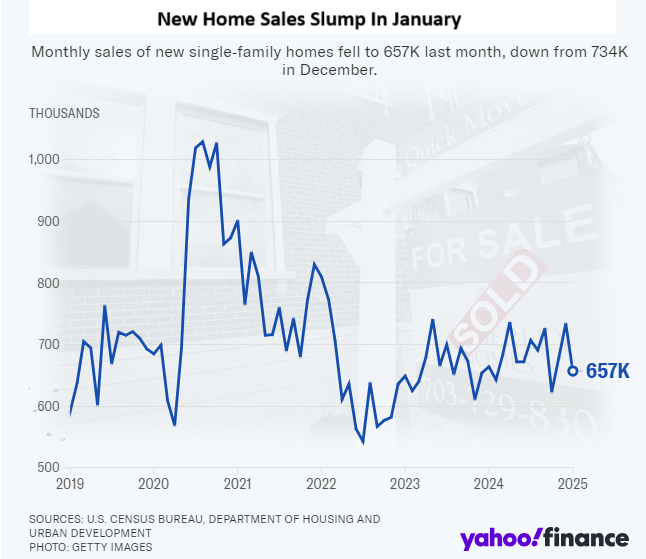

New US home sales declined significantly in January. CoreLogic’s chief economist Selma Hepp noted, “New home sales will continue to face challenges, as fewer homes are being listed due to weak buyer interest. While homebuilders are providing incentives for buyers, elevated mortgage rates and ongoing price increases limit the number of potential homebuyers to those with higher incomes.”

Recent news reports seem to have unsettled investor confidence. However, it’s premature to make sweeping conclusions based on just a few days of disappointing survey results. More critically, the most recent data suggests that the economy continues to expand, businesses are still hiring, and the short-term outlook for consumer spending remains optimistic. Nevertheless, the White House should reflect on the recent decline in public sentiment. Financial markets appear to be doing just that.

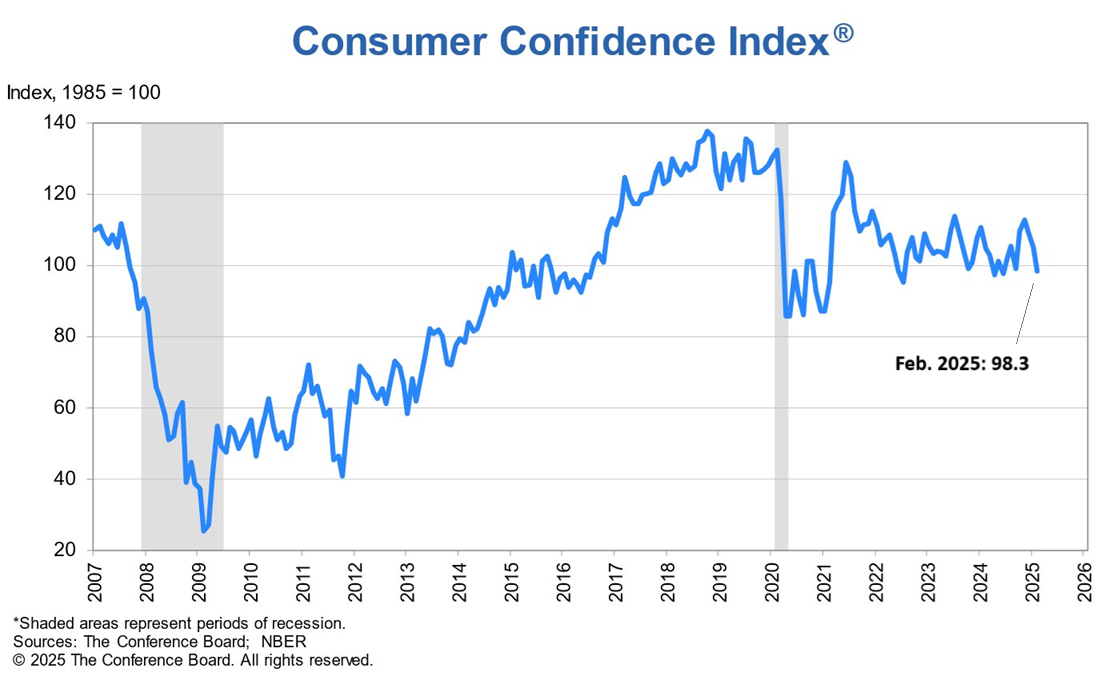

The US Consumer Confidence Index declined sharply in February, marking the largest monthly drop since 2021. Stephanie Guichard, a senior economist at The Conference Board, stated, “This marks the third consecutive month of decline, placing the Index at the lowest level seen since 2022.” Additionally, average inflation expectations over the next twelve months jumped from 5.2% to 6% in February.

The central bank’s task is perpetually challenging, and current circumstances render it particularly complex.

In addition to the usual hurdles that complicate real-time monetary policy decisions, the Federal Reserve must also consider the potential economic effects of a multitude of directives from the White House. The impact of President Trump’s plans on the Fed’s expectations remains uncertain, but economists in the private sector are assessing the broader implications.

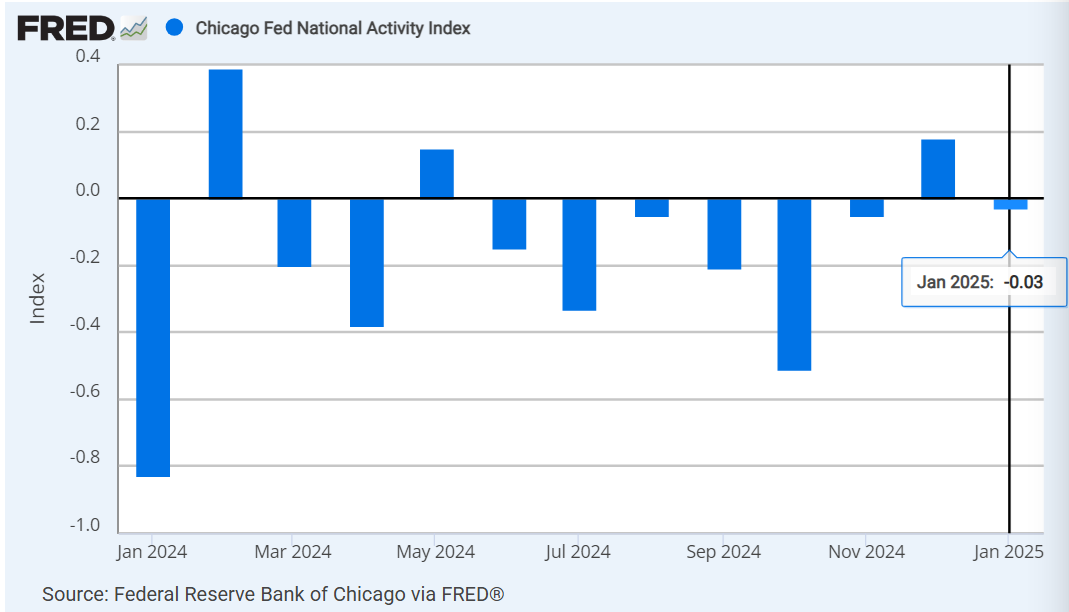

According to the Chicago Fed National Activity Index, US economic activity slowed in January. Two of the index’s four major categories experienced a decrease compared to December, with one category contributing negatively in January.

This year is proving to be markedly different from 2024 regarding the performance of various major asset classes. Global equities outside the US are leading the way, alongside a wide array of commodities, as evidenced by a range of ETFs up to Friday’s close. In contrast, the once-dominant US equities market is showing rather modest results thus far.

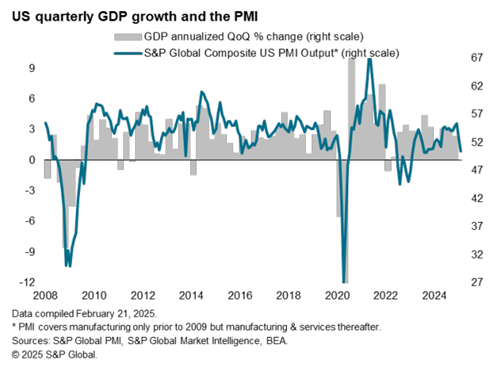

US economic activity has “stalled and payrolls are declining in February, as optimism diminishes and costs rise,” according to the latest update of the US PMI Composite Output Index, a survey-based GDP indicator. The initial estimate for the index this month is 50.4, hitting a 17-month low, only slightly above the neutral 50-point threshold that delineates growth from contraction.

● Why Nothing Works: Who Killed Progress―and How to Bring It Back

● Why Nothing Works: Who Killed Progress―and How to Bring It Back

Marc J. Dunkelman

Interview with author via NPR

Q: When New York City built its subway system in the early 1900s, the first subway line through Manhattan took about three years to complete. Today, anything of that scale in the United States is virtually impossible to accomplish in three years. What are your thoughts on this comparison?

A: I believe that comparison is spot on. There was a time in our history where centralized power was granted to specific figures to make significant decisions that were intended for the common good. Although these decisions were not always beneficial and sometimes became abusive, we began to realize this during the 1960s and 70s.

Amid growing uncertainty regarding inflation, the relatively elevated real yields available in inflation-indexed Treasuries provide a partial remedy of certainty for cautious investors.

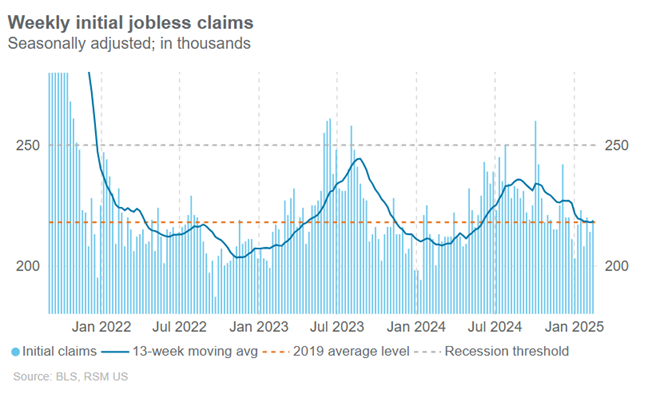

The number of US jobless claims rose slightly last week, but remains at levels consistent with the pre-pandemic period. An analyst from RSM noted, “New claims have been on a downward trend since last August, with the 13-week moving average reaching 218,000 after a peak of 235,000, indicating that the labor market remains resilient.”