In recent times, the economic environment in America has become increasingly problematic, with multiple issues compounding to create a troubling scenario. Key areas of concern include soaring consumer price inflation, rising interest rates, stagnant gross domestic product, and growing unemployment. This analysis delves into the current state of these economic challenges.

In recent times, the economic environment in America has become increasingly problematic, with multiple issues compounding to create a troubling scenario. Key areas of concern include soaring consumer price inflation, rising interest rates, stagnant gross domestic product, and growing unemployment. This analysis delves into the current state of these economic challenges.

Firstly, consumer price inflation remains well above the Federal Reserve’s target of 2 percent. According to the Bureau of Labor Statistics, the consumer price index reflects a troubling annual inflation rate of 4.9 percent.

Even when examining the Fed’s favored inflation indicator, the personal consumption expenditures price index, we see consumer prices rising at an annualized rate of 4.2 percent. This figure is still over double what the Federal Reserve aims for.

Additionally, short-term interest rates are significantly higher compared to the past 15 years. The rapid increase from 0 percent to over 5 percent in just 18 months has had a considerable negative impact on credit markets. This shift has been dramatically illustrated by the recent struggles faced by the managers of Silicon Valley Bank, who learned that what were once considered ultra-safe Treasuries could quickly turn into risky investments.

Simultaneously, while the unemployment rate stands at a historically low level of 3.4 percent, the labor participation rate is only 62.6 percent. This discrepancy clouds the true picture of the labor market; for instance, had the participation rate returned to its level from the early 2000s (67.3 percent), the unemployment figure would be significantly higher.

It seems inevitable that the unemployment rate will increase from here. With tightening credit conditions for both corporations and consumers, the economy is stalling, leading to potential job losses.

Working Harder or Working Smarter

Recent events have highlighted significant layoffs within the high-paying technology sector. The latest data from tech job tracker layoffs.fyi reveals that over 350,000 tech jobs have disappeared since the beginning of last year.

Moreover, within just the first six months of 2023, tech companies have eliminated nearly 200,000 positions. While some displaced tech workers may choose to pursue new startups, others will take on whatever roles they can find.

Unfortunately, replacing these high-paying tech careers with lower-wage service positions will not stimulate economic growth, nor will the expanding nursing home assistant profession significantly contribute to competitiveness in advanced and more lucrative industries.

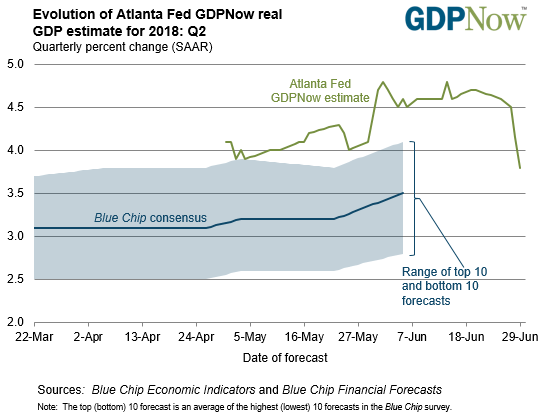

On another note, let’s examine economic growth. The Commerce Department recently announced that U.S. GDP rose at an annualized rate of only 1.1 percent during the first quarter of 2023—a meager indication of progress.

For American workers, the economy has already been declining for two years. Specifically, inflation-adjusted wages have been decreasing, meaning that workers have essentially been facing a pay cut every month for the last two years. Efforts to work harder or smarter have yielded little reward.

At this juncture, it is likely that the economy is already contracting. Though we won’t have official confirmation until the second quarter GDP report in July, it may serve as merely a footnote in what is shaping up to be a challenging summer.

Misleading Graphs

From this overview, it’s apparent that the economy is indeed slowing and potentially reversing. Unemployment is on the rise, consumer price inflation remains stubbornly high, and interest rates are elevated.

A similar situation unfolded roughly 45 years ago, and it was far from pleasant. While the current circumstances are not entirely the same, there are noteworthy similarities—especially regarding the confusion these conditions create for economists and policymakers.

In the late 1970s, a perplexing situation arose where both inflation and unemployment surged simultaneously, contradicting existing economic theories. Leading economists were bewildered, as such a phenomenon was considered impossible and went against their academic teachings.

The Phillips curve, which posits an inverse relationship between inflation and unemployment, suggested that as unemployment decreases, inflation increases, and vice versa. Economist William Phillips initially illustrated this concept using wage and unemployment data from the UK between 1861 and 1957, providing a seemingly straightforward explanation for economic behavior.

While this curve proved useful for economic modeling, it ultimately fell apart under real-world conditions. The surprise simultaneous rise in inflation and unemployment in the late 1970s shattered the theory, demonstrating that economic predictions are often unreliable. The 1970s experience radically altered the understanding of inflation and employment relationships.

Circa: Now!

In practice, the Phillips curve was a convenient yet flawed theory. As the late 1970s unfolded, the U.S. Treasury, supported by the Federal Reserve, followed Keynesian principles by running deficits to stimulate job creation.

Theoretically, the Phillips curve indicated that with rising unemployment, they could print money without causing price inflation. However, the unexpected outcome was rampant inflation, not new jobs. Subsequent attempts to implement this strategy resulted in further price increases without the desired job growth.

The lessons from Phillips’s study remind us of the limitations of deriving economic theory purely from historical data. The unpredictable nature of the economy means that patterns can change rapidly, challenging our understanding and expectations.

Furthermore, any data collected prior to 1971, when gold was removed from the monetary system, can no longer serve as a reliable reference for understanding inflation and unemployment dynamics. It seems logical that rising unemployment signals a declining economy, but a decrease in unemployment does not always correlate with economic recovery.

For instance, between January 2010 and January 2020, the U.S. unemployment rate dropped from 9.8 percent to 3.5 percent, yet this period saw minimal GDP growth, averaging only 2.3 percent. And now, as we face 2023—with low unemployment that is likely to rise, a stagnating economy, persistent inflation, and elevated interest rates—Fed Chair Jerome Powell, earning a pre-tax salary of $190,000 per year, finds himself with few effective options.

Unfortunately, each alternative appears grim. Yet it’s crucial to remember that this chaos is primarily a result of policies from the Fed and Washington. You can almost guarantee the Fed will exacerbate the situation.

[Editor’s note: Enjoy this article? If so, please Subscribe to the Economic Prism.]

Sincerely,

MN Gordon

for Economic Prism