Recently, several key economic updates have emerged that could influence future market trends:

- * The Federal Reserve has maintained interest rates; Powell indicates a potential rate cut in September is ‘on the table.’

- * Wage growth in the US continues to decline, hitting a four-year low in the second quarter.

- * Pending home sales in the US have increased significantly in June.

- * The Chicago PMI has dipped further into contraction territory this July.

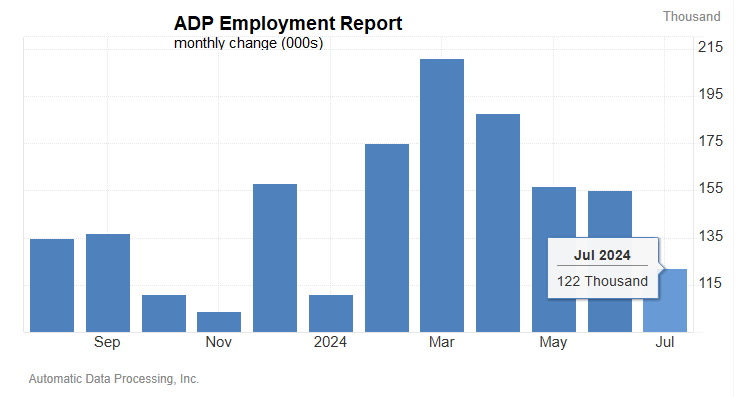

- * Private employment growth in the US has slowed to its lowest pace since January.

So far this year, US fixed income returns have generally been positive, particularly leading up to the Federal Reserve’s policy announcement scheduled for today. Although it is widely anticipated that the central bank will keep rates steady, many in the market are betting on a rate cut in September, anticipating that the Fed will take this action.

Key developments include:

- * A Hamas leader has been killed in Iran, following a suspected Israeli strike, potentially escalating tensions.

- * Japan has increased interest rates as part of a shift away from its long-term easy monetary policy.

- * The Fed is expected to leave rates unchanged today.

- * Consumer confidence in the US remains lukewarm for July.

- * Home prices in the US have reached a new record high, according to the Case-Shiller Home Price Index.

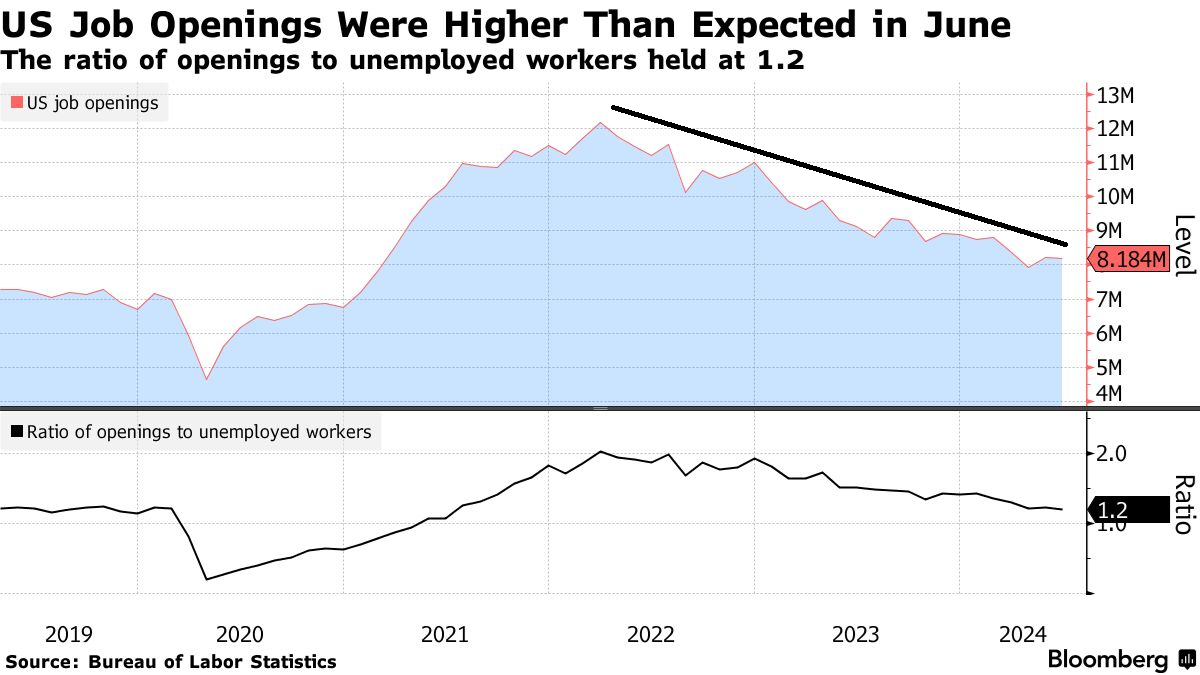

- * Job openings in the US declined in June, indicating a continued downward trend.

Market analysts are increasingly convinced that the Federal Reserve will initiate interest rate cuts during the upcoming policy meeting on September 18. While tomorrow’s announcement could introduce some uncertainty, market sentiment leans strongly towards this expectation.

Key indicators this week include:

- * The prolonged inversion of the US Treasury yield curve shows signs of potentially ending.

- * Eurozone growth remains sluggish during the second quarter.

- * Senator Lummis proposed legislation for the US Treasury to acquire a bitcoin reserve worth $69 billion.

- * Advances in AI are enhancing the precision and speed of weather forecasts.

- * Texas’s manufacturing sector has remained stable in July amid weakening demand.

- * Even with expected rate cuts, long-term bonds still carry associated risks.

US equities faced challenges, experiencing declines for two consecutive weeks through July 26, as reflected in the S&P 500 Index. This marks the first series of back-to-back weekly decreases since April. Currently, the potential for further downturns remains uncertain. However, it is evident that US stocks continue to outperform other global markets this year, as indicated by various ETFs tracking major asset classes.

Recent articles reflect important trends and economic factors:

- * A review examines whether the Fed has waited too long to implement rate cuts.

- * US manufacturers are reassessing their hiring strategies.

- * Foreclosures in the commercial property sector are increasing.

- * An analysis of potential risks to the booming AI sector can be found here.

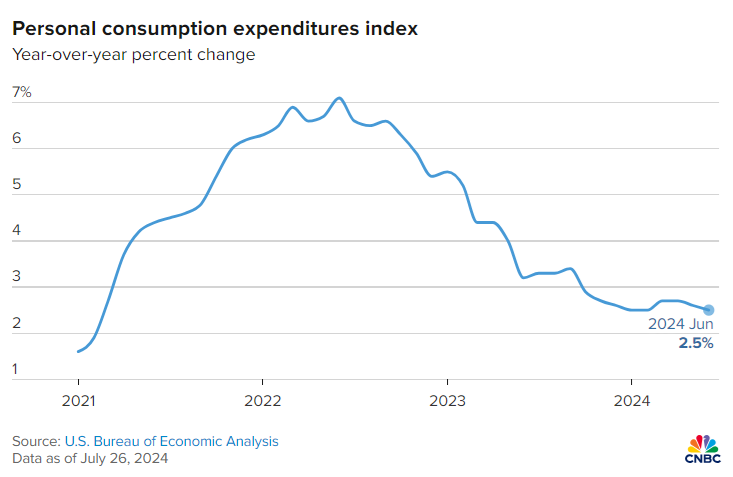

- * PCE inflation dropped to 2.5% in June compared to last year:

● The Fragility of China: Breaking Points of an Invincible Regime

● The Fragility of China: Breaking Points of an Invincible Regime

Dennis Unkovic

Summary via publisher (Encounter Books)

President Xi Jinping of China is convinced that his nation is destined to surpass the United States as the leading military and economic power. Every strategy Xi has implemented since taking office in 2013 is designed towards achieving this goal. Although almost four decades of rapid economic growth have misled many in the West into viewing contemporary China as an unassailable power, deeper examination reveals that it is, in fact, more vulnerable than it seems. In the book, author Dennis Unkovic introduces the concept of MaxTrends®, identifying key factors that could undermine Xi’s ambitions. Among these include significant demographic changes, breakdowns in global supply chains, an intensifying arms race, and the Taiwan dilemma, all suggesting that China’s perceived strength may be more of an illusion.

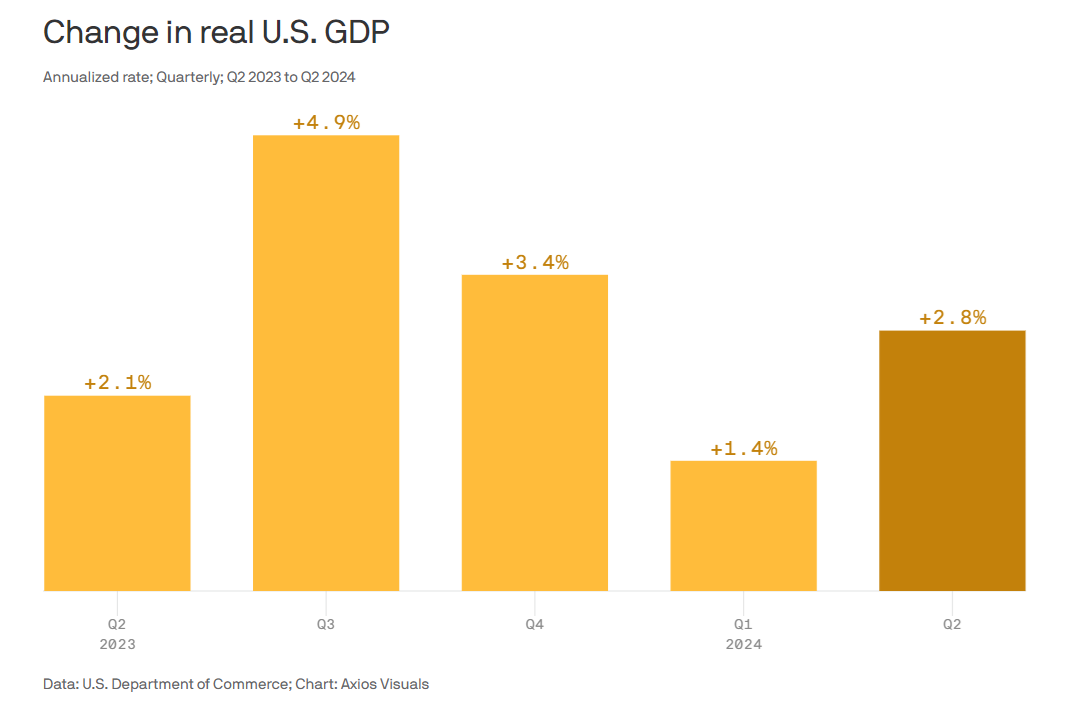

With the prospect of a recession, some analysts are now looking to the third quarter as the earliest possibility for an economic downturn in the US. Recent reports indicate that the chances of the second quarter marking the beginning of a contraction have diminished, especially after the GDP rose unexpectedly during the April to June timeline.

As the market reacts to various pressures, analysts predict potential risks for big tech if the US economy slows down. Key updates this week highlight:

- * Bank of America analysts are warning that a cooling economy could jeopardize the recent big-tech rally, they say.

- * US credit card delinquency rates have risen to their highest level in twelve years.

- * Durable goods orders have seen a surprising decline in June.

- * Apple has dropped out of the top five smartphone vendors in China.

- * Jobless claims in the US decreased last week while remaining within a relatively low range.

- * Economic growth improved more than anticipated in the second quarter: