Yves here. Recent reports from mainstream media have illuminated the challenges facing several Asian countries, particularly India and the Philippines, due to the energy and impending food crises resulting from the Iran war. Author Satyajit Das presents critical data regarding the vulnerabilities of larger economies and explores the policy options available in times of severe disruption. The prospects appear grim.

By Satyajit Das, a former banker and author of various technical publications on derivatives as well as general titles, including: Traders, Guns & Money: Knowns and Unknowns in the Dazzling World of Derivatives (2006 and 2010), Extreme Money: The Masters of the Universe and the Cult of Risk (2011), and A Banquet of Consequence – Reloaded (2016 and 2021). His upcoming book focuses on ecotourism – Wild Quests: Journeys into Ecotourism and the Future for Animals (2024). This article builds upon a piece published in the New Indian Express on May 29, 2026..

The ongoing Iran war has underscored the crucial role of accessible energy in modern economies and societies. Disruptions in energy supplies create a divide between nations rich in oil and those that lack it. Rising energy prices, coupled with shortages of petrochemical products, will have a detrimental impact on various sectors, including agriculture, mining, plastics, textiles, semiconductors, and construction. Even if the conflict were to cease soon, returning to normalcy would necessitate months or even years, resulting in severe repercussions.

Europe, which has already been affected by the decision to cut off Russian gas supplies, and Japan are feeling the strain. However, the most significant impacts will manifest across oil-dependent nations in South and East Asia.

The severity of the situation hinges on pre-existing vulnerabilities like inadequate currency reserves, poor public finances, trade imbalances, elevated debt levels (especially in foreign currencies), dependence on foreign capital, limited industrial diversity, and inadequate contingency strategies. The table below outlines some important statistics:

Notes: All figures are primarily for 2025.

For countries reliant on energy imports, supply disruptions affect the economy through multiple channels. Import costs escalate, inevitably impacting the overall economy. The most immediate effect is a widening current account deficit.

Transport costs exacerbate inflation, prompting price increases across various sectors. Rising input costs reduce profitability for businesses, ultimately undermining their sustainability. As basic goods become pricier, disposable income dwindles, leading to decreased consumption and slower economic growth, which in turn results in increased unemployment. Tax revenues decline, and welfare expenditures rise, further straining government budgets. These challenges are often compounded by politically motivated subsidies, particularly for fuel, designed to alleviate living expenses.

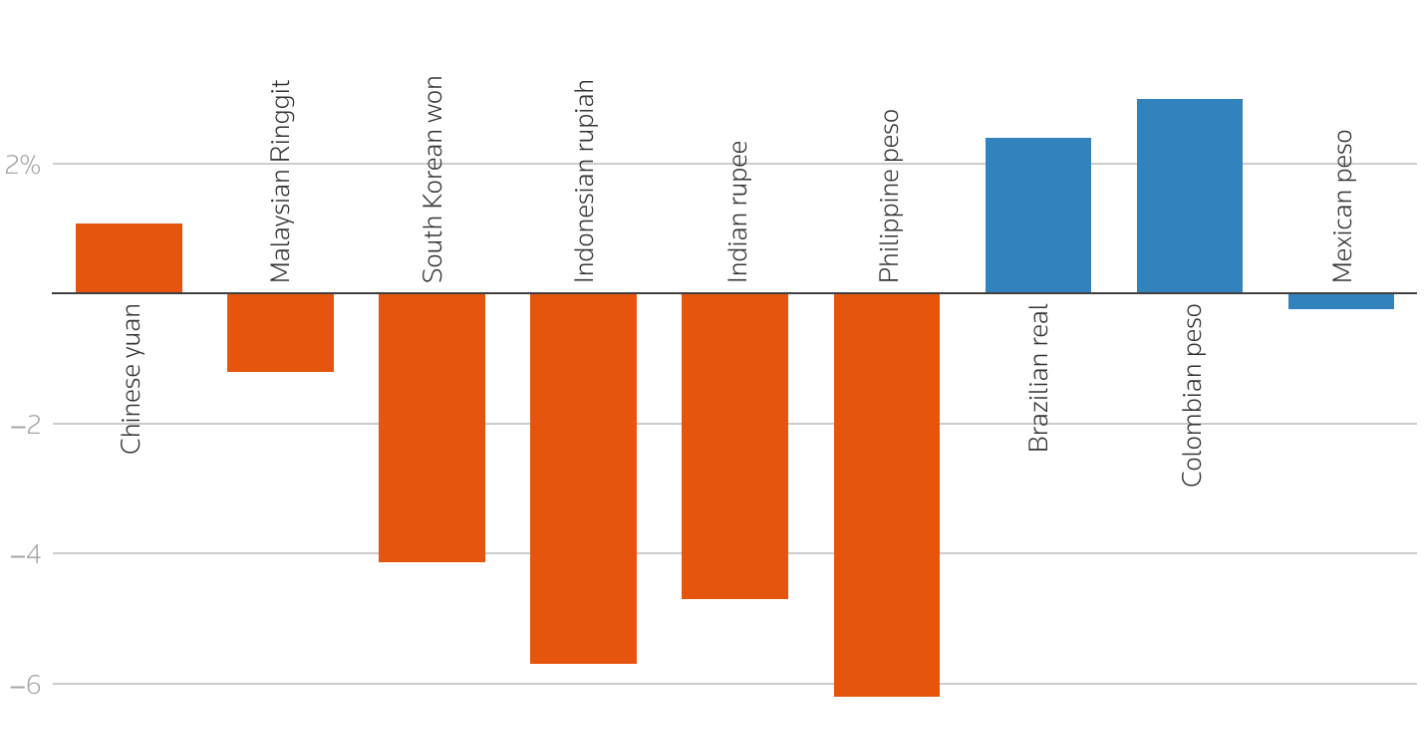

Financially, the most apparent consequences include weakened currencies and declining asset prices. Asian currencies have dropped by 5 to 6% since the onset of the Iran war. Stock markets in Asia, particularly those not linked to semiconductor industries like South Korea and Taiwan, are experiencing downturns, accompanied by heightened market volatility.

Source: https://www.reuters.com/world/asia-pacific/global-markets-war-graphic-2026-05-27/

Typically, inflows of foreign investment diminish as portfolio investors withdraw from equities and bonds, driven by declining asset values in their home currencies. Direct investments fall as economic prospects worsen. Banks confront a rise in non-performing loans due to a struggling economy while also facing diminished loan demand. For those dependent on foreign borrowings to supplement domestic funds, access to capital becomes restricted.

Inflation exerts upward pressure on interest rates, further decelerating economic activity and compounding financial pressures. This crisis exemplifies how oil shocks ripple through economies. Additional complications, such as neglected Trump-era tariffs and ongoing economic conflicts manifested as trade restrictions and sanctions, will only heighten existing challenges. The likelihood of economic and financial turmoil across many affected nations is significantly amplified.

What measures can be taken? As a wise Irish farmer once told an outsider seeking directions, “I wouldn’t start from here!”

The traditional policy approach is to allow currency devaluation to instigate necessary adjustments. Alternatively, governments could intervene in currency markets and raise short-term interest rates to stabilize the exchange rate. The most drastic option involves implementing measures to restrict capital outflows and potentially deploy price and income controls. Each approach has its pros and cons.

In theory, currency depreciation should reduce imports by dampening demand, provided typical supply and demand principles apply. This should also boost exports. However, such adjustments frequently result in harsh living standard reductions, especially for vulnerable low-income groups.

In practice, the effectiveness of currency devaluation is contingent on multiple factors, particularly the responsiveness of demand for a nation’s imports and exports. Essential imports, like energy, may not see a decrease in demand, while growth in export volumes depends on product type and price sensitivity. Additionally, competition and available alternatives play crucial roles. If competitors offer superior products or can match prices, export volumes may remain stagnant. This scenario is further complicated when all emerging market countries collectively devalue their currencies, undermining any individual nation’s efforts to reduce currency value. Moreover, a simultaneous slowdown in advanced economies, like the US and Europe, diminishes demand for Asian exports, which are vital for these economies.

Currency devaluation also tends to exacerbate inflation through increased import costs unless it suppresses demand sufficiently to curtail economic growth. A weaker currency can quicken capital flight as investors become concerned about potential losses. This dynamic may cause disruptive behaviors, with importers rushing to purchase needed goods while exporters delay converting foreign currency earnings. For businesses borrowing in foreign currencies without matching revenues to hedge against risk, the situation leads to heightened indebtedness. Emerging markets often leverage lower interest rates compared to domestic funding, which exposes them to currency risks.

Interventions in money markets typically yield minimal success and risk depleting currency reserves that are essential for commercial imports or short-term debts. Historically, successful interventions require collaboration among major central banks, like the 1985 Plaza Accord which aimed to devalue the dollar. Unfortunately, emerging market central banks have struggled in this respect. During the 1997 Asian financial crisis, countries like Thailand, Indonesia, and Malaysia burned through their foreign exchange reserves in fruitless attempts to defend their currencies pegged to the dollar. Generally, when foreign currency debts and investments exceed reserves, successful interventions are rare.

To combat currency decline, central banks in India, Indonesia, and the Philippines have attempted to intervene in currency markets, drawing down their foreign exchange reserves but with limited success.

Capital controls require the management of exchange rates while restricting the flow of foreign currency into and out of the country. While they can help manage crises, maintaining economic sovereignty over exchange rates, interest rates, inflation, and the banking system, long-term capital controls may deter foreign investment due to concerns about repatriating funds. This can lead to the emergence of a black market for currency and alternative practices that undermine their efficacy.

Within a market-based system, insulating an economy from massive external shocks like those imposed by the Iran war becomes challenging. Underdeveloped domestic capital markets restrict the local supply of capital and adequate risk management tools, hampering the capacity to absorb shocks effectively.

Many emerging market economies are starkly unprepared. Even without supply chain disruptions, they possess alarmingly low buffer stocks or reserves. Their economic structures lack diversification, leaving them vulnerable despite prior energy crises. Efforts to increase energy independence, including conservation and alternative energy sources, have been inadequate. Investment in renewables—solar, wind, hydro, and biofuels—remains insufficient. Worst still, emergency strategies for scaling up alternative fossil fuels, such as coal, are largely nonexistent. In contrast, China has proactively built significant strategic oil reserves and developed renewable energy options, which currently account for up to 40% of its total electricity generation and over 50% of its installed power capacity.

Governments have fostered a sense of complacency among their citizens, leading to a belief that policymakers can shield them from these crises. While politically popular, subsidies, transfers, and price controls do not tackle the fundamental issues at hand.

Similar to Aesop’s grasshopper, energy-deficient countries have squandered periods of surplus and now face a challenging winter.

Satyajit Das June 2026

© 2026 Satyajit Das All Rights Reserved