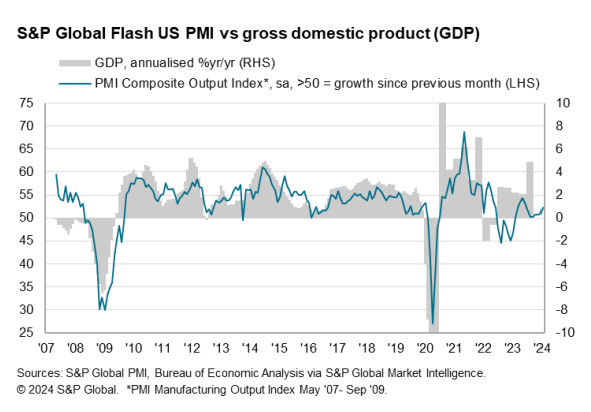

* US business activity saw an uptick in January as reflected in PMI survey data:

The Bureau of Economic Analysis is expected to announce tomorrow (January 25) that US output slowed considerably in the fourth quarter following an exceptionally strong gain in Q3. However, Thursday’s GDP report is also anticipated to reveal moderate growth during the final three months of 2023—a development that aligns with the ‘soft landing’ narrative embraced by some economists.

* Trump looks poised to be the GOP nominee after winning the New Hampshire primary

* The Eurozone economy continues to contract in January according to PMI data

* The Chinese central bank has announced policy measures to stimulate economic growth

* Economic repercussions are spreading from turmoil in the Red Sea region

* The upcoming US Q4 GDP report on Thursday may confirm the presence of a ‘soft landing’ in the economy

* Climate economics are now of concern in many sectors

* The S&P 500 edged higher on Tuesday, achieving yet another record high:

The resilience demonstrated by the US economy throughout 2023 caught many economists off guard. From the beginning of the year to the early weeks of the third quarter, a plethora of recession warnings filled the airwaves. While a closer examination of the data suggested a different narrative, these high-risk alerts captured attention and flourished, often extending beyond their expiration date.

* Polls indicate Trump is likely to become the GOP nominee following today’s New Hampshire primary

* Goldman’s head of trading still anticipates four interest rate cuts by the Fed in 2024

* China is considering a stock market rescue package to mitigate declining prices

* Japan’s Nikkei index reached a 34-year high on Monday

* India’s stock market capitalization has now surpassed Hong Kong’s for the first time, making it the world’s fourth largest

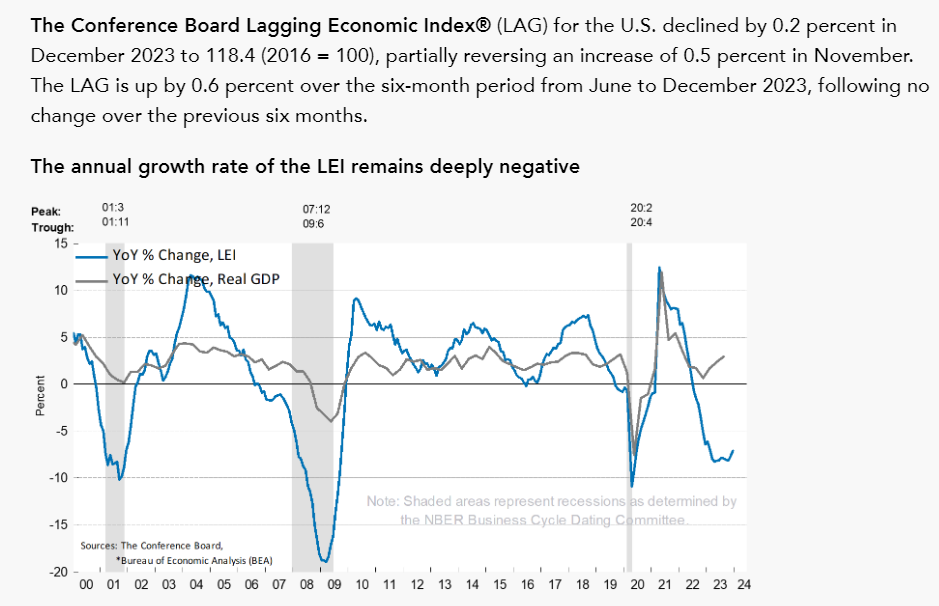

* The US Leading Economic Index still suggests a recession despite the growing economy: