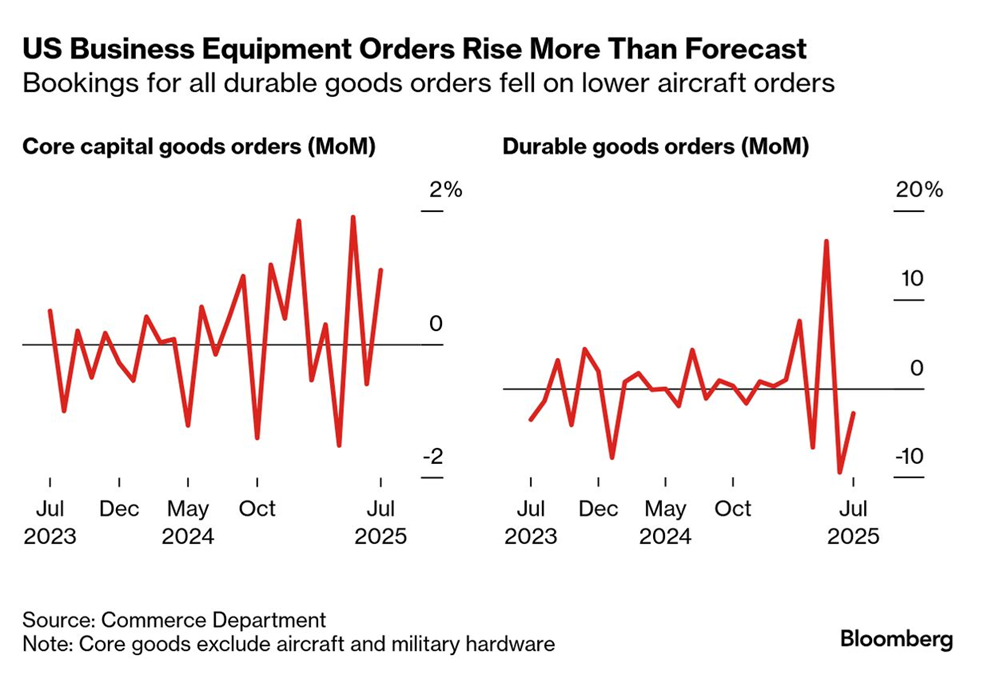

U.S. durable goods orders declined significantly in July, primarily due to a drop in transportation equipment. However, orders for non-defense capital goods, excluding aircraft—which serve as an indicator of business investment—saw a recovery with a 1.1% increase in July after a 0.6% decrease in June.

The economy is not currently in a recession and is unlikely to enter one in the near term. However, the increasing pressures from White House policies could challenge U.S. resilience in the coming months.

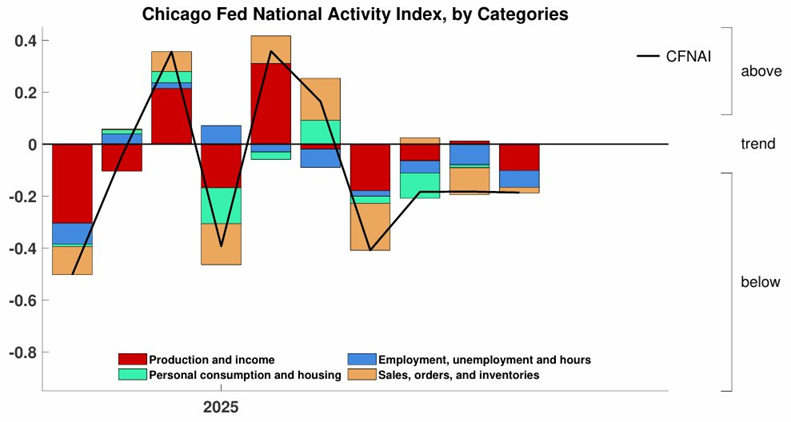

The Chicago Fed National Activity Index signals sluggish economic activity in the U.S. for the fourth consecutive month in July. The index published last month registered below-trend performance, with three out of four broad categories showing negative contributions.

Shifting towards foreign bonds continues to be a favorable strategy for U.S. investors this year, as evidenced by a comparison of ETFs up to Friday’s close (August 22). The modest gains from benchmarks of U.S. government and investment-grade securities have not been able to keep pace with international bond markets in terms of returns in U.S. dollars.

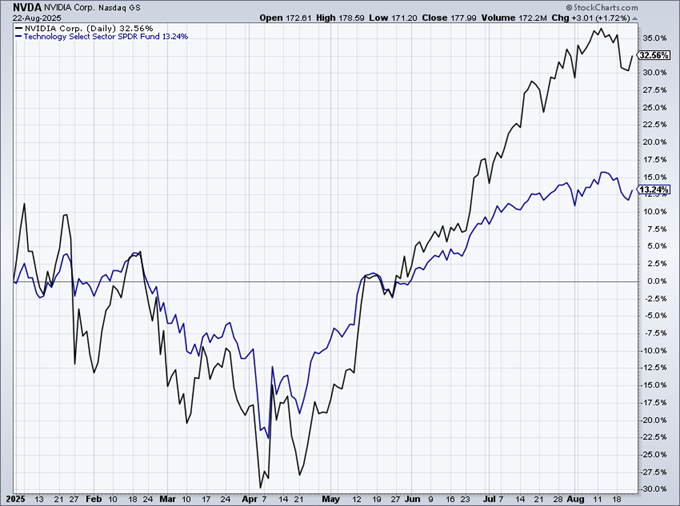

The impact of AI on technology stocks and the broader market will be a key focus this week, particularly with Nvidia, a leading chipmaker, set to release their earnings report on Wednesday. Nvidia, a crucial player in the AI sector, has significantly outperformed the tech sector this year, reporting a 33% increase compared to the sector’s 13% rise.

● Here Comes the Sun: A Last Chance for the Climate and a Fresh Chance for Civilization

● Here Comes the Sun: A Last Chance for the Climate and a Fresh Chance for Civilization

Bill McKibben

Review via The New Atlantis

In past years, my colleagues and I jested that after the revolution, every essay on climate change would be penned by Bill McKibben. This was during the latter part of the Obama administration and the start of the Trump era, when McKibben was a constant presence in mainstream media. From 2015 to 2021, he contributed at least two articles annually—up to six—in the New York Times, while also maintaining a regular column in the New Yorker and writing for various leading center-left publications like the New Republic, Rolling Stone, and the Nation. No significant legacy publication, it seemed, was immune to his influence.

However, recent trends suggest that McKibben’s revolutionary momentum may be losing ground.

The latest nowcasts for U.S. economic activity remain consistent in suggesting a moderate slowdown for the third quarter, according to the median of estimates gathered by CapitalSpectator.com. While the risk of recession appears low based on this update, growth is anticipated to significantly decrease compared to the strong performance observed in Q2.

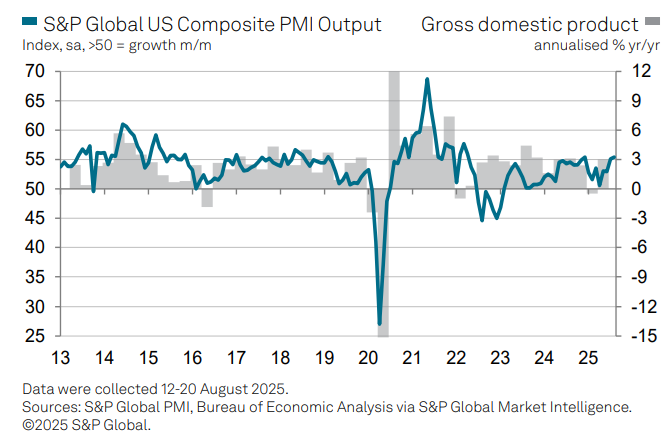

U.S. business activity showed a significant increase in August, achieving the highest growth rate of the year, according to the Composite PMI Output Index—a GDP proxy based on surveys. “The robust flash PMI reading for August indicates that U.S. businesses have experienced a strong third quarter thus far,” explains Chris Williamson, chief business economist at S&P Global Market Intelligence.

The bond market has remained stable this month as participants await new catalysts to assess potential interest rate cuts. On one hand, rising concerns about tariffs could heighten inflationary pressures, possibly leading the Federal Reserve to maintain its current policy. On the other hand, indications of slowing economic growth are building a case for rate reductions.

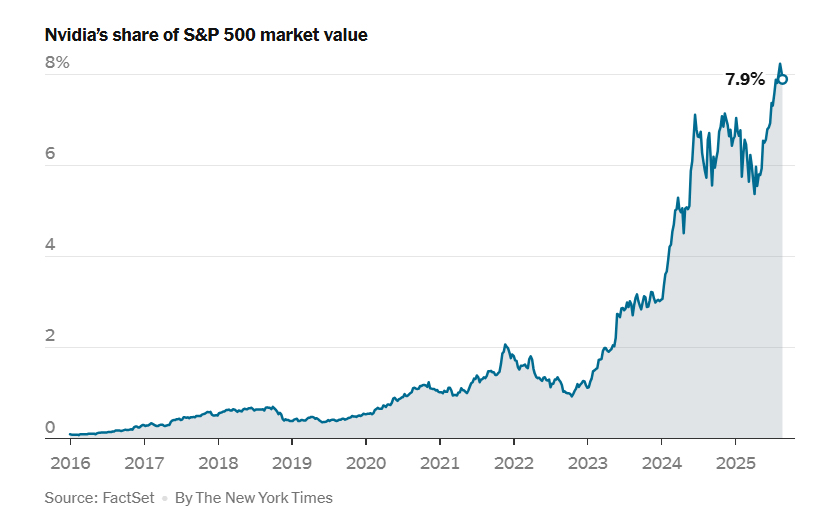

Nvidia’s upcoming earnings report next week is expected to significantly influence market sentiment. “In terms of relative importance, Nvidia’s earnings could be the most consequential event for the S&P 500 over the next month,” noted Stuart Kaiser, an equity strategist at Citi. Nvidia has seen its market share in the S&P 500 increase dramatically in recent years, now representing approximately 8% of the index’s total market value.