Global Athleisure Market Overview

Market Size & Forecast

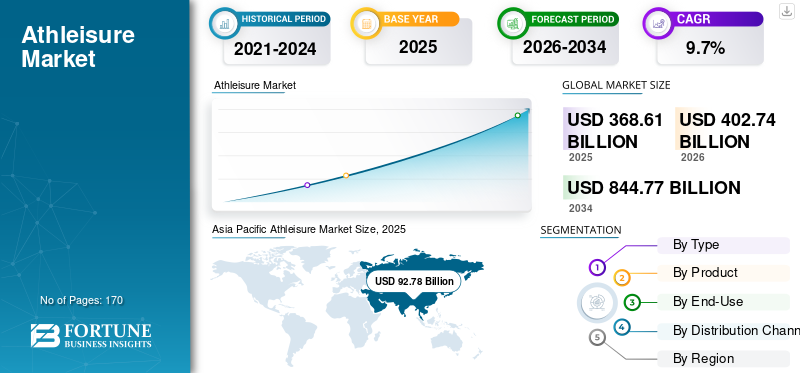

- 2025 Market Size: USD 368.61 billion

- 2026 Market Size: USD 402.74 billion

- Projected 2034 Market Size: USD 844.77 billion

- CAGR (2026–2034): 9.7%

Market Dynamics

- Dominance: Asia Pacific held a 25.17% share in 2025, influenced by growing health consciousness and increasing demand for versatile clothing.

- Product Types: Common items include sports bras, leggings, sweatpants, and athletic shoes, blending functionality and style.

Impact of COVID-19

- Shift towards comfortable clothing during remote work, significantly boosting athleisure sales as consumers prioritized fitness and casual wear.

Key Growth Factors

- Health and Wellness: Emphasis on fitness driving demand.

- Fashion Trends: Increasing preference for casual, comfortable clothing due to changes in work and lifestyle.

Restraints

- Proliferation of counterfeit products negatively affecting brand image and sales.

Segmentation Analysis

By Type

- Mass segment dominates with a 63.3% market share anticipated in 2026 due to increasing online shopping.

- Premium segment expected to grow rapidly, driven by rising incomes in developing regions.

By Product

- Sweatpants and joggers expected to see the highest growth, influenced by hip-hop culture.

- T-shirts remain a significant segment due to their versatility.

By End-Use

- Women’s segment is leading, supported by rising participation in fitness activities.

- Men’s athleisure segment projected to grow rapidly.

By Distribution Channel

- Offline retail expected to lead, but online stores are rapidly gaining traction due to convenience.

Regional Insights

- North America: Expected to generate USD 136.51 billion in 2025, led by the U.S. market.

- Europe: Contributes 30.21% of the global market; growing awareness and presence of major brands.

- Asia Pacific: Rapid growth expected, with countries like China and India leading in market size.

Key Players

Major companies include Adidas, Nike, Under Armour, and Lululemon, focusing on innovation and sustainability in their product lines.

Key Developments

- Recent launches by major brands to expand product ranges and offerings, focusing on comfort and functionality.

Conclusion

The global athleisure market is poised for substantial growth, driven by health trends, evolving consumer preferences, and continuous innovation from key industry players.