On his first day in office, President Trump has announced that he is contemplating implementing tariffs on both Canada and Mexico as early as February: “We’re considering a 25% (tariff) on Mexico and Canada…” The trade imbalance the US has with Canada is primarily due to American oil purchases. Mexico also maintains a trade surplus with the US and, during the first eleven months of 2024, was the leading exporter to the largest economy in the world.

Donald Trump will be inaugurated as the 47th president of the United States at noon Eastern Time. Upon taking the oath of office for the second time, it will be evident that he is returning to the White House with an economy that is significantly healthier than when he departed four years ago.

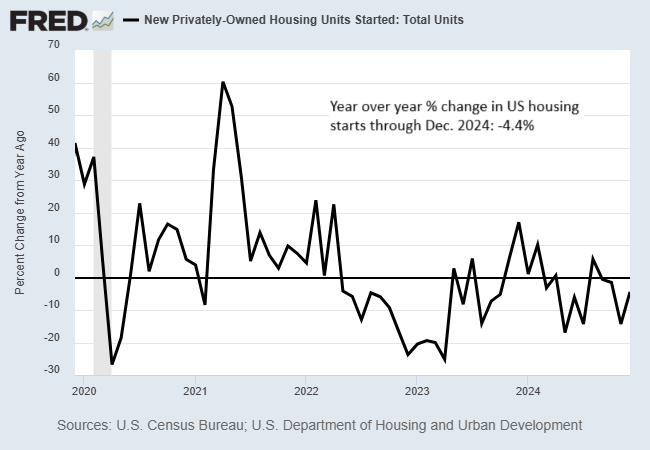

US housing starts saw an increase for a second consecutive month in December, reaching the highest annual rate since February. “Home builders concluded 2024 with impressive growth after several months of subdued construction activity,” stated Nationwide Economist Daniel Vielhaber. However, the year-over-year trend remains weak. Despite the latest increase, starts fell 4.4% compared to the same month last year.

● The Data Economy: Tools and Applications

● The Data Economy: Tools and Applications

Isaac Baley and Laura L. Veldkamp

Summary via publisher (Princeton U. Press)

The world’s most valuable companies derive their worth largely from their data assets. Giants like Amazon, Apple, and Google illustrate the competitive edge enhanced by substantial data collections. Despite this growing importance, contemporary economic theory often underplays the role of data. In this work, Baley and Veldkamp leverage a variety of theoretical frameworks from the cutting edge of macroeconomics and finance to model and assess data-driven economies. By establishing that data represents digitized information that aids in predictions and minimizes uncertainty, the authors reveal how decisions regarding data at the firm level resonate throughout the larger macroeconomic and financial arenas.

An Investigation into the Causes of Stock Market Return Deviations from Real Earnings Yields

Austin Murphy (Oakland University), et al.

December 2024

This study reveals that the disparity between the current earnings yields of the S&P 500 and the long-term real TIPS yield has significant predictive capabilities for excess returns on that stock market index, both in the short term and over longer investment periods. For all intervals, deviations from the theoretical standard for the equity premium align positively with existing economic slack. At annual intervals, these excess stock return deviations correlate negatively (positively) with recent inflation rates (money growth). Inflation appears positively (negatively) related to future monetary policy tightening (long-term real profit growth).

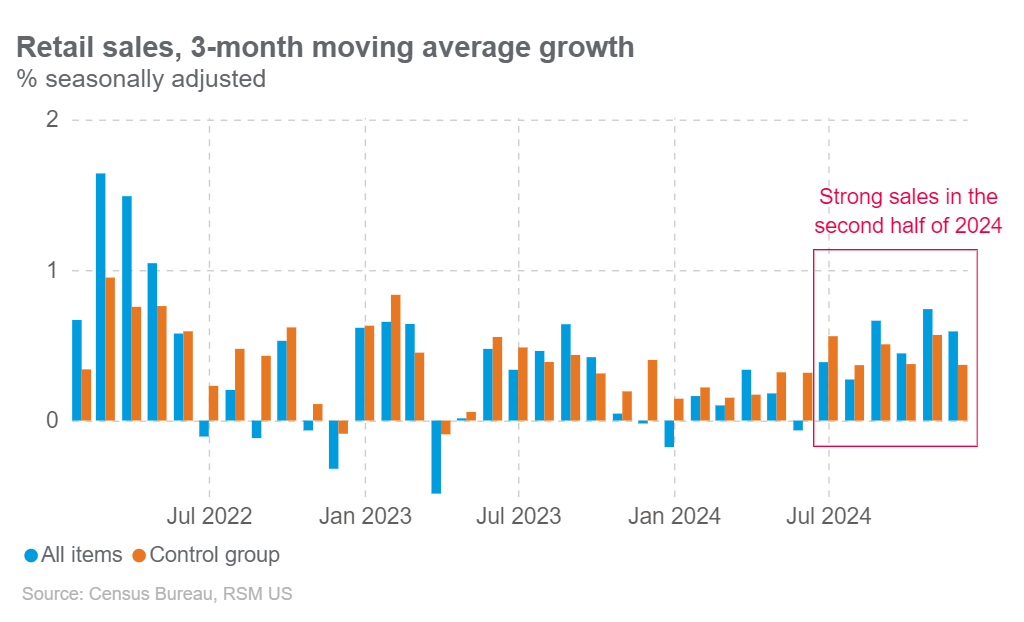

US retail sales increased for a fourth consecutive month in December, posting a lower-than-anticipated rise of 0.4% compared to the month prior. The Commerce Department also revised November’s figures upward to an impressive 0.8% monthly gain. “The control group, which contributes to GDP calculations, surpassed expectations with a 0.7% increase for the month,” writes an analyst at RSM. “This growth raised the group’s three-month annualized average to 5.4%, just shy of the 5.9% recorded in the third quarter.”

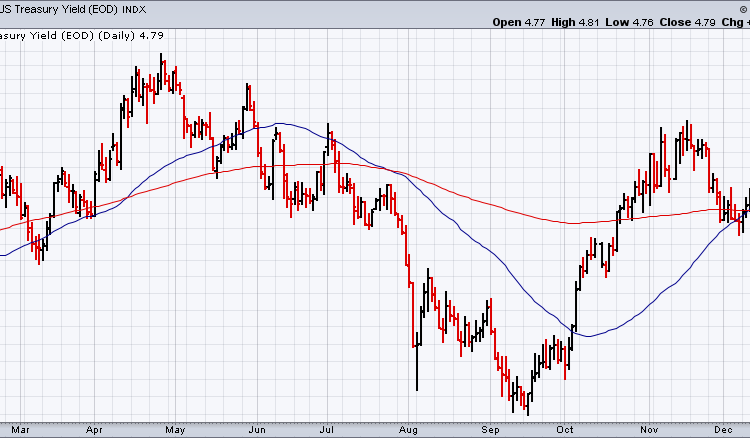

The market premium for the US 10-year Treasury yield softened in December after two consecutive months of increases. This assessment utilizes a “fair value” calculation provided by CapitalSpectator.com. Despite the recent dip, the market continues to value the 10-year yield at a significantly higher rate compared to pre-pandemic levels.

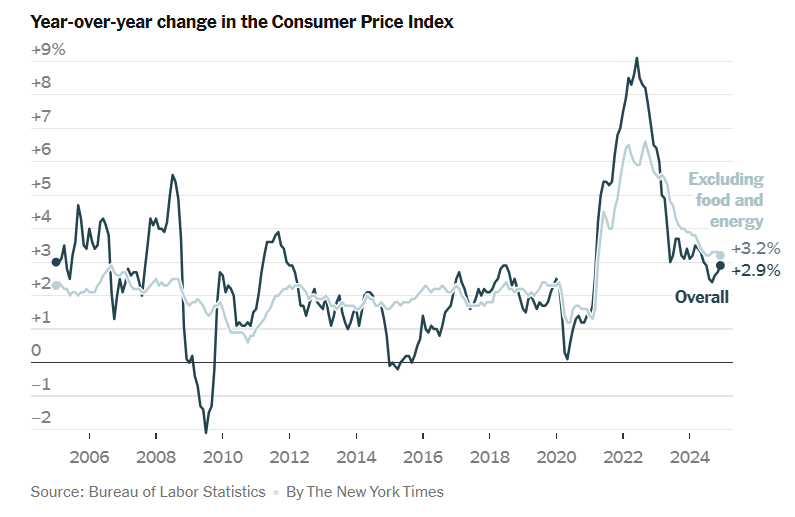

US consumer inflation accelerated in December, increasing by 2.9% compared to the previous year. This rise marks the third consecutive month in which the consumer price index at the headline level has gained. The current rate represents the highest since July. In contrast, the core CPI rate dipped to 3.2%, maintaining a consistent range above 3% that has been observed lately. “When we take a broader view of inflation, we see that progress is slow,” said Sarah House, senior economist at Wells Fargo. “While some advancements have been made, the pace is quite disappointing.”

As January progresses, the financial landscape appears to be challenging for most major asset classes, except for one: commodities. Utilizing a diverse array of ETF proxies, a comprehensive measure of commodities is showing a remarkable year-to-date increase. In stark contrast, the remainder of the markets are predominantly declining, with only one sector remaining flat as of trading on January 14.

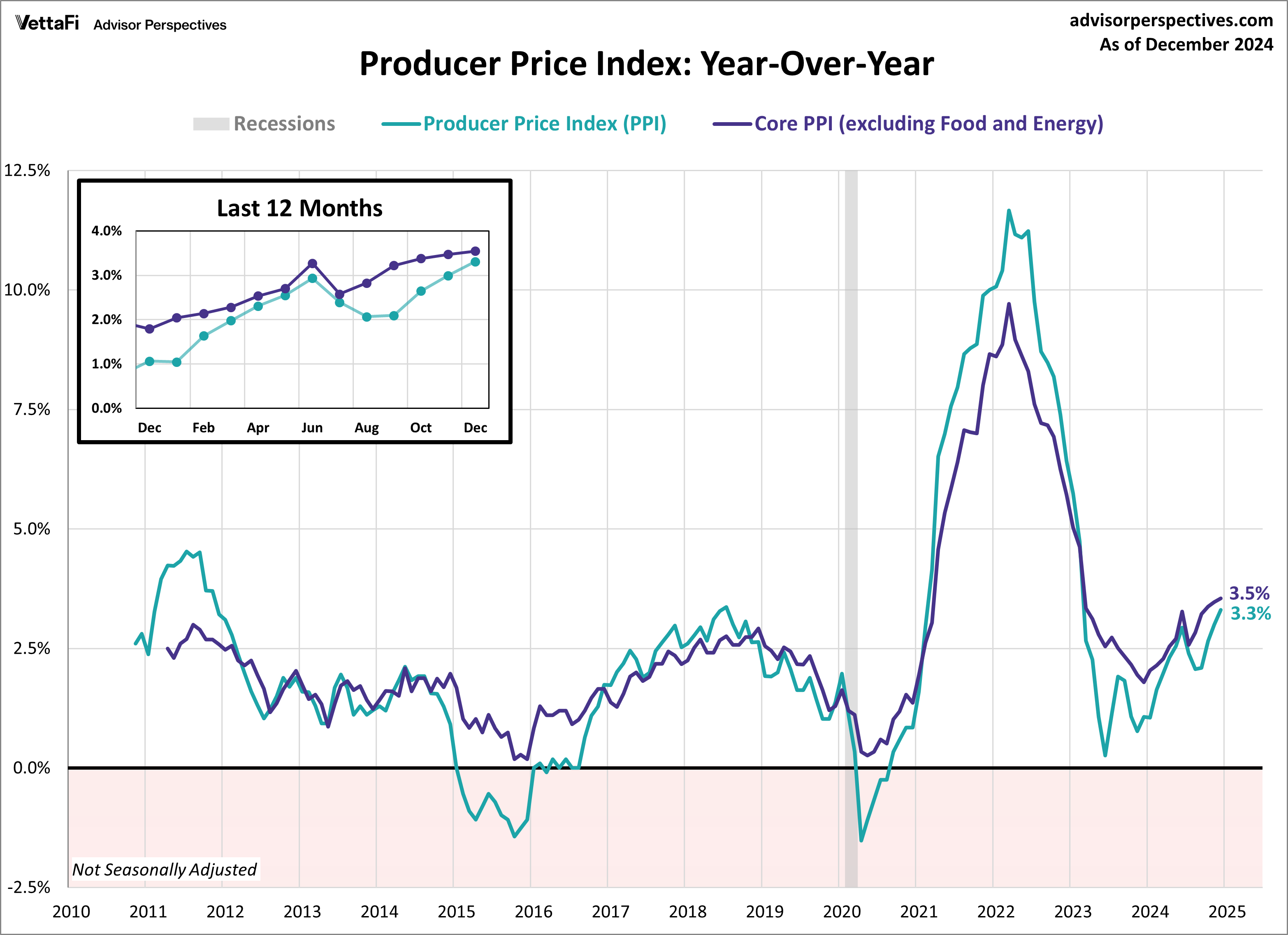

US producer price inflation rose to a year-over-year level of 3.3% as of December. Although this figure falls short of expectations, it represents the fastest increase since February 2023. “While the current figures are better than anticipated, they may not align with what the Federal Reserve desires in terms of easing monetary conditions in a rapidly growing economy, especially considering the incoming administration’s agenda of tariffs and tax cuts,” noted Carl Weinberg, chief US economist at High Frequency Economics.

This revised structure maintains the original HTML formatting while improving the readability and flow of the content. The added introductions and conclusions offer context and coherence for the discussion presented in the article.