Shifts in uncertainty can be challenging to quantify, yet they become more apparent during significant events. Currently, we find ourselves in one such period. A key indicator is the US stock market, which is now requiring a higher risk premium due to increased uncertainty—evidenced by falling prices. This situation effectively signals a greater expected return for future time horizons.

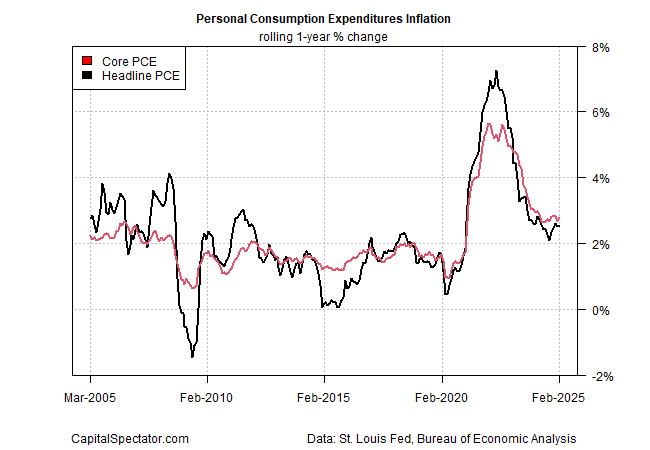

Core inflation in the US remained “sticky” in February, as indicated by the core PCE index, which the Federal Reserve closely monitors. The core PCE registered a year-over-year increase of 2.8%, significantly above the Fed’s 2.0% inflation target. “The Fed appears to be adopting a ‘wait-and-see’ approach, with additional waiting ahead,” explained Ellen Zentner, chief economic strategist at Morgan Stanley Wealth Management. “While the latest inflation data was higher than expected, it is not extreme enough to hasten the Fed’s timeline for interest rate cuts, particularly given the prevailing uncertainty concerning tariffs.”

● The Behavioral Portfolio: Managing Portfolios and Investor Behavior in a Complex Economy

● The Behavioral Portfolio: Managing Portfolios and Investor Behavior in a Complex Economy

Phillip Toews

Summary via publisher (Harriman House)

The investment advisory industry is facing two significant challenges that often go unaddressed. First, the historical risks associated with both stock and bond portfolios surpass what most investors and advisory practices can sustain. Secondly, the typical methods advisors employ to discuss portfolios do little to mitigate investors’ inherent biases and poor decision-making tendencies. In “The Behavioral Portfolio,” Phillip Toews provides a roadmap for constructing robust portfolios that cater to optimistic investing while concurrently addressing the challenges posed by a heavily indebted environment. He begins by redefining foundational portfolio objectives, such as market gains, minimizing extreme loss risks, and safeguarding against high inflation. Following this foundation, he elucidates the process of quantifying and assembling these portfolios, demonstrating that advisors can enhance their clients’ chances of success through this careful strategy.

Economic growth is anticipated to experience a significant pullback in next month’s official GDP report for the first quarter, according to the median nowcast compiled by various sources at CapitalSpectator.com. While recession conditions are likely to be averted for the time being, the first quarter’s data suggests heightened vulnerability as we proceed into the second quarter and beyond.

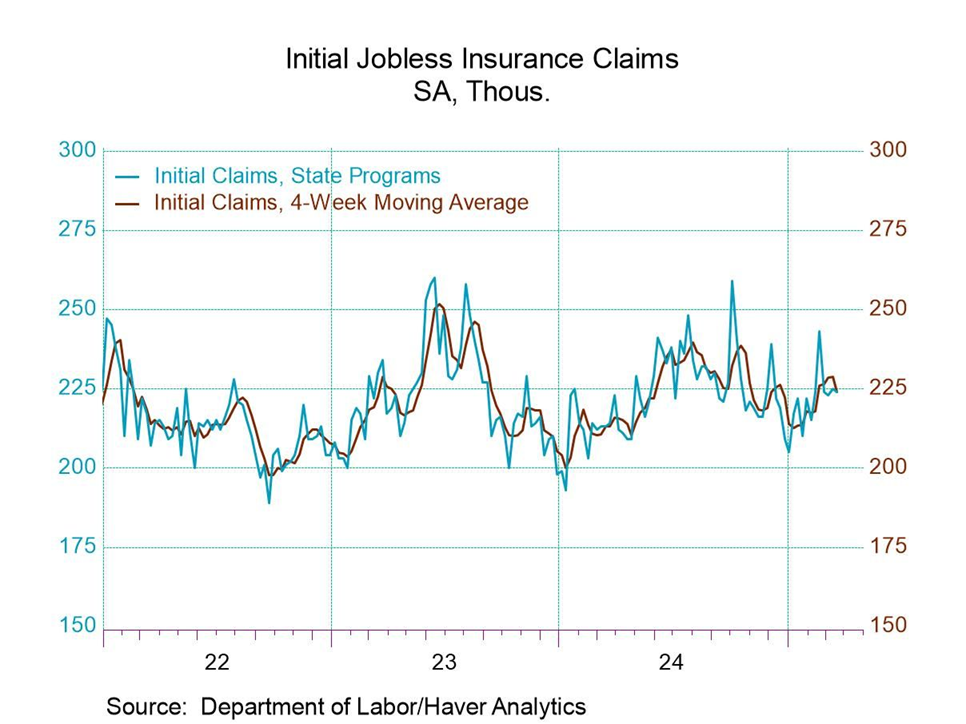

The number of US jobless claims declined last week, maintaining a moderate level relative to recent trends. Initial unemployment claims decreased to 224,000, seasonally adjusted—a low figure in the historical context, indicating ongoing stability or even growth in the labor market.

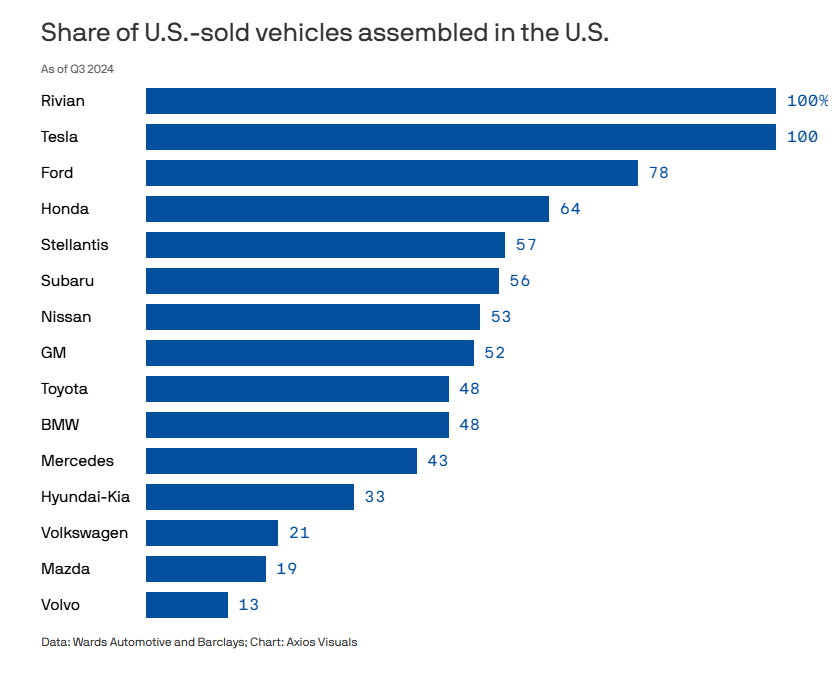

President Trump’s recent announcement regarding tariffs serves as a stark reminder that macroeconomic uncertainty remains high and is likely to persist in the near future. “We’re going to implement a 25% tariff on all vehicles not produced in the US,” he stated on Wednesday. While not entirely unexpected given the President’s inclination toward tariffs, it underscores the administration’s commitment to its policies, suggesting a challenging landscape for those relying on typical economic and financial market strategies.

Trump’s announcement regarding a 25% tariff on imported vehicles is expected to increase car prices in the US. “We anticipate significantly higher vehicle prices,” commented economist Mary Lovely, a senior fellow at the Peterson Institute for International Economics. About 45% of vehicles sold in the US are imported, with the majority coming from Mexico and Canada. Automakers most at risk include Volvo, Mazda, and Volkswagen, which reportedly have the lowest proportion of their vehicles produced domestically, according to research from Wards Automotive and Barclays.

The US stock market has faced challenges this year; however, the low-volatility equity risk premium has been performing impressively, surpassing overall stocks significantly through the close on March 25. This notable rise in the risk premium in 2025 stands in stark contrast to the modest decline exhibited by the market overall.

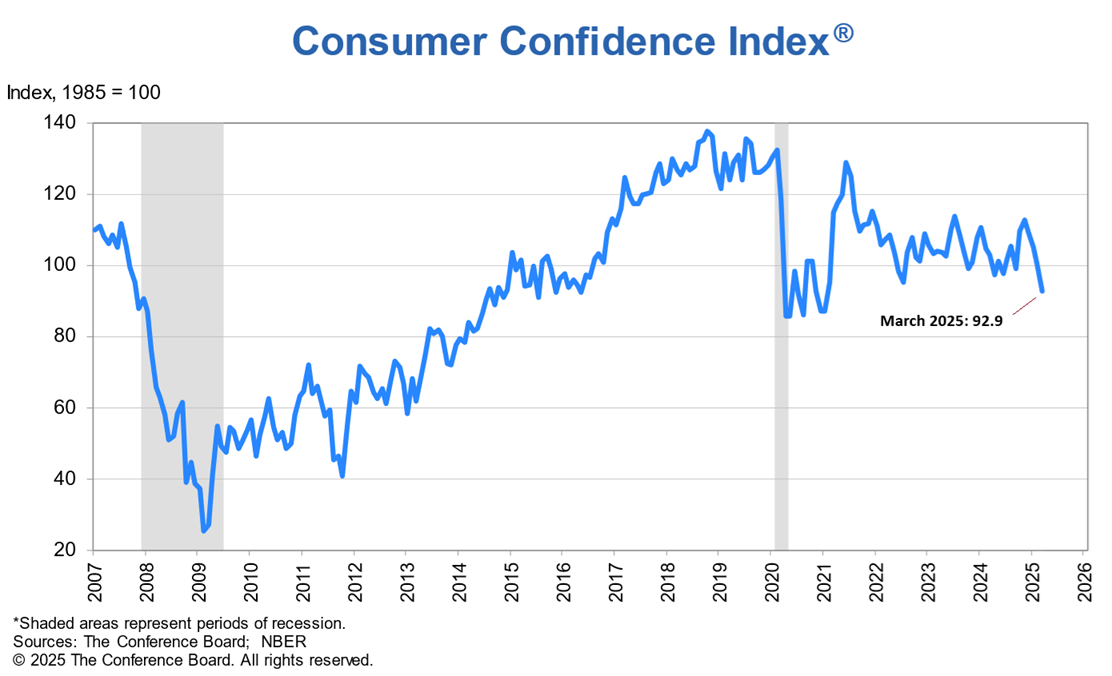

The US Consumer Confidence Index fell for the fourth consecutive month in March. This latest decline signifies a dip below the narrower range maintained since 2022, as noted by Stephanie Guichard, a senior economist at The Conference Board. “Among the Index’s five components, only the assessment of current labor market conditions showed slight improvement. Sentiment regarding business conditions weakened, approaching neutrality. Conversely, consumer expectations became significantly more pessimistic, with concerns about future business conditions intensifying and optimism about employment prospects dropping to a twelve-year low.”

Newly released data on Monday reaffirm the idea that the US economy continues to grow, with a low likelihood that a recession has begun or is on the horizon. Although rapidly evolving tariff conditions may alter the outlook, current economic activity appears to be robust.