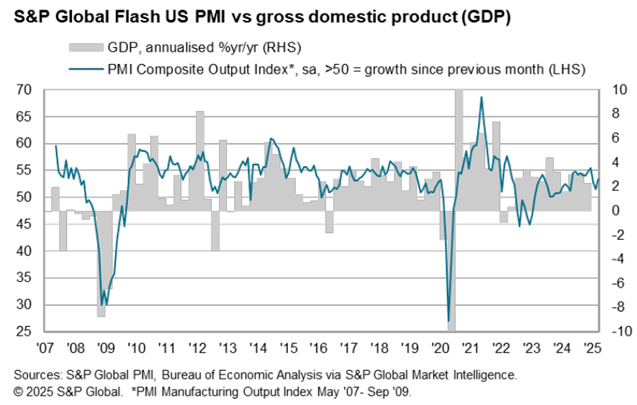

In March, US business activity saw a notable upswing, reaching a three-month peak, as reported by the US PMI Composite Output Index, which serves as a survey-based proxy for GDP. This growth surge was primarily driven by the services sector, despite a downturn in manufacturing activity. The chief business economist at S&P Global Market Intelligence noted, “The rebound in service sector activity in March signals a stronger economic trajectory as we wrap up the first quarter.” However, he cautioned that the data suggests an annualized growth rate of just 1.9% for March, and only 1.5% for the entire quarter, indicating a gradual decline in GDP growth as we move away from the peak levels of 2024.

2025 has proven somewhat challenging for the US stock market, however, year-to-date returns for energy and healthcare stocks depict a different narrative. Based on a range of ETFs up to Friday’s close (March 21), both sectors have achieved significant gains, standing out as bright spots in an overall lukewarm market.

The US Treasury yield curve has inverted once more, as evidenced by the spread between the 10-year and 3-month treasuries, registering a minor negative shift of -0.03. Historically, an inverted yield curve is often seen as an indicator of increased recession risk in the near term. However, it’s important to note that this signal isn’t infallible; the inversions in 1998 and mid-2022 did not precipitate economic downturns. More recently, the curve inverted in both 2022 and 2023 without leading to a recession.

● King Dollar: The Past and Future of the World’s Dominant Currency

● King Dollar: The Past and Future of the World’s Dominant Currency

Paul Blustein

Review via Financial Times

Dollar hegemony has long been a point of frustration for governments globally. In the 1960s, the French criticized America’s “exorbitant privilege.” Fast forward forty years to the global financial crisis, and China began advocating for a move away from the dollar. Blustein argues that despite these challenges, the forces supporting the dollar are remarkably sturdy while alternatives remain weak, rendering its dominance “nearly impregnable.” Even if the dollar’s importance declines, he suggests that the emergence of multiple international currencies could enhance financial stability, as it would offer diverse safe havens for investors during crises.

ChatGPT and Deepseek: Can They Predict the Stock Market and Macroeconomy?

Jian Chen (Xiamen University), et al.

February 2025

This study investigates whether ChatGPT and DeepSeek can successfully analyze information from the Wall Street Journal to forecast stock market trends and the macroeconomy. The findings indicate that ChatGPT possesses notable predictive capabilities. In contrast, DeepSeek doesn’t perform as well, likely due to its less extensive training in English compared to ChatGPT. Other large language models showed similar limitations. Notably, the prediction accuracy stems from investors’ tendency to be slow to react to positive news during economic downturns and uncertainty. While negative information does correlate with market returns, it lacks predictive strength. Current evidence suggests that ChatGPT is the only model effectively capturing economic news relevant to market risk premiums.

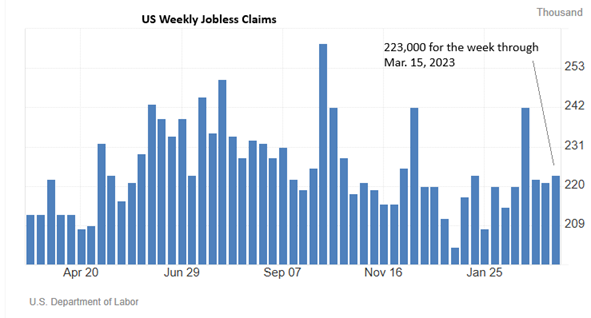

US jobless claims increased slightly last week, yet they remain low, indicating a generally positive outlook for the labor market. Last week, claims rose by 2,000, reaching a seasonally adjusted level of 223,000, which is moderate compared to recent historical figures.

So far this year, investing outside of US stocks has proven a successful strategy. Analysis using ETF proxies indicates that American equities remain the sole asset class showing negative returns year-to-date, as of trading through March 19.

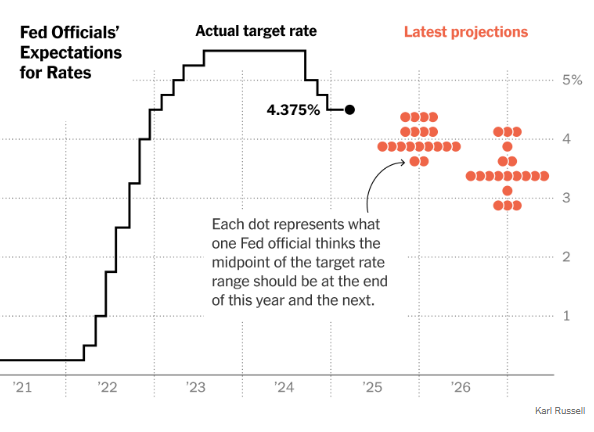

The Federal Reserve maintained its target interest rate and adjusted its 2025 inflation forecast upward while lowering growth expectations. Despite the rise in inflation projections, most Fed officials still anticipate potential interest rate cuts later this year. In a recent press conference, Chairman Powell stated, “Inflation has started to rise again, attributed partly to tariffs, and we may see a delay in further progress throughout this year.”

The escalation of macroeconomic uncertainty associated with tariffs, along with the looming threat of a global trade war, has complicated the Federal Reserve’s daunting task of adjusting interest rates amidst unpredictable future economic conditions. Additionally, evolving White House policies could significantly influence future inflation and economic performance, creating a challenging landscape for the Fed’s rate-setting strategy.

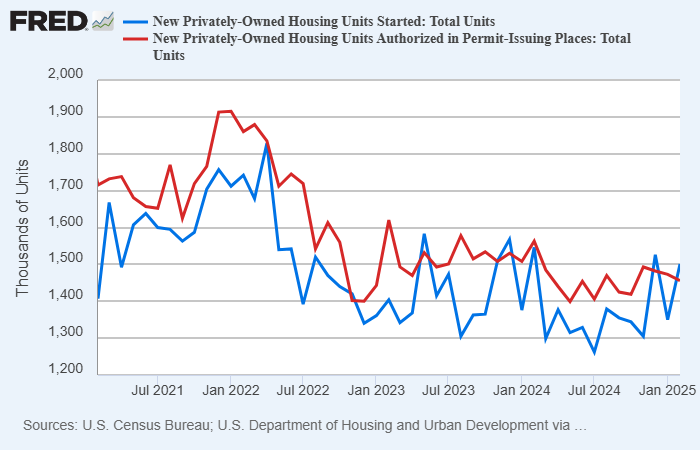

US housing starts increased in February, yet newly issued building permits — a leading indicator for residential construction — have decreased for the second consecutive month, dropping 6.8% compared to last year. “February’s recovery from January’s sharp decline, attributed to unusually harsh temperatures, was balanced by a fall in housing permits, dampening overall enthusiasm. The uncertainty induced by impending tariffs is hampering construction activities,” Bloomberg Economics remarks.