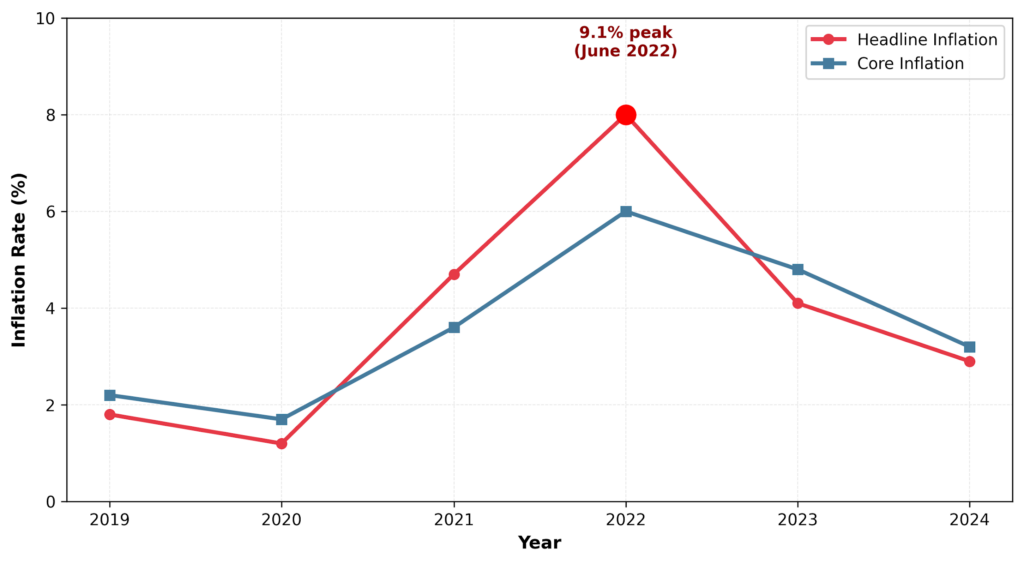

The inflationary landscape began to shift in 2021, a change triggered by pandemic-induced disruptions and ongoing economic reopenings. The outbreak of the Russia-Ukraine conflict in February 2022 compounded these challenges, leading to a commodity super cycle marked by soaring energy and raw material prices. This chain of events caused inflation rates to surge across numerous economies, particularly in the U.S., where the Consumer Price Index (CPI) peaked at 9.1% in June 2022 (see Figure 1). However, it is not just the way inflation rose that merits discussion, but also its notable decline that began in 2023.

Figure 1. Core and Headline Inflation

Headline inflation soared in 2022, then declined rapidly, while core inflation receded at a slower pace.

Source: FRED and author’s own calculations

During the inflationary surge in 2022, forecasts indicated that a prolonged period of high unemployment would be necessary to restore inflation to the Federal Reserve’s target of 2%. This perspective echoed the traditional Phillips curve theory, which suggests a trade-off between inflation and unemployment. Central to these predictions was the sacrifice ratio, which represents the increase in unemployment typically needed to lower inflation by one percentage point.

Despite historical precedents indicating that the sacrifice ratio would be significant, inflation decreased markedly without a corresponding rise in unemployment, which remained steady between 3.6% and 3.9% throughout 2021 and 2022. Ultimately, the sacrifice ratio turned out to be negligible.

This raises an important question: did economists overrate the lasting impact of supply-side shocks and the inflationary sensitivity linked to unemployment? Evidence points to a flatter Phillips curve, suggesting a lower relationship between unemployment and inflation, along with inflation expectations being firmly anchored around the 2% mark (Blanchard and Bernanke, 2023).

The economic scenario expected for 2025–26 appears to be more complex and potentially more challenging than the situations encountered in 2022–23. The tariffs introduced during this period offer valuable insights into:

- 1. The mechanics of supply-driven inflation, and

- 2. How policy measures can effectively combat inflation without incurring sacrifices.

Between 2025 and 2026, U.S. tariff rates soared from 2.4% to nearly 18%. This dramatic increase led to $195 billion in customs duties during fiscal year 2025 (Yale Budget Lab, 2025). Surveys reveal that American businesses anticipate tariffs to contribute to 40% of their overall unit cost increases during this period (Bostic, 2025). Concurrently, over 55% of companies now consider geopolitical factors as a primary concern for their supply chains in 2025, a rise from 35% in 2023 (Risk Management Magazine, 2025).

The decline in inflation, which occurred without a rise in unemployment, highlights the necessity of integrating supply-side factors and anchored expectations into macroeconomic policymaking.

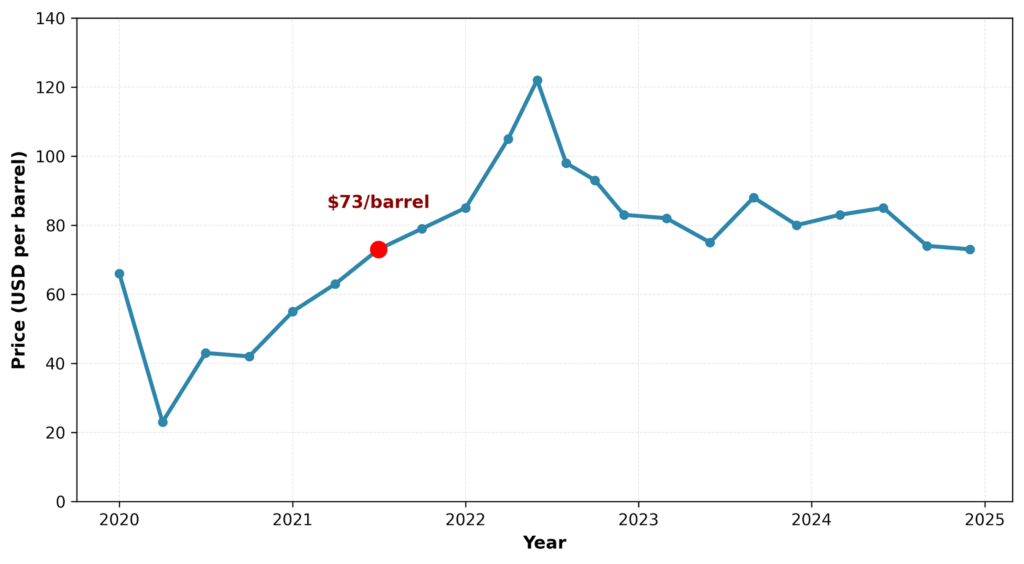

During the inflationary episode of 2022–23, supply chain disruptions and energy price shocks proved less persistent than predicted. Energy prices plummeted from over $120 per barrel in June 2022 to the range of $70–$90 per barrel by late 2023 (see Figure 2). Additionally, global supply chain pressures normalized by mid-2023 (Morales, 2025). Economists misjudged the duration of this shock, believing that supply and energy challenges would remain elevated well into 2024, rather than normalizing as early as mid‑2023.

Figure 2. Brent Crude Price

Brent crude prices significantly decreased from mid-2022 peaks to much lower levels by late 2023.

Source: FRED

Historical experiences from the 1970s suggested that supply-side shocks would be prolonged, correlating with unemployment costs associated with reducing inflation (Dolan, 2023). However, the supply-side context of the 2020s differs in meaningful ways. In addition, inflation driven by tariffs behaves differently compared to disruptions experienced during the pandemic.

Research conducted by Cavallo, Llamas, and Vasquez (2025) found that prices for imported goods increased between 4% and 6.2% from March to September 2025, whereas domestic goods rose by 2% to 3.6%. The price hikes for domestic products indicate that tariffs exert inflationary pressures beyond those associated solely with imported items.

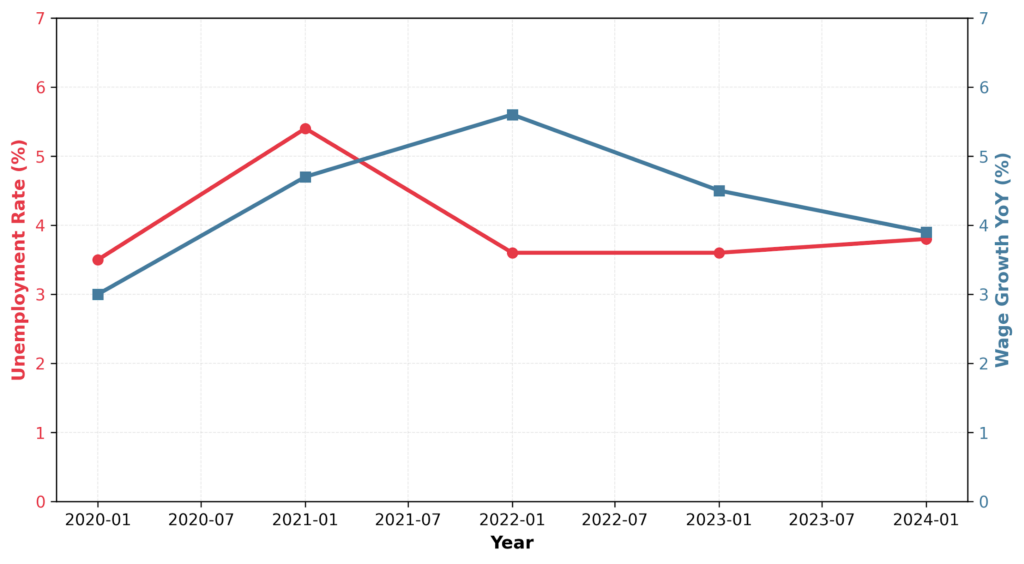

The labor market demonstrated resilience as returning workers helped maintain wage growth at modest levels, despite low unemployment rates. Wage increases slowed from 5.9% in March 2022 to 4.3% in October 2023, which highlights reduced labor market tensions while achieving lower inflation without requiring an employment sacrifice (see Figure 3). Initially, many believed that as workers re-entered the job market, companies would need to increase salaries considerably to attract them, thereby exacerbating inflation. Nonetheless, the influx of available workers allowed businesses to hire without significantly raising wages, leading to slowed wage growth, even with low unemployment.

Figure 3. Wage Growth and Unemployment Rates in the US

Wage growth slowed even as unemployment remained low.

Source: FRED and author’s own calculations

The Federal Reserve’s credibility has played a crucial role in maintaining inflation expectations close to its target of 2%. When these expectations are well anchored, individuals trust that inflation will not deviate significantly from this target, reducing the likelihood of planning for ongoing price increases. The Fed’s strong reputation, combined with a proactive communication strategy, has fostered a regime of expectations that limited second-round effects related to wage-price spirals (where rising wages lead to further price increases). This reflects a pivotal policy shift from adaptive to anchored expectations, firmly tied to the central bank’s objectives.

Before the inflationary period of 2021–2022, the concepts of inflation-targeting central banks and anchored expectations were largely theoretical. These ideas became tangible as unemployment stayed near historic lows while inflation rates decreased, as shown by the stable five-year breakeven inflation rates hovering around the 2% target.

Despite tariff-related pressures, long-term inflation expectations remain relatively stable. In November 2025, Atlanta Fed President Raphael Bostic emphasized that inflation represents a significant risk to the Fed’s dual mandate of ensuring price stability and maximum employment. Additionally, Fed Vice Chair Philip Jefferson noted that the “lack of progress” towards the inflation target seems to stem from tariff-related effects. Policymakers face the challenge of differentiating between one-time price shifts caused by tariffs and persistent inflationary pressures that necessitate monetary tightening.

The inflation episodes from 2021 to 2023 highlight the possibility of supply-driven disinflation occurring with a nearly zero sacrifice ratio when shocks are fleeting and expectations remain anchored. However, the conditions anticipated for 2026 present a different set of challenges. With inflation still above the Fed’s 2% target and signs of a weakening labor market, the Fed is unable to replicate the approach taken during 2021–2023, which involved waiting for supply pressures to dissipate while maintaining strict policies. Any further monetary tightening to counteract tariff-induced inflation risks exacerbating job losses, hindered hiring, and stagnant income growth for workers.

A key takeaway for policymakers is to acknowledge the impacts of supply-side factors, such as disrupted supply chains or sudden spikes in raw material costs, which can drive prices up from the production side. They must consider the transient nature of supply shocks in future inflation predictions. This lesson is particularly relevant for current tariff-induced inflation. While the Federal Reserve can uphold expectations through effective communication, it cannot counteract the direct price effects of tariffs without incurring economic costs. The policy challenge is magnified because tariffs are discretionary administrative choices rather than external shocks.

Insights from the inflation experiences of 2021–2023 and the evolving economic landscape of 2025–2026 underscore the necessity for a coordinated approach between monetary and trade policies. A recent analysis by Yahoo Finance (2025), informed by J.P. Morgan Global Research, estimates that announced tariff measures could elevate Personal Consumption Expenditures prices by 1.0–1.5 percentage points in 2025. It is crucial to carefully preserve the credibility of the central bank, as repeated policy-induced shocks that drive inflation above target can compromise this credibility.

The upcoming challenges in 2025–26 involve addressing a distinct type of supply shock—one driven by trade policy distortions rather than disruptions in supply chains, ideally with minimal economic fallout.

The essential lesson for policymakers is that anchored inflation expectations and clear differentiation between supply shocks and demand pressures allow for significantly lower costs associated with disinflation than conventional models predict. Achieving disinflation at such minimal costs necessitates coordinated policy efforts and sustained central bank credibility in a uniquely uncertain economic environment.