This article features insights from Joel Bowman, the esteemed founder and author of the enlightening Notes from the End of the World.

This article features insights from Joel Bowman, the esteemed founder and author of the enlightening Notes from the End of the World.

We have followed Mr. Bowman’s work for nearly two decades, as it has taken him to many countries across the Americas, Europe, as well as the Middle and Far East. When he isn’t exploring the world with his family, he spends part of the year in Buenos Aires, Argentina.

Recently, we caught up with Bowman in the mountains of southern Appalachia, where he shared insights into President Javier Milei’s intriguing libertarian experiment in Argentina.

By addressing issues like national debt, deficits, tax reductions, and inflation—effectively taking a chainsaw to bureaucratic regulations—Milei is offering a model that other nations, including the United States, can adopt to move away from the failings of large, corrupt governments. This narrative is both compelling and crucial for anyone who values freedom and individual liberty.

We have no financial ties with Bowman, nor do we profit from sharing his work. Our motivation lies in the value of his observations and writings, which we believe are worth sharing.

Bowman’s piece, How to Make a Government Disappear Completely, will bring you up to speed on the latest developments in Milei’s trial of libertarian governance in Argentina. After reading, be sure to visit his website and subscribe to his newsletter for real-time updates.

Enjoy!

MN Gordon

—

How to Make a Government Disappear Completely

One deficit, one debt, one burdensome tax at a time…

By Joel Bowman, founder of Notes from the End of the World

“If the bulk of the public were really convinced of the illegitimacy of the State, if they recognized that the State is essentially a grand bandit gang, then it would soon collapse, losing any more status than that of a mere Mafia gang.”

~ Murray N. Rothbard, from The Ethics of Liberty (1982)

Don’t look now, dear reader, but there’s more promising news from the (other) End of the World…

After committing to a radical “zero deficit” policy, Argentina’s libertarian president, Javier “El Loco” Milei, has once again provided a month of unexpected economic stability.

Here’s the latest update from the nation’s Ministry of Economy (translated):

“MAY RECORDS ANOTHER PRIMARY AND FINANCIAL SURPLUS”

“In May 2025, the National Public Sector recorded a primary surplus of $1,696,917 million and a financial surplus of $662,123 million.

“Thus, in the first five months of the year, we noted a financial surplus of about 0.3% of GDP and a primary surplus of around 0.8% of GDP, confirming the National Government’s commitment to its fiscal anchor, a cornerstone of the economic plan initiated in December 2023.”

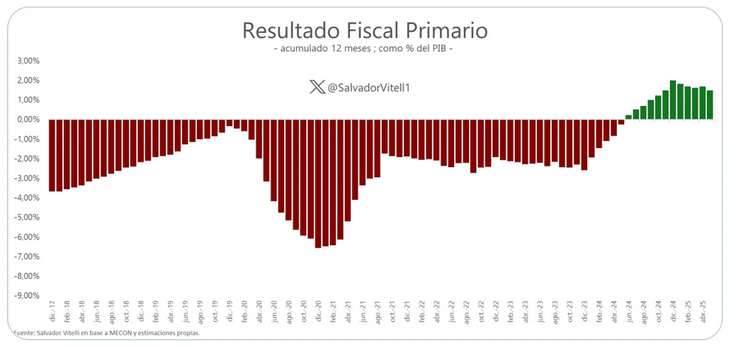

This latest surplus marks the twelfth consecutive month of progress, accumulating to 1.45% of GDP.

For those unfamiliar with such uncommon occurrences, here’s what a primary fiscal surplus appears like in graphical form…

(NB: Notably, Milei took office in December 2023, indicated at the start of the promising trend shown in the graph.)

Deflating Inflation

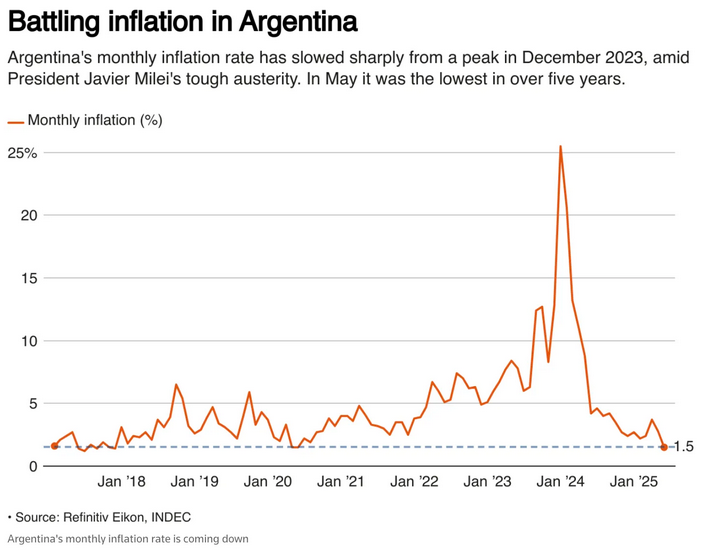

Simultaneously, Argentina’s Public Enemy #1—inflation—has been effectively restrained. The latest statistics from INDEC, the national institute of statistics, indicate a decline in inflation to its lowest level since the economy’s downturn during the tumultuous times of Covid in 2020.

Even mainstream news outlets have been compelled to acknowledge this inconvenient truth. For instance, here’s how one outlet described the situation:

“BUENOS AIRES, June 12 (Reuters) – In May, Argentina’s monthly inflation rate dropped to its lowest in over five years, according to official data released Thursday, boosting the momentum behind President Javier Milei’s effort to eradicate chronic price increases.”

“Prices rose only 1.5% from the prior month, according to national statistics agency INDEC, well below the 2.0% prediction from analysts surveyed by Reuters.”

Although still excessively high, the annualized rate of 43.5% is an improvement from 47.3% last month and a dramatic decrease from an official high of 289.4% recorded last April.

Often referred to as the “stealth tax,” inflation most adversely affects those on the lower rungs of the economic ladder—those who politicians often profess to care about but tend to avoid seeing on the streets.

Notably, items like home appliances (1.4%), clothing and footwear (0.9%), non-alcoholic food and beverages (0.5%), and transportation (0.4%) have experienced lower inflation rates, reflecting trends that resonate with real people’s concerns.

But let us pause for a moment and ponder a question seldom asked during the Age of Experts: Why?

What draws our interest to the developments at the End of the World beyond the fact that we share 0.6% of the global population living there?

A compelling question indeed.

The Path to Government Accountability

When we first journeyed to Argentina in 2010, it was an economic disaster, teetering on the brink of catastrophe akin to that of Caracas—if not Harare. The political landscape resembled a vast crime scene, where one could easily outline the entire barrio of Congreso and find no integrity or honor within.

However, our move wasn’t motivated by economic opportunity or political affiliation. Long-time readers are aware that we often prefer to remain distanced from politics. Our relocation to Buenos Aires (from Taipei) was inspired by the city’s Belle Époque architecture, abundant bookstores, leisurely post-dinner drinks, and vibrant cultural experiences surrounding sobremesa.

It was all about lifestyle—valuing private matters over public distractions, prioritizing the individual over the collective, and placing community above government.

After enduring three-quarters of a century of economic mismanagement and governmental spectacles sure to make a Roman senator blush, Argentines have witnessed a multitude of scams, schemes, and swindles. They have come to understand what genuinely matters in life and how to appreciate it, even as their surroundings deteriorate. (More on CFK in future Notes…)

Imagine our astonishment when, amidst all this, Argentina transformed into an expansive real-world experiment in libertarianism, electing a self-proclaimed “enemy of the state” to combat governmental overreach.

Everything written over the years—esoteric concepts such as “balanced budgets,” “sound currency,” and “personal accountability”—was about to face a critical evaluation.

We termed it, with considered enthusiasm, the “Greatest Political Experiment of Our Age” and prepared ourselves for an exhilarating journey.

Understanding Natural Laws

Undoubtedly, mistakes are inevitable along this path—judgment errors and all too human oversights. In the sphere of politics, fairness often takes a back seat. But we must navigate a world forged by imagined realities, where humanity’s most foolish ideas flourish in capital cities, from Buenos Aires to Washington, D.C, London, Ottawa, Sydney, and beyond.

Yet, we exist in the world as it is, not as we yearn for it to be. Acknowledging cause and effect is essential. As the song suggests, the politics bone is connected to the economics bone, and the economics bone connects to real life. This is what makes the Argentine experiment so captivating.

Javier Milei’s spokesperson, Manuel Adorni, elaborates on how to effectively dismantle government power, one deficit and one debt at a time:

‘“When there’s a fiscal surplus and the printing press slows, inflation decreases naturally. This is a fundamental economic principle.”’

Some people, gazing theatrically at the world stage, become wistful for the days of esteemed statesmen and honorable political figures. However, what they seek is an illusion—a fantastical mirage. Politics is anything but dignified, while socialism is hardly social, and communism lacks community.

The political arena resembles a realm dominated by unrefined thugs, rife with deception and pretense that, once stripped away, reveals nothing but raw force and violence.

We do not aspire to better politicians, more polished salesmen, or shrewder communicators. Instead, we desire a significant reduction in the power of unscrupulous bandits. Our interest in politics is not for its own sake, but rather to ultimately reach a point where it’s no longer necessary.

Stay tuned for more Notes From the End of the World…

Best wishes,

Joel Bowman

founder of Notes from the End of the World

Return from How to Make a Government Disappear Completely to Economic Prism