The Unintended Consequences of Rebalancing

Campbell R. Harvey (Duke University), et al.

January 2025

Institutional investors regularly engage in portfolio rebalancing with significant cumulative value, often guided by predetermined schedules or deviations from target allocations. Our study reveals that such rebalancing actions influence market behavior and generate distinguishable price trends. When stocks become overweight, funds typically sell equities and purchase bonds, resulting in a decrease in equity returns of approximately 17 basis points the following day. This finding remains consistent even after controlling for momentum, reversals, and macroeconomic factors. Alarmingly, we estimate that current rebalancing methods cost investors roughly $16 billion each year, equating to about $200 per U.S. household. Furthermore, the predictability of these transactions allows certain market participants to capitalize on the orders from large institutional funds. While rebalancing is an essential practice for investors, our findings underscore the costs tied to conventional strategies and highlight the necessity for new methods to alleviate these losses.

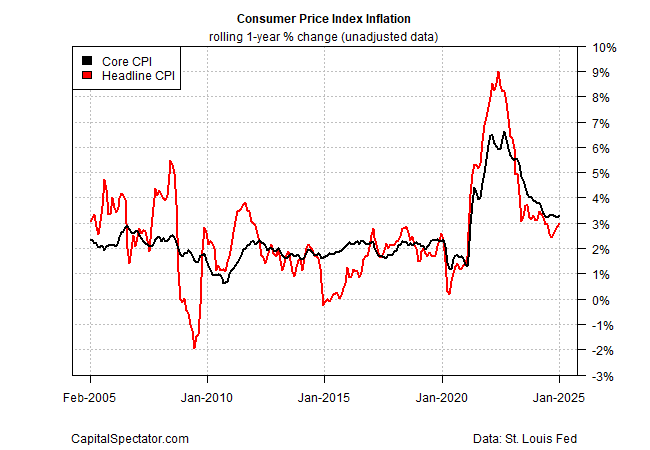

A notable increase in US producer prices during January aligns with consumer price trends indicating a potential rise in inflation. The producer price index rose by 3.5% over the year ending in January, matching December’s figures and hinting at a moderately quicker increase compared to recent trends.

The market premium on the US 10-year Treasury yield surged significantly in January, reaching its highest level in nine months, as reflected in a “fair value” assessment from CapitalSpectator.com. The hotter-than-anticipated inflation readings from the previous month indicate that this market premium may remain elevated longer than initially predicted.

US headline consumer inflation continues to rise, showing a 3.0% increase in January compared to the same month last year, marking the highest rate since last June. “The ongoing struggle with inflation isn’t over for consumers, businesses, or investors,” writes Chris Rupkey, Chief Economist at FwdBonds, in a research note released Wednesday. “There might be seasonal factors causing prices to spike in January, but the news is concerning for Federal Reserve officials.” ClearBridge Investments’ investment strategy analyst, Josh Jamner, observes: “The Federal Reserve’s ‘wait and see’ approach will extend longer than anticipated following January’s scorching CPI inflation report. This data solidifies our belief that the cycle of rate cuts has concluded.”

This year, yields on a range of global assets have trended upward. This shift reflects various anxieties, such as persistent inflation risks and increasing uncertainty regarding global trade dynamics. Investors are demanding a higher yield premium, as suggested by various ETFs that track the primary asset categories.

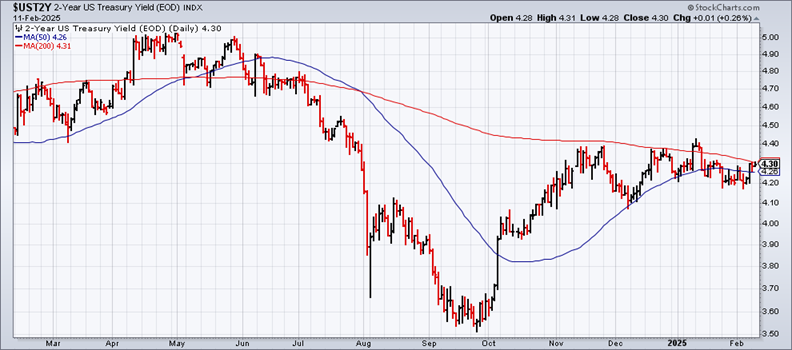

Federal Reserve Chairman Jerome Powell asserted that the central bank does not “need to be in a hurry” to reduce interest rates. While testifying before the Senate, he stated: “With our current policy stance being significantly less restrictive than it previously was, coupled with the robust state of the economy, we are not in haste to modify our policy.” Meanwhile, the 2-year US Treasury yield, sensitive to policy changes, inched up recently but remains within a moderate range compared to historical data.

Following two consecutive years of remarkable performance, U.S. stocks are currently experiencing lackluster results on the global front. While all major stock markets are recording gains thus far in 2025, there is a notable divergence, with U.S. stocks raising less compared to some foreign markets, based on a series of ETFs as of the close on February 10.

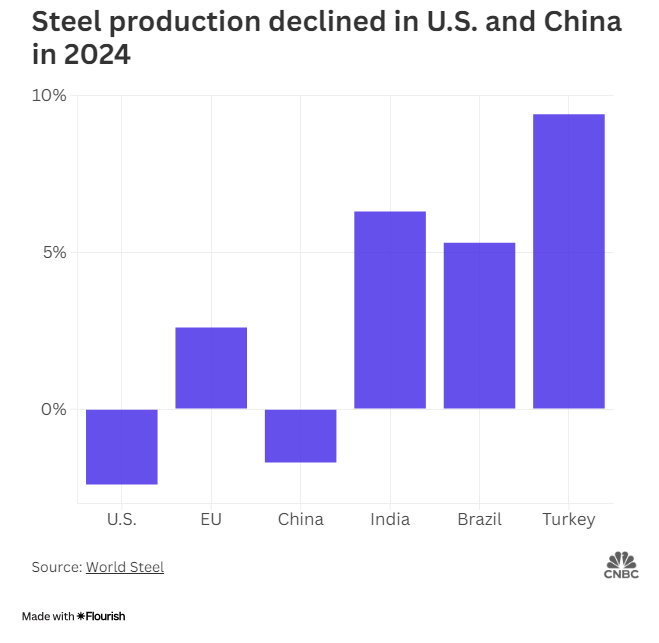

Trump has announced a 25% tariff on all steel and aluminum imports. As the world’s largest importer of steel, the U.S. sources these metals chiefly from Canada, Brazil, and Mexico. These materials are essential for various sectors, including transportation, construction, and packaging. The new tariffs will take effect on March 4.

Recently, Morningstar has reported that tactical asset allocation funds have “failed—again.” While this sounds alarming for this investment strategy, a deeper look indicates that it may be premature to abandon the notion that dynamically adjusting asset allocations has failed. As discussed below, the argument in favor of tactical asset allocation (TAA) remains compelling, provided investors are knowledgeable and willing to discern valuable strategies from ineffective ones.

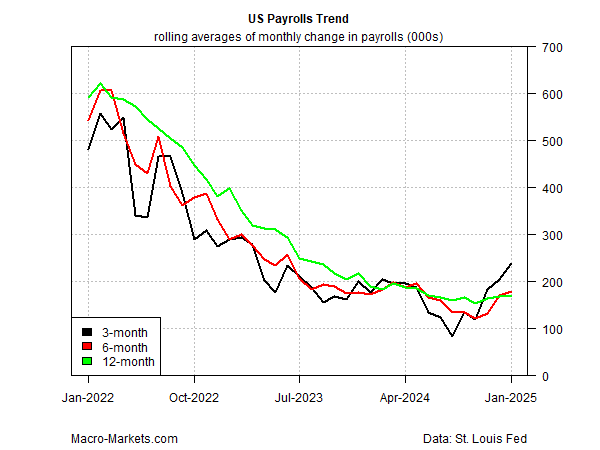

US non-farm payrolls increased by 143,000 in January, representing a significant slowdown from the robust growth observed in December. Concurrently, the unemployment rate dropped to 4.0% last month, the lowest level since May. “The diminished payroll growth in January obscures a potentially stabilizing trend in hiring,” states a report from TMC Research, a division of The Milwaukee Co. “A three-month rolling average of payrolls, which helps mitigate short-term fluctuations, suggests that the hiring trend is strengthening. Notably, the six-month trend has surpassed the one-year change in January for the first time since May.”