In a recent discussion, economist Michael Hudson, interviewed by Ben Norton, shed light on the increasing tendency of borrowing in the US to fuel speculation in assets rather than productive investments. This shift has led companies to prioritize stock buybacks and outsourcing over reinvesting in their core operations. Notably, in a 2005 article for the Conference Board Review titled The Incredible Shrinking Corporation, we initially addressed this troubling trend.

This conversation delves into how post-financial crisis policies have exacerbated this behavior, providing current data that illustrates its far-reaching consequences, notably the growing wealth inequality.

A minor correction is warranted: Hudson identifies retained earnings and stock issuance as primary sources of investment capital. However, in reality, the order of significance is retained earnings, borrowing, and equity sales. Fortunately, borrowing today is different from traditional bank loans. Smaller businesses might secure loans against real estate or receivables, while larger firms typically issue corporate bonds or commercial paper.

Originally published at Geopolitical Economy Hour

Is another financial crisis looming over the US economy? Economist Michael Hudson discusses the potential hazards. Reports indicate that the US economy might be on the brink of a new financial meltdown, particularly within the $3 trillion private credit market.

Increasingly, signs suggest that the United States may face a significant financial crisis, beginning in the unstable private credit market and potentially extending to other areas.

Ben Norton, editor of the Geopolitical Economy Report, engaged with Michael Hudson to examine the pressing issues on Wall Street. Hudson cautions that the US economy has come to rely on a Ponzi-like scheme, perpetuating a system teetering on unsustainable speculation rather than industrial output.

BEN NORTON: There are mounting indicators that we might be on the brink of another substantial financial crisis.

A former Goldman Sachs CEO remarked in a Bloomberg interview that he can sense an impending financial crisis. Where might this crisis originate? Concerns are intensifying over the private credit sector in the US.

This sector has ballooned in recent years, especially after the 2008 financial crash prompted stricter bank regulations. Consequently, numerous firms on Wall Street began lending to private corporations, inflating the private credit industry.

As it stands, the industry is a $3 trillion domain yet remains largely unregulated. Many private credit firms have issued poor loans to at-risk companies that are now on the verge of defaulting.

We have released a brief video summarizing the issues in the private credit industry and the apprehensions surrounding a potential financial crisis. However, this video serves merely as an introductory overview.

Delving deeper into the subject, it became apparent that economist Michael Hudson would provide valuable insights.

Michael is the author of numerous works, including Killing the Host: How Financial Parasites and Debt Destroy the Global Economy.

BEN NORTON: Michael, thank you for joining us. It’s always a pleasure.

Let’s examine the likelihood of a new financial crisis. Financial media outlets like Bloomberg and the Financial Times have been frequently warning about this possibility.

The crisis could initially emerge from the private credit sector, which is experiencing heightened default rates, eventually spreading to banks and other industries.

Moreover, the AI bubble, geopolitical conflicts, and energy price shocks add layers of complexity to our conversation. Let’s start by discussing this potential crisis. Do you believe we are nearing another significant financial collapse?

MICHAEL HUDSON: Certainly. The core issue traces back to 2008, or more specifically 2009, when President Obama assumed office. His response to the subprime mortgage crisis and banking fraud fueled a transformation of the economy into a Ponzi scheme.

In bailing out the banks, which had made a flood of fraudulent and high-risk loans, many major banking institutions found themselves in negative equity.

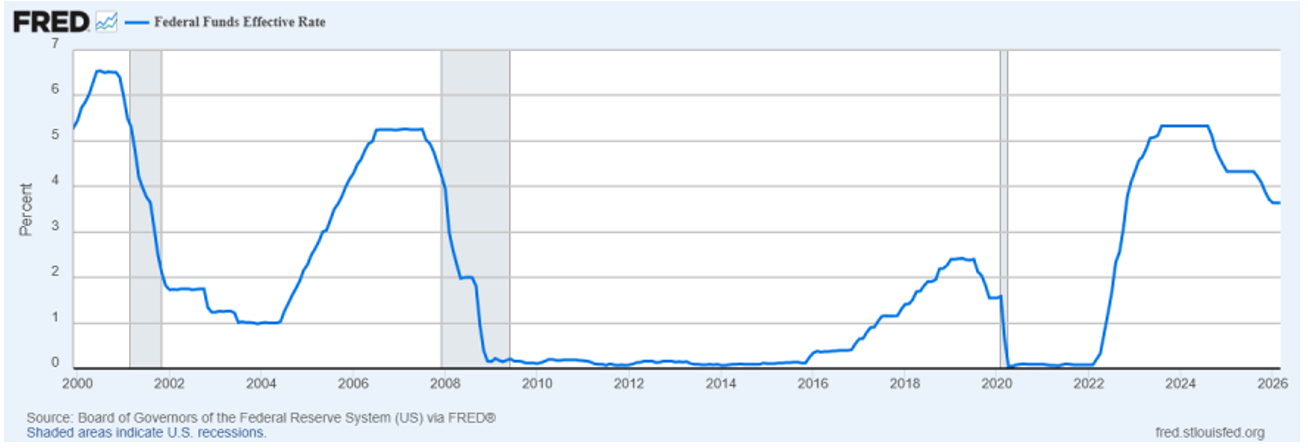

The solution? The introduction of a zero interest-rate policy (ZIRP). The Federal Reserve lowered interest rates from the elevated levels of the crisis in 2008 and 2009 to a mere 0.1%, the rate at which banks could borrow.

The Federal Reserve began creating digital money, lending to banks at minimal interest. They essentially told banks, “You have all the funds you need at 0.1%, which you can lend out to the economy to stabilize the prices of real estate, stocks, and bonds, thereby addressing the banks’ negative equity.”

As a result, banks adopted a dual approach.

Firstly, they could simply park the 0.1% money borrowed from the Federal Reserve, making a risk-free return by leaving it there, benefiting from the Fed’s strategy to channel funds into the financial sector. Secondly, they were incentivized to lend money for investments rather than actual production.

However, banks aren’t structured to evaluate loans aimed at specific businesses. Their primary focus is on the collateral backing loans. In the United States and the UK, bank credit is not typically allocated towards financing industrial capital; that responsibility lies with the stock market or companies reinvesting earnings.

Consequently, banks only extend loans for existing assets such as real estate, stocks, and bonds, effectively transferring the responsibility of finding companies to take over onto intermediaries.

This has led private entities to assume control over companies, often resulting in asset stripping. A prime example is Thames Water in England. Private equity firms target fiscally vulnerable institutions, such as hospitals, proposing to divest real estate, use capital gains for special dividends, and convert ownership into long-term leases. Such strategies have led to numerous hospital bankruptcies.

Private equity has systematically undermined American businesses, coining a term: enshittification, reflecting a deterioration in the quality of services as companies aim to minimize expenses, impose more workload on employees, and increase overtime.

When labor attrition occurs, remaining workers must absorb the workload. As productivity rises, it results in an extractive, exploitative financial environment in the United States.

Meanwhile, this predatory framework yielded substantial profits for financialized corporations. Instead of reinvesting in growth or new infrastructures, firms invested abroad, particularly in China and other Asian countries.

A staggering 92-94% of corporate cash flow profits have been allocated towards dividend payouts and stock buybacks. Companies fueled a stock market surge by repurchasing shares, artificially inflating stock prices and creating an illusion of increasing earnings per share.

These gains weren’t truly earned; they represent economic rents acquired through predatory practices.

The financial landscape has morphed into a predatory sphere. Since 2009, the remarkable increase in financial wealth has disproportionately benefited the top 10% of the population.

Currently, approximately 40% of the American populace lacks any savings, living on the edge of financial collapse.

As living expenses rise, many are falling behind on credit card bills, personal loans, auto loans, and especially student debts. A significant portion of the bottom 60-80% has seen minimal increases in economic stability. The traditional middle-class is fading.

In reality, many so-called middle-class individuals function as wage earners, akin to blue-collar workers, facing rising rent and mortgage costs inflated by the sustained low-interest rates, which have encouraged excessive borrowing.

Now that interest rates are climbing, the financial pressures are intensifying.

Consequently, a wave of defaults is sweeping through consumers— a euphemism for wage earners in America— as well as corporations struggling to cope with the demands. This scenario reflects the backwash of a Ponzi scheme, where debtors are lent money solely to pay interest.

Credit card holders often send in payments using borrowed funds to maintain a current status, allowing the cycle of debt to persist.

Such schemes rely on continuous financial input to sustain exponential growth.

This dynamic applies to corporations as well. As consumer spending dwindles, businesses find it challenging to sustain sales, compounded by wage earners needing to allocate increasing funds for essentials like gas and electricity, which are subject to monopolistic pricing, consequently impacting their purchasing power.

As a result, companies producing goods and services face declining sales and profits, impeding their ability to service mounting debts, while the economy propels towards a financial crisis spurred by transitioning into a war economy. Layoffs and business closures are inevitable.

Farmers, chemical manufacturers, and electric companies are grappling with rising operational costs, prompting many to withdraw from the market.

We may be heading toward a scenario reminiscent of the Great Depression. Importantly, depressions are deflationary, contrary to common misconceptions.

The prevailing thought is that rising interest rates hinder the purchasing power of the wealthy, necessitating a reduction in labor’s purchasing power. The financial sector’s demands will eclipse economic stability— a hallmark of neoliberalism and finance capitalism.

The US has transitioned to a post-industrial, finance-driven society dominated by banks and influenced by government policies funded by contributions from financial and real estate sectors.

This self-reinforcing cycle poses significant challenges, as Ponzi schemes invariably culminate in crashes. Investors are beginning to withdraw from American and European markets, yet viable alternatives remain unclear.

BEN NORTON: I’d like to discuss the government’s response, or lack thereof, to this situation. The Trump administration appears deeply intertwined with the finance sector.

One of the largest donors to Trump’s 2024 presidential campaign is Stephen Schwarzman, the top-paid executive on Wall Street and CEO of Blackstone, a prominent alternative asset manager with a robust private equity division.

Under pressure from Wall Street contacts, Trump signed an executive order in August 2025 deceptively titled “Democratizing Access to Alternative Assets for 401(K) Investors,” which misleadingly suggests protection for average workers saving for retirement.

In reality, this initiative represented an attempt by Wall Street to push toxic assets onto ordinary citizens, as it became apparent that numerous bad loans had been made by private credit and equity funds, leaving the market in search of new holders for these liabilities.

In response, Trump commented, “We will ‘democratize’ access.”

Reportedly, some financial firms are even compensating wealth managers to encourage average individuals to invest in private credit funds, presenting an enticing 10% return while downplaying the risks involved.

This situation draws striking parallels to the collateralized debt obligations (CDOs) that bundled mortgage-backed securities leading up to the 2007-2008 financial crisis. Back then, credit rating agencies deemed these assets safe and risk-free, yet they proved disastrous.

Today, platforms like Robinhood enable many individuals, particularly younger demographics, to gamble their savings through risky engagements and derivatives, including ETFs tied to private credit funds.

Sophisticated investors and Wall Street firms seem intent on offloading these precarious assets onto average individuals. Alarmingly, the White House has facilitated these actions leading into a crisis that many had predicted.

What is your perspective on this situation?

MICHAEL HUDSON: Your observations are spot on, Ben.

When an investment firm interacts with an investor—many of whom are pension funds—it becomes evident that pension-fund capitalism is being utilized to prop up the Ponzi scheme.

In essence, companies are now contemplating how to profit from investors and fund managers, recognizing that we are entering a depression period where genuine profits will be rare.

However, firms aim to contain losses. The prevailing sentiment among wealthy funds, like Blackstone, is to mitigate potential setbacks by exploiting average consumers and pension fund managers.

All segments of the economy seem trapped in a confidence game, persuading consumers to believe in returns, all while obscuring the reality of capital loss.

During my time in Russia in 1994, subway advertisements promised colossal returns on savings. The entire economy was embroiled in schemes that ultimately faltered, just as we observe in the US today.

The Albanian-ization of the American economy is underway, reminiscent of the instability seen in post-Yeltsin Russia.

What you’re witnessing is a guarantee of lost capital. Yet if consumers remain focused on short-term gains, they might overlook forthcoming losses.

Pension-fund capitalism has sought to restrict wages to provide for the financial sector rather than establish a robust public pension system, revealing the exploitative nature of the system.

This model involves inflating a bubble, cashing in at its peak, and selling off assets to labor and pension funds while promising them prosperity, all the while setting them up for losses in the long run.

BEN NORTON: That’s an insightful analysis, Michael.

Let’s consider the broader context of the US economy. We’re currently grappling with an energy crisis attributed to the ongoing conflict in Iran, which has driven oil prices up significantly. Simultaneously, the private credit sector is in disarray.

Several additional fundamental issues are plaguing the US economy.

Recent charts indicate that the richest 10% of Americans account for half of all spending in the economy. Combined with the deindustrialization of the US, consumption is driving significant financial disparities.