U.S Carbonated Soft Drinks Market Size

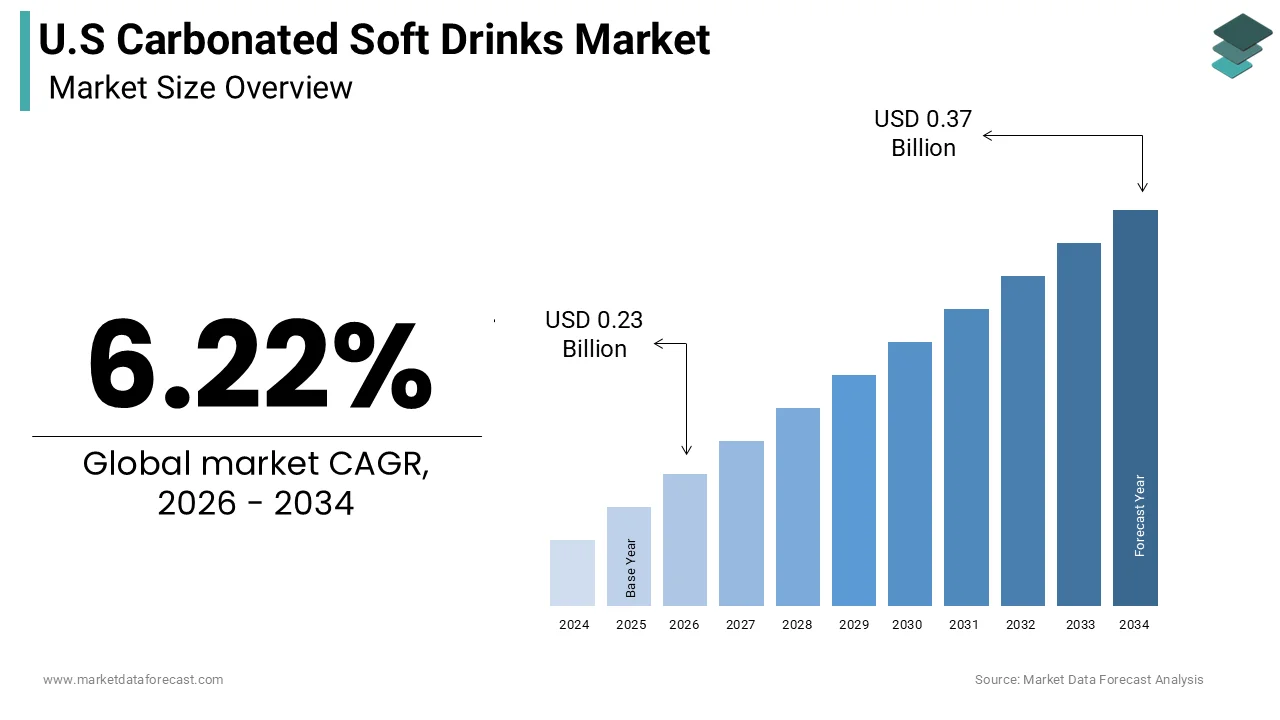

The U.S. carbonated soft drinks market is poised for growth, valued at USD 0.22 billion in 2025 and anticipated to reach USD 0.37 billion by 2034, with an annual growth rate of 6.22% between 2026 and 2034.

Carbonated soft drinks include a variety of beverages, from traditional cola and lemon-lime flavors to sparkling waters and functional sodas. The Centers for Disease Control and Prevention indicates that approximately 42.4% of U.S. adults are classified as obese, which has influenced dietary choices, leading to a decline in the consumption of sugary drinks. Additionally, the environmental impact of single-use plastic bottles has prompted a shift toward sustainable packaging. Consumers are increasingly mindful of artificial ingredients and are thus opting for products that utilize natural sweeteners like stevia and monk fruit. The trend of incorporating functional ingredients, such as probiotics, further blurs the lines between soft drinks and wellness products.

MARKET DRIVERS

Innovation in Zero-Calorie and Natural Sweetener Formulations

The introduction of innovative zero-calorie and natural sweetener formulations has fueled growth in the U.S. carbonated soft drinks market. Modern consumers are seeking beverages that deliver the soda experience without the associated health risks of high sugar intake. According to the International Food Information Council, 73% of Americans noted in 2024 that they are attempting to restrict sugar in their diets, thus generating significant demand for alternative sweeteners. Companies are investing in improving the taste profiles of non-nutritive sweeteners such as stevia and monk fruit, presenting a cleaner label appeal compared to synthetic options like aspartame. The popularity of zero-sugar variants of classic sodas is rising, prompting retailers to allocate more shelf space to these options, which cater to health-conscious consumers, including those managing diabetes and weight. These products allow consumers to enjoy flavors they love without dietary concerns.

Premiumization and Craft Soda Renaissance

A trend towards premiumization and the resurgence of craft sodas is driving market growth, as consumers increasingly seek unique and high-quality beverage experiences. A segment of consumers now views soda as not merely a thirst quencher but as a gourmet treat, willing to invest in artisanal and small-batch options. Craft sodas often feature exotic flavors and organic ingredients with lower sugar content, distinguishing them from mass-market products. Brands focusing on local sourcing and transparency foster trust and authenticity with consumers. This trend is particularly resonant with millennials and Generation Z, who prioritize ethical consumption. Independent soda makers are thriving in urban markets, often appearing in specialty grocery stores. The aesthetic appeal of premium packaging also reinforces brand loyalty, as it signals quality to consumers.

MARKET RESTRAINTS

Health Concerns Related to Artificial Ingredients and Obesity

Health concerns surrounding artificial ingredients and the association of sugary drinks with obesity are restraining the growth of the U.S. carbonated soft drinks market. Despite the availability of zero-calorie options, many products still contain high fructose corn syrup and artificial additives, increasingly viewed as harmful. Excessive sugar consumption is linked to various health issues, prompting parents to limit their children’s soda intake, opting instead for water or juice. The negative perceptions surrounding artificial preservatives and colorings have driven consumers to seek clean-label products made with familiar ingredients. Regulatory organizations are considering stricter labeling guidelines and potential taxes on sugary beverages, which could further dampen market growth. The stigma surrounding soda consumption as inherently unhealthy remains a considerable challenge for established brands trying to shift their reputations.

Environmental Impact of Single-Use Plastic Packaging

The environmental repercussions of single-use plastic packaging are a growing concern, prompting both consumers and regulators to call for sustainable alternatives. The beverage sector contributes significantly to plastic waste, with billions of bottles discarded each year. According to the EPA, only 29% of plastic bottles were recycled in 2023 in the United States. This inefficiency has resulted in public outcry and legislative movements aimed at reducing plastic usage. Brands are under increasing pressure to adopt sustainable packaging practices, facing potential backlash from consumers who evaluate their environmental responsibility. The costs associated with transitioning to sustainable materials can impact profit margins. The evolving regulatory landscape is pushing companies to invest in packaging innovations that also safeguard product integrity.

MARKET OPPORTUNITIES

Expansion into Functional and Wellness-Oriented Beverages

The incorporation of functional ingredients into carbonated soft drinks aligns with the increasing consumer demand for beverages that offer additional health benefits. This aligns with the broader wellness movement where consumers seek items that contribute to health beyond hydration. Opportunities exist for manufacturers to include probiotics, prebiotics, vitamins, and adaptogens in sparkling beverages. Probiotic sodas are particularly appealing to consumers keen on gut health, while adaptogenic ingredients are gaining traction for stress relief. These functional sodas typically contain lower sugar levels and natural flavors, presenting healthier alternatives. Retailers are keen to feature these innovative products, recognizing their appeal among health-conscious shoppers.

Growth in Direct-to-Consumer and Subscription Models

The rise of direct-to-consumer channels and subscription models offers new growth avenues for the U.S. carbonated soft drinks market, enabling brands to build more meaningful relationships with customers. Digital platforms facilitate direct sales, providing personalized shopping experiences and convenient delivery options. In 2024, direct-to-consumer e-commerce sales in the food and beverage sector increased by 20%. Subscription services allow consumers to receive regular orders of their favorite drinks, generating consistent revenue streams. This model is particularly useful for premium brands that struggle for placement in traditional stores. Direct engagement with consumers allows for targeted marketing and product adaptation based on preferences, enhancing brand loyalty.

MARKET CHALLENGES

Volatility in Raw Materials and Supply Chain Costs

Volatile prices of raw materials and supply chain disruptions pose challenges to the profitability of the U.S. carbonated soft drinks market. Key ingredients, such as sugar and aluminum, are subject to fluctuating global costs influenced by geopolitical and economic factors. Price fluctuations necessitate strategic decisions for companies, either absorbing costs or passing them on to consumers through price hikes, which may adversely affect demand. Supply chain disruptions, such as labor shortages and port delays, compound these problems. Companies are required to develop diverse sourcing strategies to support resilience amidst volatility, which can be operationally complex and financially burdensome.

Regulatory Pressure and Sugar Taxes

Regulatory pressures and the implementation of sugar taxes are complicating growth in the U.S. carbonated soft drinks market. Many jurisdictions have introduced taxes on sugary beverages, leading to increased retail prices and, subsequently, decreased sales. As reported by the Rudd Center for Food Policy and Health, areas implementing soda taxes have experienced reduced consumption. Companies must navigate diverse regulations, which elevates compliance costs, while also continuously reformulating their products to lower sugar content. Stricter labeling requirements place additional pressures on brands, compelling them to reinvent offerings while maintaining customer satisfaction. The political momentum behind public health initiatives suggests that regulatory scrutiny will intensify, demanding proactive adjustments from manufacturers.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

6.22% |

|

Segments Covered |

By Product Type, Flavor, Distribution Channel, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

|

Market Leaders Profiled |

The Coca-Cola Company, PepsiCo, Keurig Dr Pepper, National Beverage Corp., Monster Beverage Corporation, Jones Soda Co., Refresco, Cott Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

The carbonated water segment held the largest share of the U.S. market in 2025, driven by a consumer shift towards healthier hydration choices that forgo added sugars and calories. Increased awareness of the health risks linked to high sugar intake has led many consumers to favor alternatives that offer carbonation without compromising nutritional integrity. Carbonated water is perceived as a premium option that complements wellness lifestyles. Brands are enhancing their appeal with natural fruit essences and mineral enhancements, diversifying the product offerings to suit various palates. Many premium sparkling waters also boast the absence of artificial sweeteners, appealing to consumers who prefer clean-label products. Retailers are increasing shelf space for sparkling water, recognizing its quick turnover and broad demographic reach. Additionally, the versatility of carbonated water as a mixer elevates its utility beyond simple hydration, reinforcing its premium image through innovative packaging.

The sports and energy drink segment is projected to grow at the fastest rate of 7.8% from 2026 to 2034, driven by the rising demand for functional performance beverages among active consumers. The distinction between sports nutrition and mainstream hydration is diminishing, as individuals seek beverages that provide specific benefits like enhanced endurance, quicker recovery, and mental clarity. The Council for Responsible Nutrition reported a 15% increase in the use of sports nutrition supplements in the U.S. in 2024, highlighting a shift towards performance optimization. Carbonated sports drinks have gained popularity due to their capability of delivering hydration and electrolyte replenishment with a refreshing taste. The inclusion of caffeine and B vitamins in energy drinks is appealing to various demographics, including students and athletes. Innovations in natural caffeine sources like green tea extract attract health-conscious consumers seeking to avoid synthetic additives, while the introduction of zero-sugar and low-calorie options broadens market appeal. Marketing strategies often feature professionals and fitness influencers to foster brand loyalty, positioning these drinks as essential for peak performance.

By Flavor Insights

The cola flavor segment commanded 22.1% of the U.S. carbonated soft drinks market share in 2025, reflecting its iconic status and deep-rooted cultural significance in America. Cola has been synonymous with refreshment and social connection for decades, bolstered by substantial marketing efforts and widespread retail availability. Major brands cultivate emotional connections with consumers using nostalgic promotions and sponsorships of major events. The unique flavor attributes of cola, characterized by a mix of vanilla, cinnamon, and citrus oils, create a familiar comfort for many, encouraging repeat purchases across generations. The drink’s adaptability as both a standalone beverage and mixer enhances its utility and boosts consumption frequency. Retailers prioritize cola offerings for their reliability and consistent demand.

Conversely, the fruit-flavored segment is expected to experience the fastest growth rate of 6.5% from 2026 to 2034, driven by consumer preferences for natural fruit flavors that provide vibrant and refreshing taste experiences. Consumers increasingly desire beverages that replicate the freshness of real fruit juices while offering fizz. Popular flavors emerging in the beverage market include mango, passion fruit, and various berry combinations. Brands are adopting real fruit purees and concentrates to enhance these flavors, aligning with clean label trends. The visual appeal of fruit-flavored drinks, often featuring bright and natural colors, captures consumer attention. Social media significantly influences the popularity of these flavors, with influencers showcasing visually appealing beverages. The wide variety of fruit options allows for continual innovation, maintaining excitement within the category, especially among younger consumers.

By Distribution Channel Insights

The supermarkets and hypermarkets sector captured 34.6% of the U.S. market share in 2025, as consumers favor these large retailers for their one-stop shopping convenience. Easy access to a broad range of products and the ability to purchase in bulk contribute to their appeal. The expansive aisles and dedicated beverage sections enable eye-catching displays and promotions, influencing purchasing behavior. Economical bulk packaging options, such as multi-packs and cases, attract families and frequent buyers. Retail environments allow consumers to compare prices and brands concurrently, empowering informed purchasing decisions. Many supermarkets offer loyalty programs and digital coupons to encourage repeated sales. The availability of a diverse array of mainstream and niche brands ensures a broader range of consumer preferences is satisfied.

The e-commerce channel is anticipated to grow the fastest at a CAGR of 14.2% from 2026 to 2034. The convenience of online grocery platforms and subscription services is appealing to busy consumers who prefer avoiding store visits. This model ensures that customers with regular soda consumption don’t run out and enhances supply chain efficiency for manufacturers. E-commerce platforms often feature a vast selection of unique or specialty products that may not be found in brick-and-mortar stores. Online shopping allows consumers to read reviews and compare options easily, solidifying informed choices. Retail giants have been investing in last-mile delivery systems to minimize shipping times and costs. The integration of voice-activated ordering via smart devices furthers convenience, driving customer loyalty and repeat purchases.

COMPETITION OVERVIEW

Competition within the U.S. carbonated soft drinks market is fierce, dominated by a limited number of major players and a rising presence of niche and craft brands. Established companies exploit their extensive distribution networks and brand recognition to maintain market dominance while also responding to the surge in health-conscious consumer trends. Competitive pricing is a critical factor, especially in segments dominated by conventional sodas, where private-label alternatives offer cost-effective solutions. Innovation, particularly regarding flavors and functional benefits, drives loyalty and premiumization, compelling manufacturers to invest in research and development to keep pace with evolving dietary trends. Digital marketing strategies targeting younger demographics aim to enhance authenticity and engagement. The e-commerce landscape has lowered entry barriers, enabling smaller brands to capitalize on national market opportunities.

KEY MARKET PLAYERS

Prominent players in the U.S. carbonated soft drinks market include:

- The Coca-Cola Company

- PepsiCo

- Keurig Dr Pepper

- National Beverage Corp

- Monster Beverage Corporation

- Jones Soda Co

- Refresco

- Cott Corporation

Top Strategies Used by Key Market Participants

Leading players in the U.S. carbonated soft drinks market typically focus on product diversification and reformulating to improve health benefits. Many choose to introduce zero-sugar and low-calorie options to cater to health-conscious consumers. Expanding into functional beverages with added vitamins and probiotics is another popular tactic among firms responding to wellness trends. Strategic acquisitions of boutique and craft brands help larger companies broaden their offerings and tap into new markets quickly. Sustainability initiatives, such as implementing recycled materials in packaging and minimizing carbon footprints, enhance brand reputation and meet regulatory requirements. The embrace of digital transformation and improvements in e-commerce allow manufacturers to engage more directly with consumers, gathering valuable feedback for personalized marketing efforts. These multi-faceted strategies enable companies to adapt to changing market dynamics and sustain growth in a mature industry.

Leading Players in the US Carbonated Soft Drinks Market

- The Coca-Cola Company remains a strong leader in the U.S. market, leveraging an extensive portfolio and global distribution network to diversify its offerings to include zero-sugar and functional drinks. They are actively investing in sustainable packaging and utilizing advanced analytics for supply chain optimization and digital marketing campaigns.

- PepsiCo Inc plays a vital role in the market with a wide range of popular brands. They focus on innovation through new flavor introductions and limited editions while enhancing their e-commerce capabilities to better respond to consumer trends in sustainability and healthier options.

- Keurig Dr Pepper Inc contributes substantially, focusing on premium and craft segments while pursuing strategic acquisitions to enhance their offerings. By improving their distribution efficiencies and leveraging marketing campaigns, they continue to solidify their competitive position.

MARKET SEGMENTATION

This research report on the U.S. carbonated soft drinks market has been segmented and sub-segmented based on product type, flavor, distribution channel, and region.

By Product Type

- Soft Drinks

- Carbonated Water

- Sports and Energy Drinks

- Soda

- Others

By Flavor

- Cola

- Lemon-Lime Flavored

- Fruit Flavored

- Others

By Distribution Channel

- Supermarket and Hypermarket

- Convenience Store

- E-Commerce

- Food Service

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Key Takeaways

- The U.S. carbonated soft drinks market is projected to grow at a CAGR of 6.22% from 2026 to 2034.

- Health-conscious consumers are driving demand for zero-calorie and natural sweetener alternatives.

- The premiumization trend is fostering the growth of craft sodas, prized for unique flavors and quality ingredients.

- Environmental concerns over single-use plastics are leading brands to adopt sustainable packaging solutions.

- The e-commerce channel is anticipated to grow rapidly, driven by convenience and varied product offerings.

FAQ

What factors are driving the growth of the U.S. carbonated soft drinks market?

Factors such as innovation in zero-calorie options, the rise of premium craft sodas, and increasing health awareness among consumers are key drivers.

How are brands responding to health concerns related to sugary drinks?

Brands are reformulating products to lower sugar content and introducing natural sweeteners to meet the demand for healthier choices.

What role does e-commerce play in the carbonated soft drinks market?

E-commerce is becoming increasingly important, providing brands with a direct-to-consumer channel that facilitates convenience and personalized shopping experiences.

How is the market addressing sustainability issues?

The market is responding by investing in sustainable packaging solutions and minimizing the use of single-use plastics, reflecting consumer preferences for eco-friendly products.